Table of Contents |

Buying a car is a major decision, often one of the biggest purchases you’ll make, so it’s easy to feel overwhelmed. We’ve already covered some important information you need to know, like figuring out how much car you can afford, whether to lease or buy, how to know the true cost of buying a car, and ways to negotiate.

Beyond choosing the right model, understanding financing options, setting a realistic budget, and knowing about postpurchase protections can make a huge difference. This lesson will help you navigate the financial side of buying a car so that you can drive away feeling confident and financially secure.

Before we do that, let’s have a quick refresher on how to budget for your car:

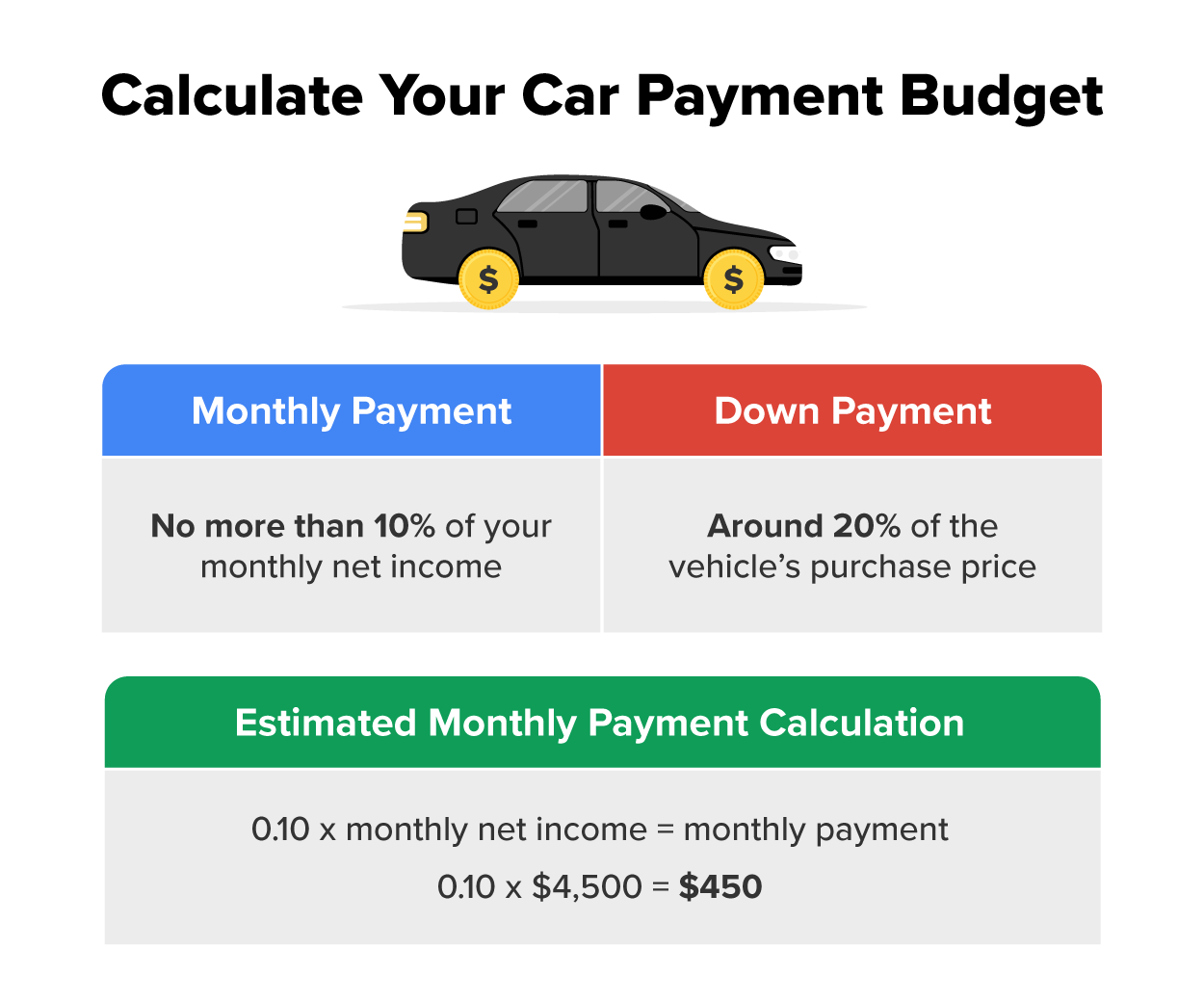

Step 1: Go back to the personal budget that you created. Begin by calculating your monthly income and subtracting essential expenses—like rent, utilities, groceries, and other bills. What’s left is what you could comfortably dedicate to car costs, which include more than just the monthly loan payment.

A common guideline is to keep all car-related expenses (loan payment, insurance, gas, and maintenance) within 10%–15% of your monthly income.

EXAMPLE

Let’s say you’re eyeing a car with a $400 monthly payment, which feels manageable. But after adding insurance, gas, and maintenance, your total car costs are closer to $600—almost double what you initially planned. By choosing a more affordable car with a $250 payment, you’d leave room in your budget for other essentials and avoid feeling financially strapped.Step 2: You’ll also need to save for a down payment. A down payment is the up-front amount you pay when buying a car, which reduces the amount you need to finance it and lowers your monthly payments. Many experts recommend putting down at least 20% of the car’s purchase price, though any amount can help reduce your loan balance and interest costs.

EXAMPLE

Suppose you’re buying a $25,000 car. By putting down $5,000, you’re only financing $20,000 instead of the full amount. Over 5 years at a 5% interest rate, this down payment would save you around $1,500 in interest and lower your monthly payment. It’s one of the simplest ways to keep your total cost down and reduce the amount you’ll need to borrow.Now that you have a feel for your budget and what you can afford, let’s look at some financing options you can consider.

When buying a car, financing is a huge part of the decision. It’s tempting to go with whatever loan the dealership offers, especially when you’re excited to drive your new car home. But the lender and rate you choose can make a big difference in what you pay each month—and over the long run. By checking out a few options beyond the dealership, you can potentially save hundreds or even thousands of dollars.

As we’ve covered before, there are a few main choices you have: dealership financing, banks or credit unions, and online lenders. Each comes with its pros and cons, so let’s break them down to help you find the best fit. Let’s look closer at them each.

EXAMPLE

Let’s say you’re buying a $20,000 car. You find three lenders offering 4.5%, 5%, and 6% interest rates for a 5-year loan. At 4.5%, you’d pay about $3,700 in interest over 5 years; at 6%, it’s $5,200—a difference of $1,500. Shopping around can save you significant money over time, so take your time and don’t settle for the first offer you get.Alright! You’ve chosen which financing option you prefer. Now, let’s look deeper into how factors like interest rates, loan terms, and annual percentage rate (APR) impact your loan.

Understanding how car loans work can help you avoid overspending. Car loans involve factors like interest rates, loan terms, and APR, all of which impact how much you’ll ultimately pay.

Remember what you’ve learned—the interest rate is the cost of borrowing money. A lower rate means smaller monthly payments and less interest over time, while a higher rate leads to larger payments and a higher total cost.

Fixed Versus Variable Interest Rates

| Variable Interest Rates | |

|---|---|

| Pros | Cons |

| Loan terms are flexible. | Interest rates change with the market. |

| You pay less if market rates go down. | You pay more if market rates go up. |

| The initial costs are potentially lower. | Loan payments may fluctuate. |

EXAMPLE

Imagine you borrow $20,000 at a fixed 5% interest rate over 5 years. Your monthly payment would be about $377, and by the end, you’d have paid around $22,620 in total. If you take a loan at 8%, your payment would be about $406 per month, totaling $24,360—a difference of $1,740 over 5 years. This example shows how even a small difference in rates can add up significantly.Loan Terms

Car loans usually range from 36 to 84 months, and the loan term you choose affects your monthly payment and total interest cost. While it might be tempting to choose a long-term loan with a smaller monthly payment, these loans come with higher overall interest costs. We’ve discussed the advantages of shorter-term loans that are 4 years or less, but let’s look at all your options:

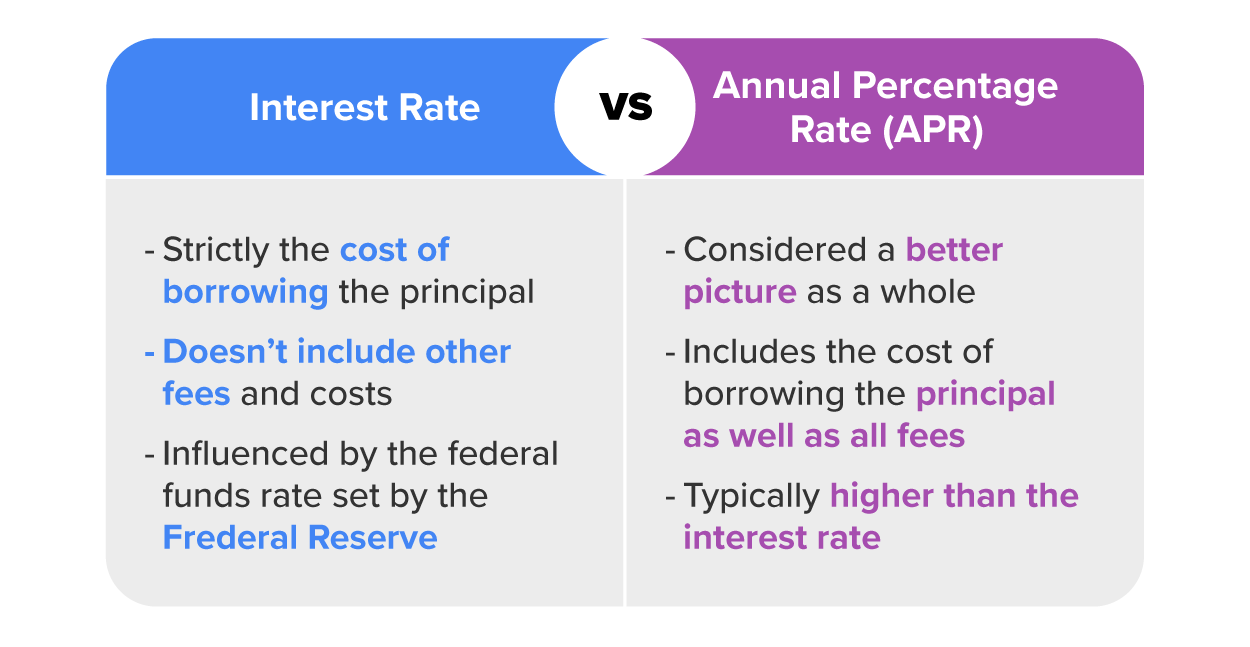

The annual percentage rate (APR) is like the all-in price tag for your loan. While the interest rate shows you what it costs to borrow the base amount, the APR goes a step further by including any extra fees the lender charges, like processing or administrative fees. This way, the APR gives you the full picture of what the loan will cost you over time—not just the monthly payments.

Pretend you’re comparing two loans, each with a 5% interest rate. Loan A has no extra fees, while Loan B has a $500 processing fee. Even though both loans have the same interest rate, Loan B’s APR will be higher because of the added fee. This means Loan B would actually cost you more overall, even though the interest rate looks identical. Be sure to ask the lender directly what the APR is and what extra fees are included so you have that information to make an educated decision when buying your car.

Once you’ve budgeted for your car and found the best loan option, you’re almost ready to hit the road! But there are still a few things to think about after the purchase to keep your car running smoothly and protect your investment. Understanding warranties, lemon laws, and routine maintenance will help you avoid unexpected costs and keep your new car in top shape.

Once you’ve driven off the lot, the process doesn’t just end there. It’s important to understand the protections available to you in case something goes wrong with the car. Having a reliable vehicle is key, and warranties and lemon laws are there to help keep things smooth after your purchase.

Warranties

Most new cars come with a manufacturer’s warranty, which covers certain repairs for a set period, like 3 years or 36,000 miles. We covered this in a previous lesson, but let’s review it. The warranty is like a safety net for unexpected issues, as it can save you from paying out of pocket if something breaks down early on. Some warranties even cover things like roadside assistance or free oil changes, giving you extra perks during the first years of ownership.

For used cars, dealerships sometimes offer limited warranties or certified pre-owned (CPO) warranties if you’re buying a CPO vehicle. These can provide some added security, but the coverage might not be as extensive as a new car warranty.

Extended warranties are another option you might be offered, especially for used cars or once the original warranty expires. While they can add to the cost, they provide continued coverage for specific repairs, which might be worth it if you plan to keep the car for a while or if it’s a model known for higher maintenance costs. Just be sure to read what’s actually covered in an extended warranty, as they vary widely, and consider if it fits your budget and needs.

Lemon Laws

Most states have lemon laws that protect car buyers if they end up with a vehicle that has serious, repeated issues. If your new or, in some cases, used car has a defect that can’t be repaired after several attempts, it might qualify as a lemon. Lemon laws vary by state, but generally, if a car’s problem affects its safety, value, or usability and the dealer or manufacturer can’t fix it within a reasonable time frame, you may be entitled to a replacement, refund, or compensation.

Routine Maintenance

Even with a warranty, routine maintenance is your responsibility, and it’s essential to budget for it. Oil changes, tire rotations, brake pad replacements, and other regular upkeep keep your car running smoothly and help it hold its value. Some people set aside a small amount each month as a car maintenance fund to cover these routine costs without dipping into other savings.

When the warranty runs out, being proactive with repairs and maintenance becomes even more important. Regular check-ups can help catch small issues before they turn into bigger, more expensive problems. Plus, keeping your car well maintained not only saves money but also helps if you plan to sell or trade it in the future.

Taking the time to understand your protections—like warranties and lemon laws—not only gives you peace of mind but also saves you from potential headaches down the road. Staying on top of routine maintenance means fewer surprises and a smoother ride, helping you keep your car running like new. With these steps in place, you can enjoy your car worry-free and focus on all the adventures that lie ahead.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE