Table of Contents |

For a taxpayer filing an income tax return, once their total income has been determined, they may be allowed certain adjustments. These adjustments reduce their total income, resulting in their adjusted gross income (AGI). Before a taxpayer deducts any of these adjustments from their total income, they would first need to qualify to claim the adjustment.

Some adjustments will be reviewed and presented in this chapter, some only as an awareness topic. Should you encounter a tax return with these items, you will need to perform additional tax research or partner with an experienced tax preparer.

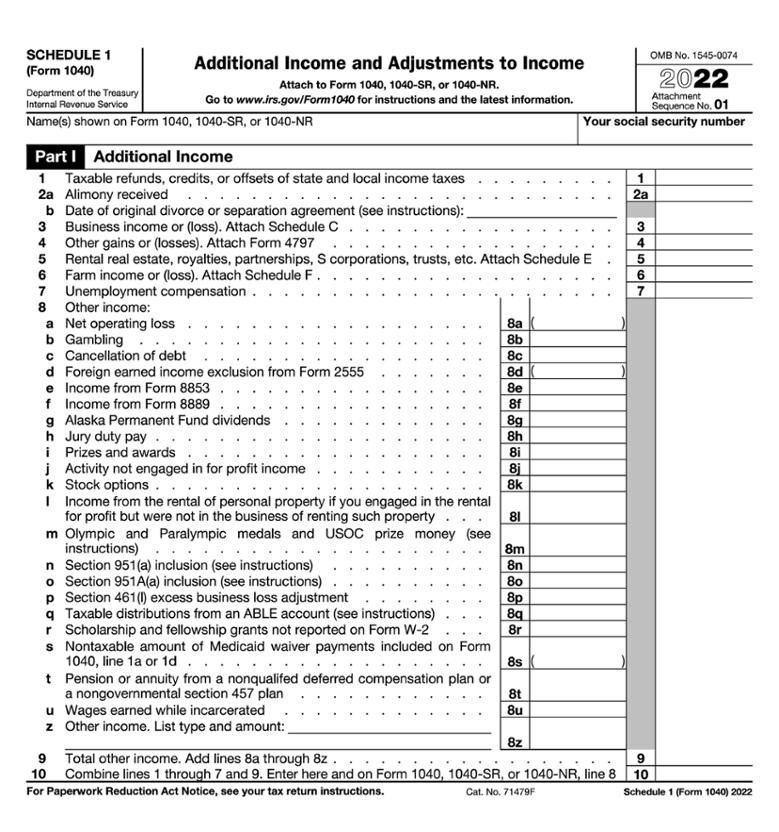

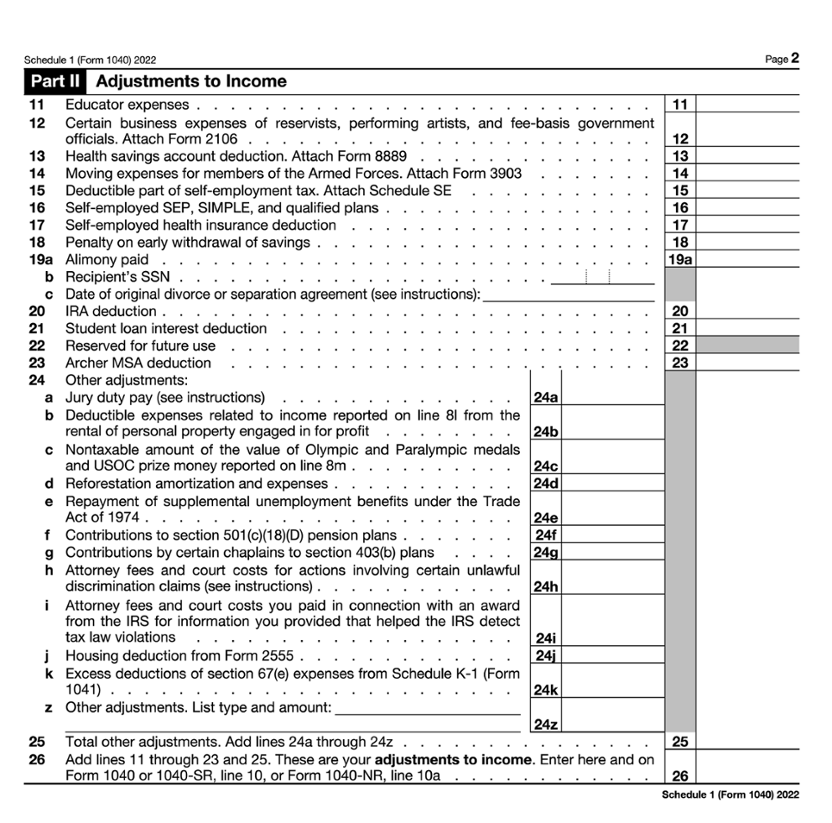

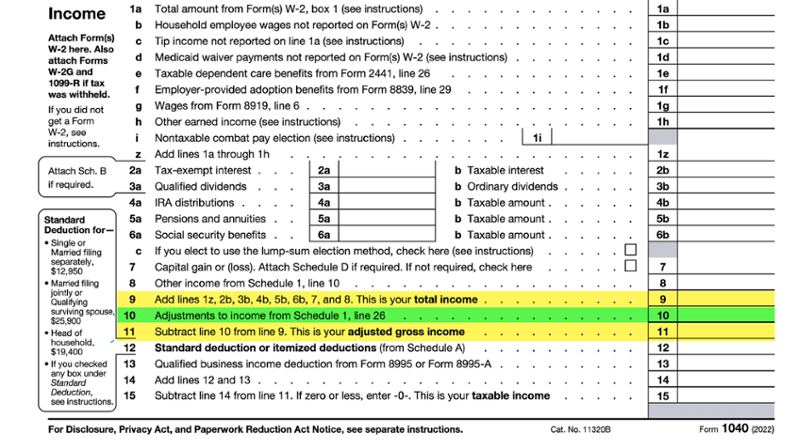

The adjustments to income are entered on Schedule 1 (Form 1040) and subtotaled. The total on line 26 is entered on Form 1040, line 10, and then subtracted from Form 1040, line 9. The result is the taxpayer’s adjusted gross income on Form 1040, line 11.

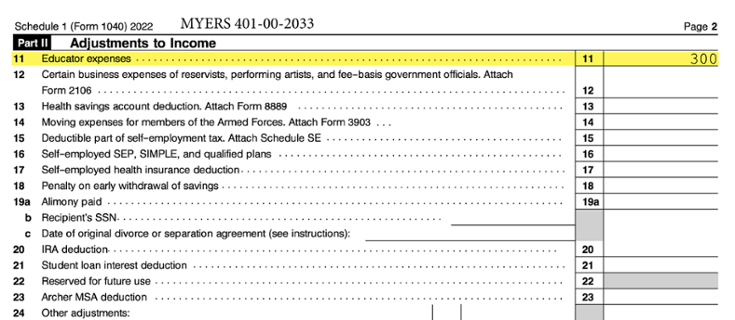

A taxpayer who is an eligible educator may deduct up to $300 of qualified educator expenses paid in 2022; this is done on Schedule 1 (Form 1040), line 11. If the taxpayer and their spouse are filing a joint return and both individuals are eligible educators, their maximum deduction is $600 ($300 per eligible educator).

An eligible educator is someone who worked at least 900 hours during the school year as a teacher, instructor, teacher’s aide, counselor, principal, or administrator physically present in an elementary or secondary school (kindergarten through 12th grade).

Qualified expenses are ordinary and necessary expenses for books, equipment, computer software, classroom supplies, and other supplemental instructional materials and services used in the classroom. This includes expenses for disinfectant, personal protective equipment, and other supplies used for the prevention of COVID-19. Ordinary and necessary means common, accepted, helpful, and appropriate in the taxpayer’s educational field. It does not necessarily mean indispensable.

Expenses for professional development courses, related to what the educator teaches, are also included in qualified expenses as well.

Taxpayers should save receipts and/or other records to substantiate the expenses.

Qualified expenses do not include expenses for homeschooling or for nonathletic supplies for courses in health or physical education.

Qualified expenses must be reduced if the taxpayer or spouse have any:

EXAMPLE

Rita Myers is a fourth-grade teacher. She taught full time during the entire school year. During 2022, she spent $625 on teaching supplies used in her classroom. She did not receive any reimbursements. Rita may deduct $300 of these expenses on Schedule 1, line 11, as an adjustment to income.

EXAMPLE

Melinda is homeschooling her children. She taught full time during the entire school year. During 2022, she spent $1,625 on teaching supplies. Melinda does not qualify for the educator expense adjustment to income because she is not an eligible educator that worked 900 or more hours in a school.