Table of Contents |

The Wealth-Building Companion

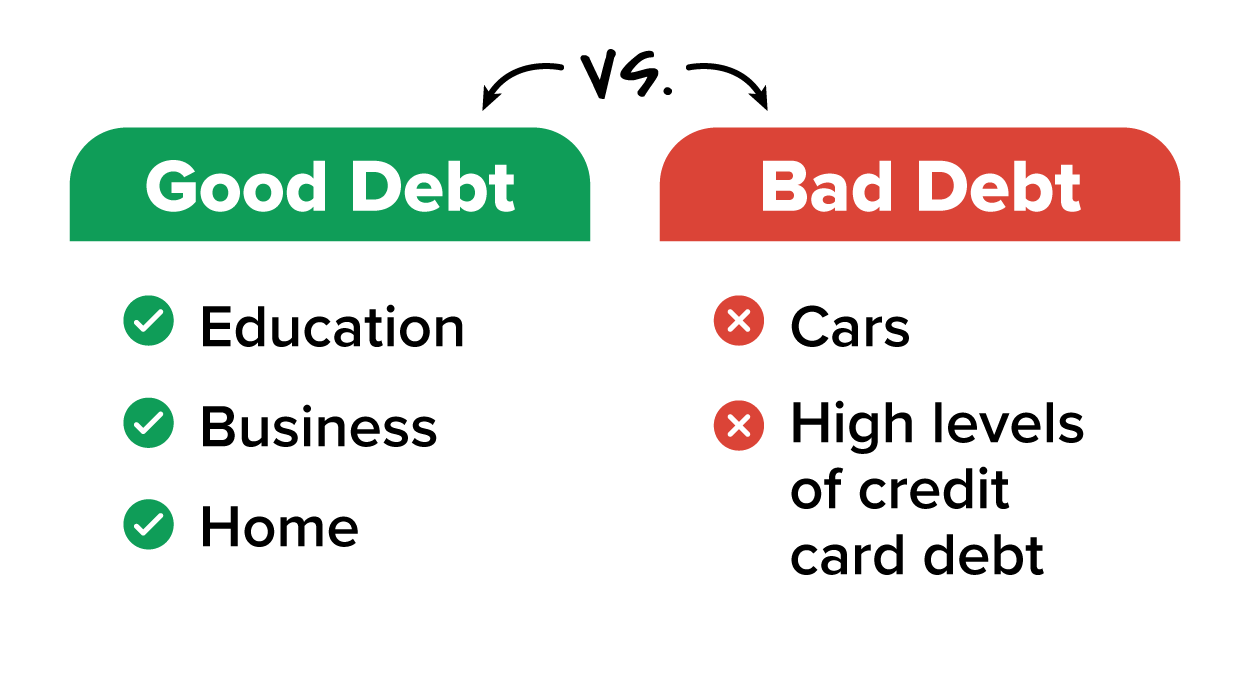

Let’s start by talking about good debt.

Good debt is the kind of debt that can help you move closer to financial freedom. It’s like a tool—a resource you can use to invest in things that will provide value or income over time. With good debt, you’re not just borrowing money for immediate gratification. Instead, you’re making a strategic choice to leverage debt in a way that helps your financial future.

Think of good debt as a friend—a financial partner that supports your journey to the Land of Wealth. But like any friendship, it only works if you handle it responsibly. Let’s look at some examples of good debt, why they’re useful, and how to handle them wisely.

Good debt might sound like an odd idea—after all, most of us think of debt as something to avoid. But certain kinds of debt can actually be a smart way to reach your goals, helping you get ahead rather than holding you back. Let's discuss three (3) examples of good debt.

1. Student Loans: Education as an Investment

Student loans, as you learned about in a previous lesson, are often considered good debt because they’re an investment in your future income. By borrowing to pay for a degree or vocational training, you’re gaining skills and credentials that can help you earn more over your lifetime. For example, data show that people with college degrees tend to make more money over their careers than those without. However, this only holds true if the degree you pursue has strong earning potential in the job market.

Imagine you take out a student loan to get a degree in a field with strong job prospects. This loan is an investment in yourself—helping you gain skills, qualify for better-paying jobs, and increase your income over time. Here’s why education debt can be considered good debt:

2. Home Mortgages: Building Equity Over Time

A home mortgage is often the largest debt people take on, but it’s generally considered good debt because it allows you to invest in a tangible asset—a home. Over time, real estate can appreciate in value, meaning your home could become more valuable than what you paid for it. Additionally, as you pay down your mortgage, you build home equity, which is the cash value portion of the home you own outright. In a future lesson, we will talk about home mortgages and make sure you have everything you need to make a smart home mortgage decision.

3. Business Loans: Fueling Your Potential

Many successful business owners take on debt, known as a business loan, to start or grow their businesses. A business loan is money that a bank or lender gives you to help start or grow your business. You agree to pay it back over time, with interest, through regular payments, just like a personal loan. Businesses use these loans for things like buying equipment, hiring employees, or creating product lines. The goal is to use the loan to help the business make more money so it can pay back the loan and continue to grow.

Now that we’ve looked at how good debt can help you build wealth, it’s time to explore the other side of the coin: bad debt.

So, let’s dive in and see what makes certain types of debt bad and why they can hold you back rather than help you move forward.

The Wealth-Draining Trap

We can’t talk about good debt without talking about its nemesis, bad debt. Bad debt, on the other hand, is like that friend who always encourages you to buy things you don’t really need—and then leaves you holding the bill. Unlike good debt, which can help you reach your goals, bad debt is usually tied to things that lose value fast or don’t help you financially in the long run. It often comes with sky-high interest rates, so you end up paying way more than you borrowed. You’ve already learned the impacts that high interest can have on your budget and financial goals. Instead of moving you forward, bad debt keeps you in a loop of payments, making it tough to save, invest, or get ahead. It’s the kind of debt that feels easy to get into but hard to escape.

Think of bad debt as a financial trap. It can feel appealing in the moment, but it often leads to more stress and fewer options down the road. It’s time to explore the different types of bad debt.

When it comes to debt, some types can feel like quick fixes but actually end up costing you big time. Let’s break down three (3) types of bad debt that can sneak up on you and keep you stuck so you know exactly what to avoid.

1. Credit Card Debt for Nonessential Purchases

You’re already a pro at all things related to credit cards, but let’s look again at them through the lens of bad debt. Credit cards make it easy to spend on things we want now and pay later for everything from clothes to dinners out and more. But credit card interest rates can be sky-high—sometimes over 20%! When you carry a balance from month to month, you’re not only paying back what you spent but also paying extra for the privilege of borrowing.

Let’s review a few pointers on how to avoid credit card debt from turning into bad debt:

EXAMPLE

Imagine this: You see the perfect outfit online, a bit pricey, but you grab your credit card, thinking you’ll pay it off later. Fast-forward to a month, the bill arrives, and you can only make the minimum payment. With a 20% interest rate, that $300 outfit starts costing a lot more, eating into money you could be saving or putting toward other goals. Over time, these little splurges add up, leaving you paying off old purchases instead of moving forward on your big dreams, like that vacation, a new home, or simply having a financial cushion.2. Car Loans for Expensive Cars

Cars lose value quickly, meaning the moment you drive a new car off the lot, it’s worth less than you paid. It’s all a bit depressing, but it’s important to know that buying a car isn’t considered an investment. Taking out a large loan for a luxury vehicle can be especially dangerous because you’re often left with a high monthly payment for something that doesn’t retain value. In a future lesson, you’ll learn how to calculate how much you can actually afford for a car so you can avoid your car loan turning into bad debt.

3. Payday Loans

A payday loan is like borrowing a small amount of cash to cover bills or other urgent expenses when you’re tight on money and need a quick fix until your next paycheck. It’s usually a few hundred dollars, and you’re supposed to pay it back in full when you get paid.

At first, it seems helpful—fast cash to get you through a tough spot. But here’s the catch: Payday loans come with sky-high fees and interest, sometimes over 400%. This means if you can’t pay it all back right away, that small loan grows fast. Before you know it, you’re stuck paying back way more than you borrowed, and some people end up needing another payday loan just to keep up. It’s a cycle that can be really hard to break and makes it even tougher to get back on track financially.

EXAMPLE

Pretend it’s a week before payday, and your car breaks down. You need $300 for the repairs, but you don’t have enough in your bank account to cover it. You’ve got work and other responsibilities, so fixing the car is urgent. You decide to take out a payday loan for $300, figuring you’ll pay it back when you get your paycheck next week. Quick cash, problem solved—right?Now that we’ve explored how bad debt can drain your finances and hold you back from reaching your goals, it’s clear why it’s essential to avoid debt that works against you. But not all debt is bad, and some types can actually help you build wealth and achieve financial security as you’ve learned. The key is knowing how to tell the difference. So, how can you decide if the debt you’re considering is good or bad? Let’s discuss below.

When you’re thinking about taking on new debt, it’s easy to feel a bit uncertain. Is this debt going to help you move forward, or could it end up holding you back? The good news is that with a few simple questions, you can figure out whether the debt you’re considering will be wealth building or not. Let’s dive into three (3) questions to help you decide if this debt will work for you or against you on your journey to financial freedom.

1. Will This Debt Help Me Make Money or Build Wealth in the Future?

EXAMPLE

If you’re taking out a student loan for a degree that’s in demand, that investment could open up job opportunities and increase your earning potential. This type of debt can be a stepping stone to a more secure financial future.A big question to ask yourself is whether what you’re borrowing for will appreciate (go up in value) or depreciate (go down in value) over time.

IN CONTEXT

Here’s a quick checklist to use as a way to decide if debt is good or bad. Before you borrow, ask yourself these questions:

If you can answer “Yes” to these questions, the debt you’re considering is more likely to be good debt—debt that works for you, not against you. But if you’re borrowing for something that won’t grow in value, has a high interest rate, or won’t benefit your financial future, you may want to rethink it.

- Will this debt help me earn more money or build wealth (e.g., education or business investment)?

- Is the interest rate affordable, so I’m not paying way more than what I borrowed (e.g., low-interest student loan vs. high-interest credit card)?

- Will what I’m buying grow in value or at least hold its worth (e.g., a house or investment vs. a luxury car or shopping spree)?

By asking these questions, you’re making sure your debt decisions align with your bigger goals. Good debt can support your financial plan, while bad debt often pulls you further from it. It’s all about borrowing with intention and keeping your eyes on the future.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.