For Tax Year 2021, the Child and Dependent Care Credit was very different. Part of the credit was refundable and the qualified expense limits were much higher. If you find that you have to do a 2021 tax return, some research will be needed.

When determining the amount of the Child and Dependent Care Credit, a specific percentage is applied based on the taxpayer’s adjusted gross income. The percentage is not automatically applied to the total amount paid for the care. Instead, the percentage is applied to the smallest of the following three amounts:

EXAMPLE

Jon (3) and Fred (12) are each a qualifying child dependent for their parents, Mark and Susan. Mark and Susan paid $7,500 in child care expenses for Jon. They incurred no child care expenses for Fred. Because Jon and Fred are both qualifying persons for purposes of the credit, Mark and Susan’s Child and Dependent Care Credit for 2022 will be based on $12,000.The lines on Form 2441, Child and Dependent Care Expenses, are, for the most part, self-explanatory. Those that require a bit of added explanation are discussed below.

The IRS provides Form W-10, Dependent Care Provider’s Identification and Certification, to assist taxpayers in obtaining information from child care providers. The taxpayer should direct the provider to complete Form W-10 or a similar document to provide the necessary information to the taxpayer.

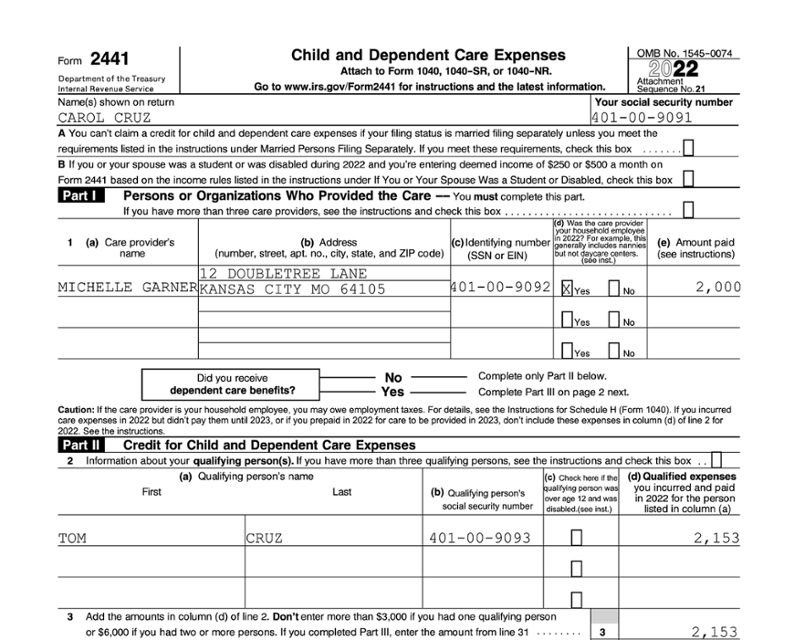

Part I, Line 1. Taxpayers must report the care provider’s name, address, and identifying number (Social Security number for an individual or employer identification number for a business). If the care provider is a tax-exempt organization (a church, for example) and they do not provide a number, enter "Tax-exempt" in column (c). Enter the total amount actually paid to each institution or individual in column (e).

The IRS can use the information on line 1 to match what the taxpayer paid the care provider with the amount the care provider reports as income on their tax return. Therefore, all amounts actually paid to the care provider (by the taxpayer, their employer, or anyone else) during the year must be entered on line 1. If an expense has been incurred, but not yet paid to the care provider, the amount would not be reported on line 1. Line 1 should only report amounts actually paid to the care provider.

If the taxpayer pays Social Security, Medicare, and other payroll taxes for a child care provider’s services within their home, those amounts would not be listed on line 1, because they were not actually paid to the child care provider. These amounts would, however, be entered in Part II, column (d) of the total qualified expenses for each qualifying person.

Part II, Line 2. On this line, enter the name and Social Security number of each qualifying person for whom care was provided, as well as the amount incurred and paid during the taxable year for the care of each person. If there are more than three qualifying persons, attach a statement.

Part II, Line 3. Taxpayers report the total amount of allowed expenses. This amount cannot exceed $3,000 for one qualifying person or $6,000 for two or more qualifying persons.

EXAMPLE

Carol Cruz hired Michelle Garner to come to her home to care for her five-year-old son while Carol worked. She paid Michelle $2,000 (exclusive of Michelle’s portion of Social Security and Medicare taxes as an employee) during the year. In addition, Carol paid the federal government $153 as the employer’s share of Social Security and Medicare taxes. Carol should enter only $2,000 in column (e), line 1, because that’s the amount that is income to Michelle, even though the full $2,153 expense qualifies for the Child and Dependent Care Credit and would be entered in column (d), line 2.

Often, the total of the amount on line 1 (total paid to providers), and the amount on line 2 (qualified expenses), will be the same, but not always, as illustrated in the previous example. Also, line 2 can be different from line 3 (total allowed expenses), because line 3 cannot exceed the maximum amounts ($3,000 for one qualifying person or $6,000 for two or more qualifying persons).

Another situation where the amount on line 3 might not be the same as the total from line 1 is if the taxpayer’s employer paid any portion of the child care expenses and excluded the amount from income. In such a case, the amount to be entered on line 3 is determined by completing Form 2441, Part III. We will defer discussion of these benefits for the moment and return to them when we discuss employer-provided benefits later.

Earned income includes:

Earned income does NOT include:

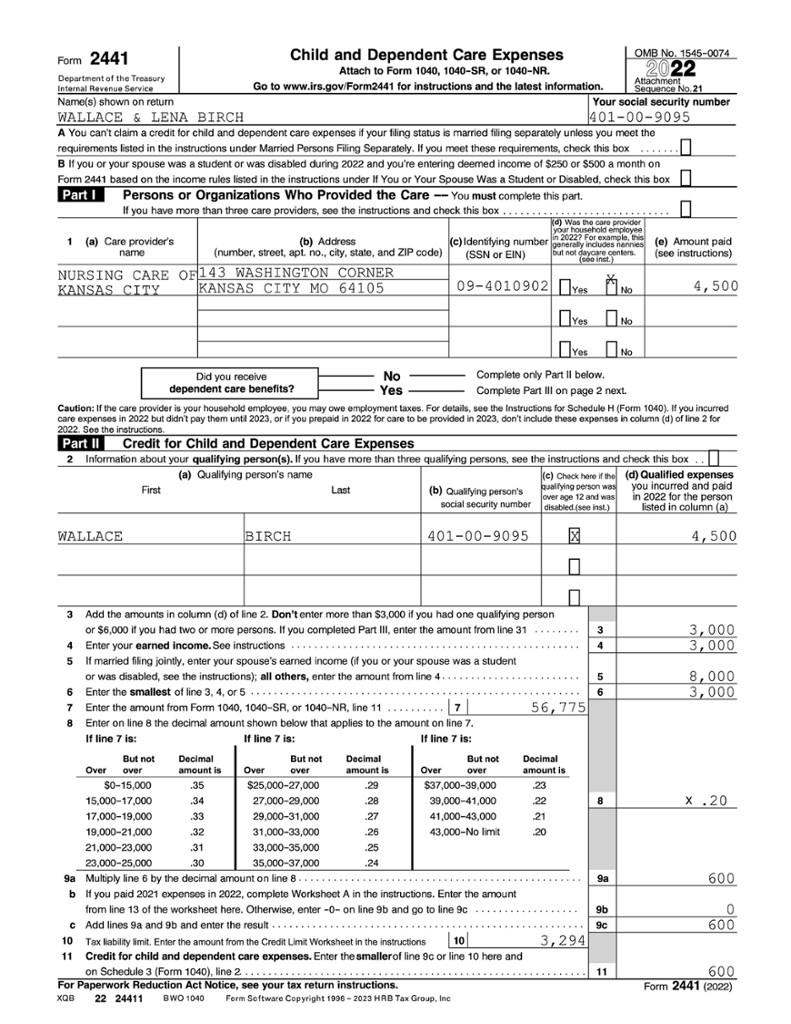

Part 2, Line 4. Enter the primary taxpayer’s earned income on line 4. The primary taxpayer is the one named first in the heading on the first page of the tax return.

Part 2, Line 5. If the taxpayer is filing a joint return, enter the spouse’s earned income on line 5. Otherwise, enter the amount from line 4 on line 5. This is important because the credit is based on the lower of lines 3, 4, or 5. If the taxpayer is unmarried and line 5 is left blank, it would be counted as zero and would be the lowest of lines 3, 4, and 5, resulting in no credit. However, if unmarried and the taxpayer’s earned income is again entered on line 5, the credit will be based on the lower of the taxpayer’s earned income or the line 3 amount.

Student or disabled. If the taxpayer or the spouse was disabled or was a qualified full-time student, multiply the number of months the taxpayer or spouse met such a condition by $250 ($500 if two or more qualifying persons are listed on line 2). Add the result to any earned income from other months, and enter the total on line 4 or 5. Only one spouse may use this adjustment in any given month.

The student or disabled exception of using $250 or $500 per month for the income of the taxpayer or spouse is ONLY available when filing a joint return. An unmarried full-time student with no earned income would not be eligible to claim the Child and Dependent Care Credit.

EXAMPLE

Wallace and Lena Birch file jointly. Wallace is disabled and incapable of self-care. He received Social Security benefits, but received no earned income. Lena was a full-time student through May, and she worked part-time through the end of the year, earning $8,000. The remainder of their income was from investments.

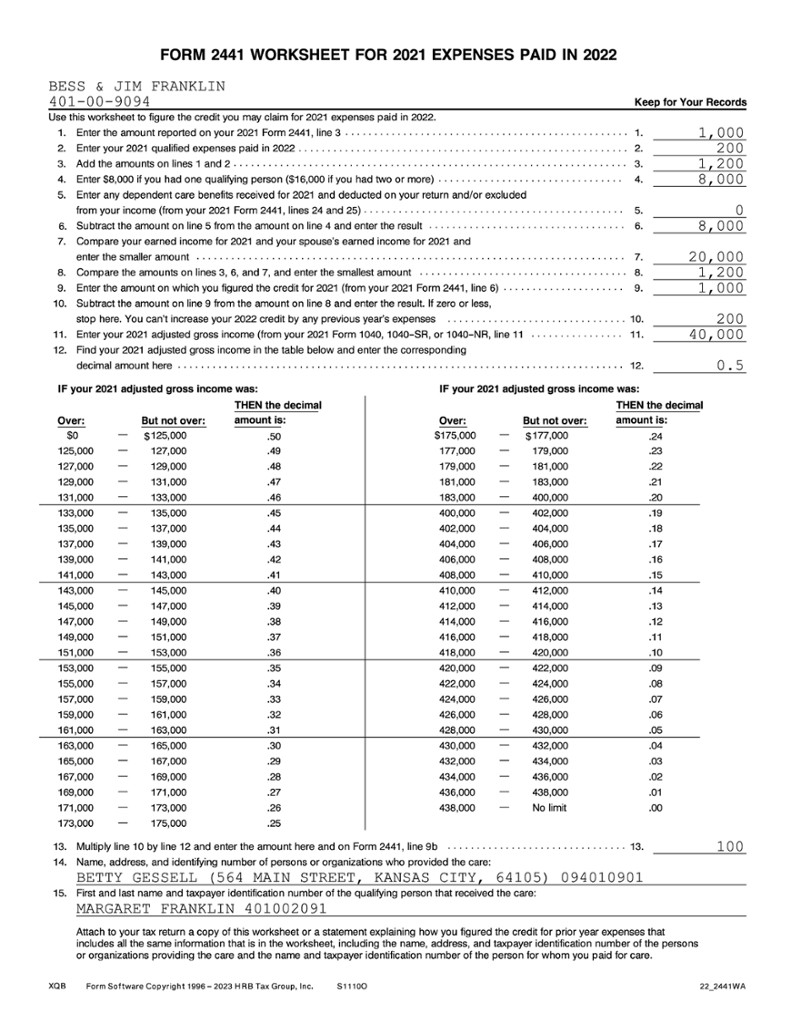

If the taxpayer paid qualified expenses in 2022 that were incurred in 2021, they must figure that portion of the credit using Worksheet A, Worksheet for 2021 Expenses Paid in 2022, in the 2022 Instructions for Form 2441, or a similar worksheet.

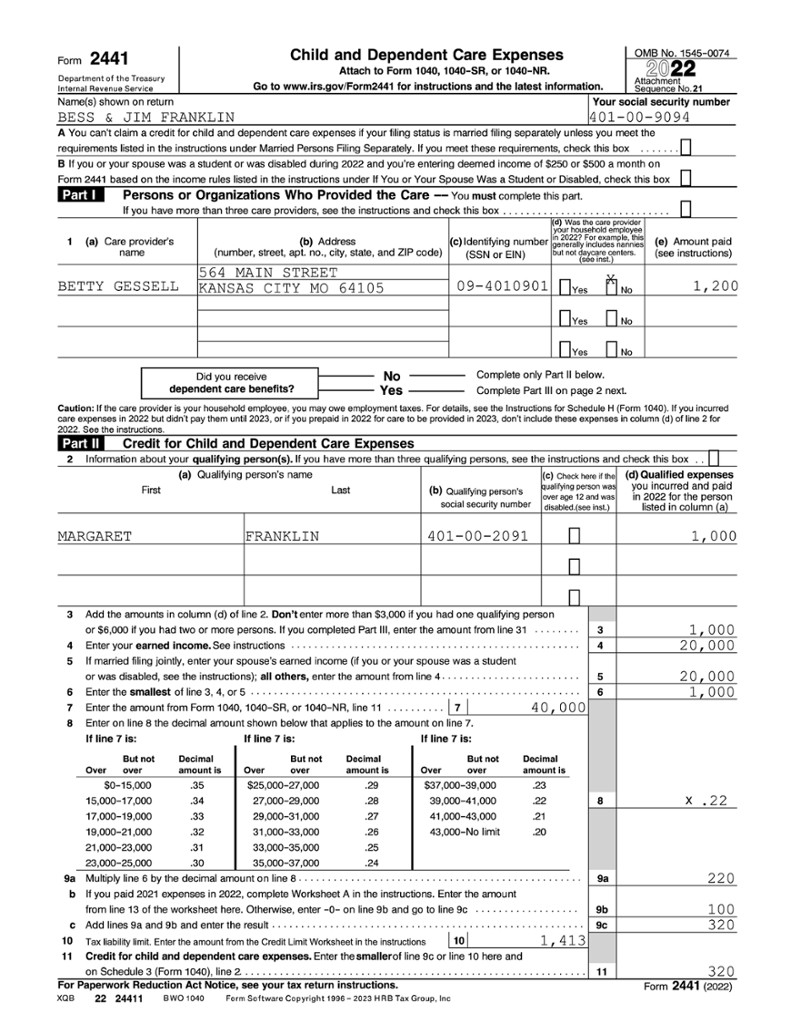

Lines 9a and 9b. For taxpayers that only paid 2022 child care costs, line 9a is the result of multiplying line 6 by the percentage on line 8. However, if the taxpayer paid any prior-year child care in the current year, an adjustment for this line may need to be made.

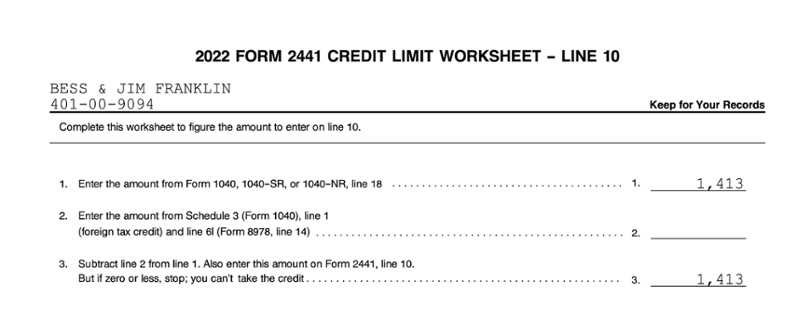

The taxpayer's Child and Dependent Care Credit is a nonrefundable credit that is limited to the taxpayer's tax liability, and any excess is lost. The credit limitation is completed by using the 2022 Form 2441 Credit Limit Worksheet – Line 10 worksheet.

Line 10. The amount from the Credit Limit Worksheet is entered here.

Line 11. The Credit for Child and Dependent Care Expenses is entered on line 11 and carried to Schedule 3, line 2.

EXAMPLE

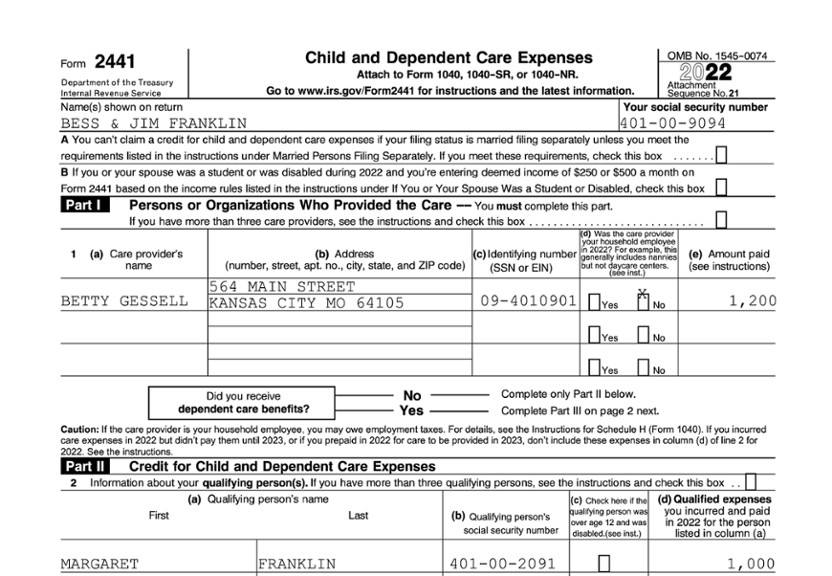

Bess and Jim Franklin paid Betty Gessell $1,200 to look after their three-year-old daughter, Margaret, in Betty's home. Of that amount, $1,000 was for expenses incurred in 2022, and $200 of that amount was for expenses incurred in December 2021 that they paid in January 2022. The Franklins should enter the full $1,200 on line 1, column (e), and $1,000 on line 2(d).