Table of Contents |

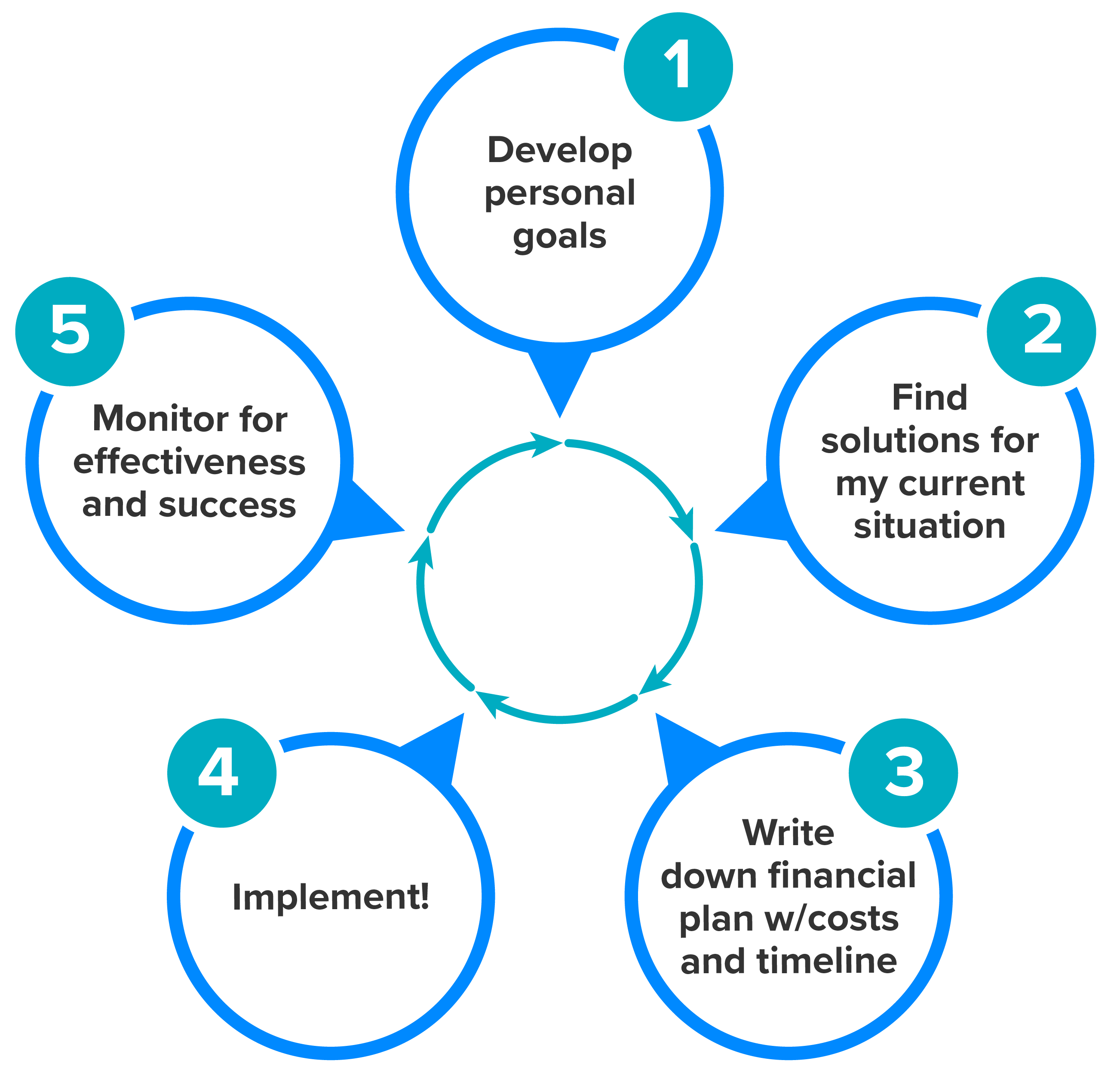

Businesses aren’t the only entities that need financial planning! For life success, personal financial planning is key. First, let’s look at the steps involved in personal financial planning.

The first step is to assess your current financial situation by reviewing your income, expenses, assets, and liabilities. This gives you a clear picture of your net worth and cash flow. Net worth is the value of all of your assets minus your liabilities (the money you owe). Once you understand where you stand financially, the next step is to set financial goals.

After setting your goals, you should create a budget that outlines your monthly income and expenses. A good budget includes savings and debt repayment as essential components and helps ensure that you are living within your means. Developing a savings and investment plan is another key part of financial planning. This includes building an emergency fund, saving for major life events, and investing to grow your wealth over time. Managing debt is equally important; by identifying all your debts and using strategies such as the snowball or avalanche method, you can pay them down more effectively.

In addition to managing money and investments, it’s crucial to protect yourself and your assets. This involves evaluating your insurance needs—such as health, auto, life, and homeowners or renters’ insurance—and setting up basic estate planning documents such as a will or power of attorney. Finally, financial planning is not a one-time task. It requires regular monitoring and revision to reflect changes in your life, such as a new job, marriage, or unexpected expenses. Staying flexible and proactive will help ensure that your plan continues to support your financial well-being over time.

IN CONTEXT: Ren Creates a Financial Plan

Let’s suppose Ren, a marketing professional, is going to look at the financial planning process. They start by reviewing their financial situation. They calculate their monthly income of $5,000 and list all their monthly expenses—rent, utilities, groceries, transportation, and entertainment—which total around $3,800. Ren also lists their assets, including their savings account, a small investment account, and their car. Their liabilities include a car loan and a few thousand dollars in credit card debt. After calculating their net worth and understanding their cash flow, Ren realizes they have about $1,200 left each month that they could be using more wisely.

Next, Ren sets their financial goals. Their short-term goal is to pay off their credit card debt within a year. Their medium-term goal is to save $10,000 for a down payment on a home within the next 3 years, and their long-term goal is to retire comfortably at age 65. With these goals in mind, they create a detailed monthly budget. They allocate $500 toward debt repayment, $300 toward their emergency savings, $200 toward their home down payment fund, and $200 for discretionary spending.

To build financial security, Ren sets up automatic transfers into a high-yield savings account for their emergency fund and opens a Roth IRA to begin investing for retirement. They also increase their 401(k) contribution at work to take full advantage of their employer’s match. To tackle their debt, they use the avalanche method, paying off the highest interest credit card first while making minimum payments on the rest.

Now that you have a budget in place, we can look at how to plan for a large purchase, such as a new computer, a car, or a vacation.

The first step is to develop financial goals. First, what do you really need? If you’re looking for a car, you probably need transportation. Before you decide to buy a car, consider alternatives to buying a car. Could you take a bus, walk, or bike instead? Often, one goal can impact another goal. Cars are typically not good financial investments. We have cars for convenience and necessity, to earn an income, and to enjoy life. Financially, they are an expense. They lose value, or depreciate, which means a decrease in value over time.

EXAMPLE

If you buy a car now for $25,000, it may only be worth $18,000 next year. So, buying a car may slow your savings or retirement plan goals.Cars continually use up cash for gas, repairs, taxes, parking, and so on. Keep this in mind throughout the planning process. Or perhaps your goal is to save for a house or a vacation? Determining what you want is an important first step for personal financial planning.

The second step is to determine and evaluate alternatives for reaching your goal. In this step, you will look at your savings, debt, income, and expenses to determine the best course of action. Suppose you have decided to purchase a car, but based on your financial situation, you’ve decided that it makes the most financial sense to purchase a used car. Or, perhaps, instead of a 3-week vacation in South America, you’ve determined you’ll save monthly for that and, for now, take a road trip locally. In every financial decision we make, there are many alternatives that may equally meet our needs and wants, and in this step, you’ll want to consider all alternatives.

The next step is to write out financial goals. Assume that you have decided to buy a used car but also want to purchase a laptop. Here’s how that might look:

| Goal | Item | Details | Budget | Timeline |

|---|---|---|---|---|

| Transportation/car | 2021 Toyota Camry | Black, A/C, power windows, less than 60,000 miles |

Car: $23,000 (max) Down payment: $3,000 Insurance: $100/month Sales tax: $900 Licensing: $145 Cash needed: $4,145 |

Have: $3600 in savings for this. Save: $50/week. Purchase in approximately 11 weeks. |

| Computer | Used or refurbished laptop | Dell with Windows, minimum 13″, 128 GB hard drive, HD graphics |

$300 Use free Windows update from school. Use free Wi-Fi at school. |

Sell current laptop for $100. Buy refurbished from Dell site for $289. $189 on credit card. Pay off when the statement comes. |

The next step is to implement your plan. Once you’ve narrowed down which car you are looking for, do more online research with resources such as Kelley Blue Book to see what is for sale in your area. You can also begin contacting dealerships and asking them if they have the car you are looking for with the features you want. Ask the dealerships with the car you want to give you their best offer, then compare their price to your researched price. You may have to spend more time looking at other dealerships to compare offers, but one goal of online research is to save time and avoid driving from place to place if possible.

Finally, our last step for large purchases is to monitor your plan. Things change, so looking toward the future and constantly monitoring your goals is key to saving and planning for large purchases.

When you take out a loan, you take on an obligation to pay the money back, with interest, through a monthly payment. You will take this debt with you when you apply for auto loans or home loans. Effectively, you have committed your future income to the loan. Some debt is OK, though. Good debt helps you build long-term value and doesn’t depreciate. Bad debt means to borrow money for things that lose value.

EXAMPLE

If I purchase a house, which usually gains value, that would be “good debt.” Paying for an education, since you’d expect to earn more money after getting the education, would also be considered good debt. Bad debt might include borrowing money for a car (although sometimes this is necessary) or spending too much on clothes on a credit card.Let’s see how credit card debt might impact your financial future:

As you can see, using a credit card and only paying the minimum can cost you a lot of money over time! Now, getting a credit card is good for building credit, but it must be used responsibly!

Let’s compare the good and bad practices in managing money:

| Good Practices That Build Wealth | Bad Practices That Dig a Debt Hole |

|---|---|

| Tracking all spending and saving | Living paycheck to paycheck with no plan |

| Knowing the difference between needs and wants | Spending money on wants instead of saving |

| Resisting impulse buying and emotional spending | Using credit to buy more than you need and increasing what you owe |

Click through to understand some ways you can help manage your debt:

Now that we’ve addressed how to budget and learned how to manage debt, let’s look at some of the basic forms of how we can save and invest money.

A 401(k) is an employer-sponsored retirement plan that allows employees to contribute a portion of their pretax income, often with an employer match. One of the biggest advantages of a 401(k) is the tax-deferred growth—it reduces your taxable income now and allows your investments to grow tax free until you withdraw them in retirement. Employer matching is essentially free money, which boosts your savings. However, 401(k)s have limited investment options compared to IRAs, and early withdrawals before age 59½ typically come with a 10% penalty plus taxes.

EXAMPLE

Suppose you work for a company with a 401(k) match, and you decide to put $100 per paycheck in the 401(k). Since your employer matches it, this means you’d be saving your $100 plus the $100 they match, for a total of $200. Employer matching is essentially free money, and you should always take advantage of this.IRAs are another type of retirement account that individuals can open independently. A traditional IRA works similarly to a 401(k) with tax-deferred growth, while a Roth IRA uses after-tax dollars but allows for tax-free withdrawals in retirement. The Roth IRA is especially beneficial for younger investors or those who expect to be in a higher tax bracket later. However, IRAs have lower annual contribution limits than 401(k)s, and depending on the income, not everyone qualifies to contribute to a Roth.

Stocks represent ownership in a company and offer the potential for high returns through price growth and dividends. They are ideal for long-term investors who can handle market volatility. The downside is that stocks can be risky; market downturns can significantly impact your portfolio, especially in the short term. On the other hand, bonds are lower risk investments where you loan money to a government or corporation in exchange for interest payments. They provide more stability but generally offer lower returns compared to stocks.

Mutual funds and exchange-traded funds (ETFs) pool money from many investors to buy a diversified mix of assets, such as stocks and bonds. They are a great option for investors who want diversification without picking individual securities. The main disadvantages can be fees, especially with actively managed funds, and limited control over the specific holdings.

Certificates of deposit (CDs) can be a useful part of a personal investment strategy, especially for conservative investors or those who need a low-risk place to store money for the short to medium term. You can put money in a CD for a set amount of time through your bank and earn interest.

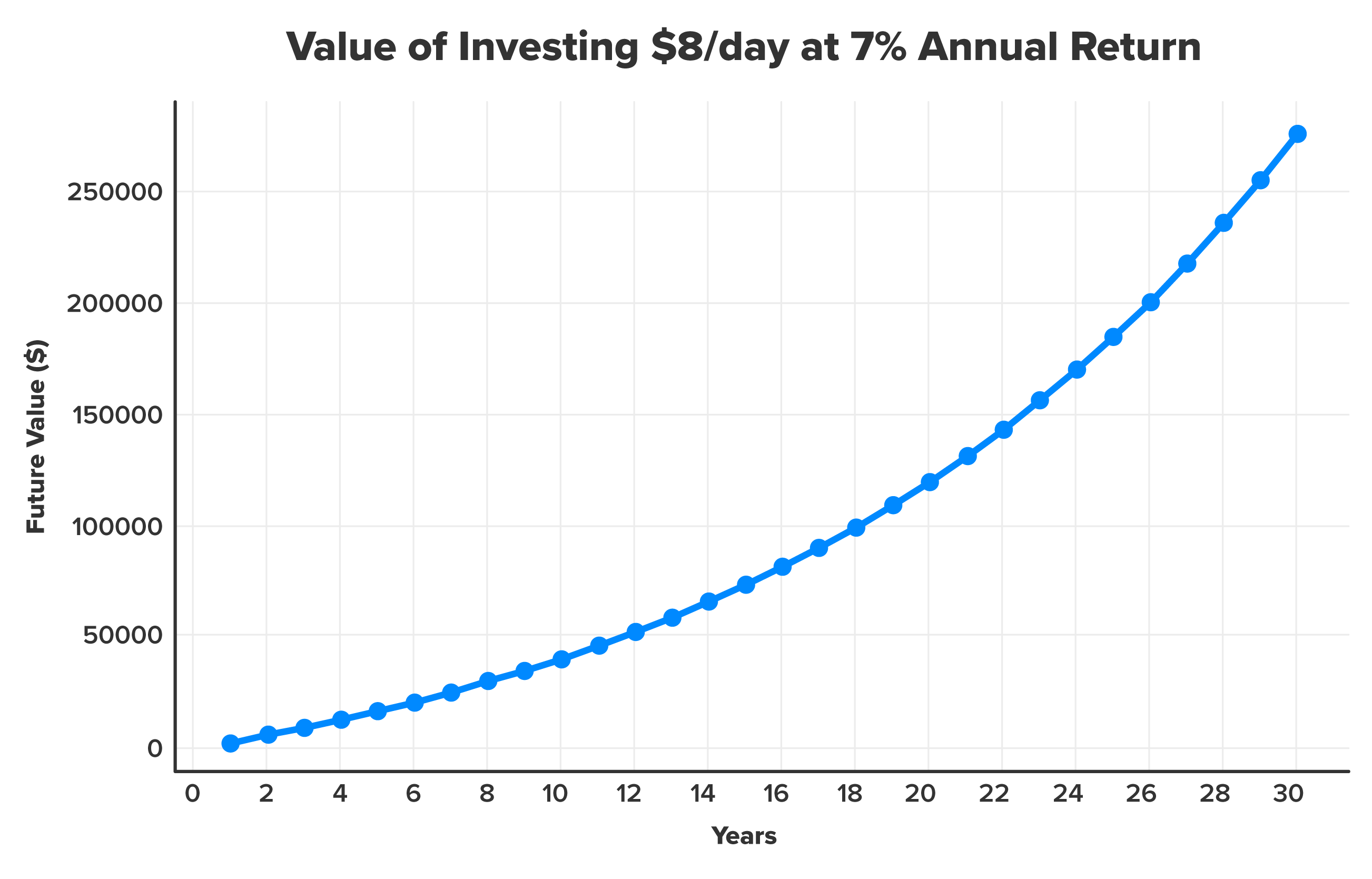

Small changes can make a big difference in financial health. Let’s look at how Ren might use their money differently:

IN CONTEXT: Ren Invests Coffee Money

Assume that Ren spends $8 per day on coffee. What would happen if they invested that money instead?

Basic Assumptions:Step-by-Step Calculation:

- Daily coffee cost: $8

- Annual investment return: 7% (a common average return for the stock market)

- Time frame: 10 years

- Investment frequency: Daily contributions

What If They Do This for 20 Years?

- $8/day × 365 days/year = $2,920 per year

- Invested annually at 7% return over 10 years = future value of about $40,250

- $2,920/year invested for 20 years at 7% = about $123,000

Summary:

If Ren skips the daily $8 coffee and invests that money instead:Moral of the story? Small investments, done wisely, can turn into huge financial opportunities over time!

- In 10 years, they could have around $40,250.

- In 20 years, they could have over $123,000.

- In 30 years, that amount would be $240,000.

Source: THIS CONTENT HAS BEEN ADAPTED FROM RICE UNIVERSITY’S “COLLEGE SUCCESS”. ACCESS FOR FREE AT OpenStax. LICENSE: CREATIVE COMMONS ATTRIBUTION 4.0 INTERNATIONAL.