In this lesson, you will learn about the key players in the financial services industry and how they meet your financial needs. This includes the essential services of banks, growing investments with brokers, and what credits unions can provide. Specifically, this lesson covers the following:

1. Banks

Banks are the most common type of financial institution that you are likely familiar with. Banks are institutions that help you manage the money you earn, spend, and save. Whether you’re getting a paycheck directly deposited into your checking account or applying for a loan to buy a new car, a bank is involved in those transactions. Banks offer services that are essential to your day-to-day financial life, like checking and savings accounts, credit cards, and personal loans.

-

EXAMPLE

Imagine one of your financial goals is to buy a home. You have set a goal of saving $20,000 for your down payment. You walk into your bank and ask them if there is a savings account that will meet your needs. On the spot, you open a savings account and transfer your first $500 into your savings account from your checking account. Your bank also helps you set up automatic transfers from each of your paychecks directly from your checking account to your savings account.

Banks generally come in three types:

-

Retail banks: These are the banks we’re most familiar with, like Chase, Bank of America, or your local credit union where you have your checking and savings accounts. Retail banks offer services for individuals, including checking and savings accounts, credit cards, and personal loans. You can find them as brick-and-mortar banks, which have physical locations you can visit, and online-only banks, like Ally or Chime, that operate entirely through apps and websites.

- Some advantages of brick-and-mortar retail banks:

- They offer face-to-face customer service, ATM access, and in-person support for complicated issues. You also get a sense of personal connection.

- They often offer lower fees, higher interest rates on savings, and convenient digital tools since they save on overhead costs. You can access your account anytime, anywhere.

- Some disadvantages of brick-and-mortar retail banks:

- They usually have higher fees and lower interest rates on savings accounts to cover the cost of maintaining physical branches.

- There is no in-person support, and you might have limited access to ATMs or face delays for certain transactions, like cash deposits.

-

Commercial banks: These banks cater to businesses, helping them manage daily financial operations, get loans, and grow their businesses. Examples include Wells Fargo and HSBC. Although you might not interact with commercial banks directly, they impact the economy and job market. When businesses can access loans and services to grow, they can hire more people, expand their offerings, and ultimately improve the economy.

- Some advantages of commercial banks are that they help businesses of all sizes with financing, managing cash flow, and handling payroll, enabling growth that can boost the economy.

- Some disadvantages of commercial banks are that they typically offer fewer services for individuals and they prioritize larger businesses, so small businesses may face higher fees or stricter loan requirements.

-

Investment banks: These banks serve large companies and governments with complex financial needs, like helping companies go public, raising money, managing large-scale investments, and overseeing when a business is bought or sold. Some well-known investment banks include Goldman Sachs and Morgan Stanley. While we don’t directly interact with investment banks, their activities influence the stock market, large-scale investments, and even job availability in the industries they support.

- Some advantages of investment banks are that they play a crucial role in helping companies grow, which can lead to new products, innovation, and more jobs.

- Some disadvantages of investment banks are that they focus on large-scale profits, which can sometimes lead to economic risks, especially if they take on high-risk ventures or fail to balance their investments responsibly. Additionally, the services they offer aren’t accessible or relevant to the average individual.

Each type of bank has a unique role, with retail banks serving individuals, commercial banks supporting businesses, and investment banks managing large financial deals. Whether you prefer a brick-and-mortar or online bank, each has its own strengths and weaknesses that can influence your banking experience.

-

- Banks

- Financial institutions that hold and manage money for people, offering services like savings accounts and loans.

- Retail Banks

- Provide financial services to individuals and small businesses, such as checking and savings accounts, loans, and credit cards.

- Brick-and-Mortar Bank

- A traditional bank with physical locations you can visit, like branches or ATMs, where you can do things like open accounts, deposit money, or get help from a banker in person.

- Online-Only Bank

- A bank that operates entirely online without physical branches. You manage your account, make deposits, transfer money, and access customer support through a website or app.

- Commercial Banks

- Banks that serve businesses and larger organizations, offering services like business loans, commercial accounts, and payment processing.

- Investment Banks

- Help companies raise money and handle big financial deals, like mergers. They don’t offer regular banking services like deposits.

1a. FDIC Insurance

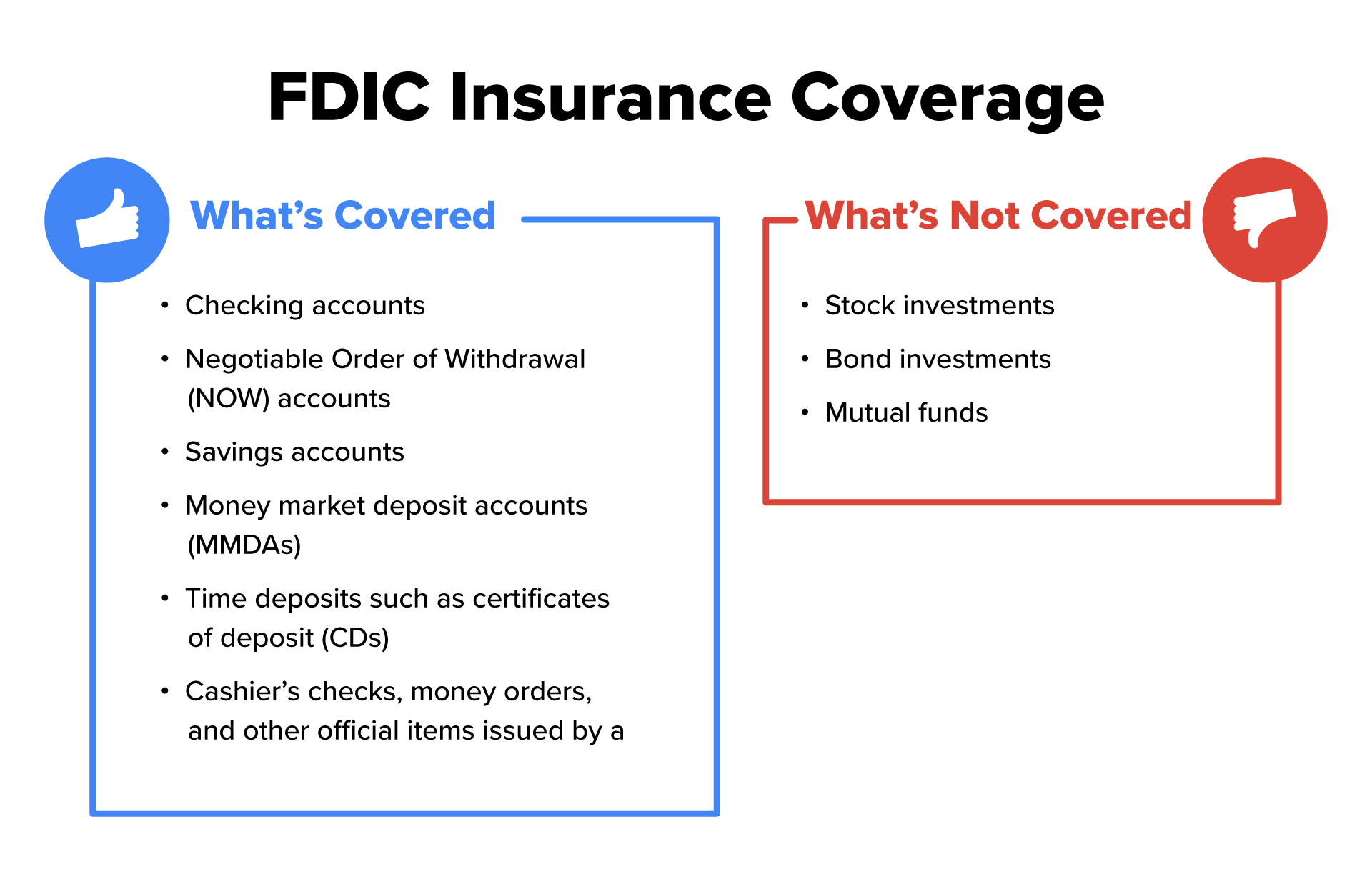

Banks are generally pretty safe places to keep your money, but every now and then, things can go wrong. When banks go out of business (yes, it happens), FDIC insurance kicks in to protect you.

The Federal Deposit Insurance Corporation (FDIC) was created after the Great Depression when many banks and people lost their life savings. Today, FDIC insurance guarantees that if your bank collapses, the federal government will reimburse you up to $250,000 per depositor, per bank. That means that your money is secure and safe as long as you have less than $250,000 in your bank account.

-

If you happen to have more than $250,000, then you may want to consider spreading your money across multiple banks to stay under this threshold.

Here are some examples of historically relevant bank failures where FDIC insurance helped protect customers.

-

Silicon Valley Bank (2023)

Silicon Valley Bank (SVB), known for serving tech start-ups, collapsed in March 2023. The FDIC stepped in to cover insured deposits and later announced plans to cover uninsured deposits, ensuring clients could access their funds.

Signature Bank (2023)

Signature Bank failed shortly after SVB, impacted by similar issues, including large withdrawals and insufficient cash reserves. FDIC insurance protected insured depositors, giving them access to their accounts.

First Republic Bank (2023)

After facing financial difficulties and a sharp decline in deposits, First Republic Bank was taken over by the FDIC and sold to JPMorgan Chase. FDIC insurance protected depositors and ensured continuity of banking services for clients.

IndyMac Bank (2008)

During the financial crisis, IndyMac Bank failed and became one of the largest bank failures in U.S. history at the time. The FDIC insured deposits up to the limit, helping depositors recover their funds amid the turmoil.

It’s important to know that not all banks have FDIC insurance, but it’s smart to choose one that does. Most well-known banks and credit unions offer this protection. Knowing that your hard-earned money is insured helps you feel confident in using the banking system, whether you just have a checking account, are keeping a small emergency fund, or saving up for something bigger, like a house.

Now, let’s take a closer look at what is and isn’t covered by FDIC insurance to make sure you know exactly how your money is protected.

-

EXAMPLE

You’ve been working for years to build an emergency fund, and you finally have $2,000 in your savings account. Then, one day, you hear on the news that your bank is in trouble. Instead of panicking, you know that your $2,000 is insured by the FDIC. The FDIC typically steps in very quickly when a bank fails—usually by the next business day. In most cases, the FDIC either arranges for another bank to take over the failed bank’s accounts or issues a direct payment to depositors. So, if your bank goes under, you can expect access to your insured funds within a few days, helping you avoid a long wait or financial disruption.

-

- FDIC Insurance

- Protects your money in a bank account up to a certain limit (usually $250,000) if the bank fails, so you don’t lose your savings.

2. Brokers

Now that we’ve covered banks and how they keep your money safe, let’s shift to brokers—your gateway to the world of investing. If you’ve ever thought about buying stocks, bonds, or mutual funds, brokers are the ones who make those transactions happen for you.

Brokers are your entry pass to the investment world. If you’ve ever thought about buying stocks, bonds, or mutual funds, you’ll need a broker to make the transaction. Brokers act as intermediaries, helping you buy and sell investments based on your goals and risk tolerance.

There are two main types of brokers:

-

Full-service brokers offer a wide range of services, from investment advice to financial planning and more. They’re great if you want someone to guide you every step of the way as you make investing choices. Of course, all that help comes at a cost, and full-service brokers often charge fees for their professional help.

-

Discount brokers are more of a DIY type of broker. They allow you to make your own trades at a much lower cost. You won’t get personalized advice, but a discount broker is ideal if you’re comfortable doing your own research and managing your investments.

Some popular brokers you might have heard of include Charles Schwab, Fidelity, E*TRADE, Robinhood, and TD Ameritrade. These are the companies that help you buy and sell stocks, bonds, and other investments.

To find the right broker for you, start by checking out reviews on sites like NerdWallet or Investopedia. They break down things like fees, how easy the website or app is to use, and what kinds of investments you can buy. It’s also a good idea to visit each broker’s website to see what they offer, like free educational resources or customer service options. Some even have tutorials or demo accounts so you can test out how it works before you sign up. If you’re still unsure, look for feedback from real people in online forums or social media—sometimes, hearing from others can make a big difference in your choice!

Also, brokers aren’t just for rich people—anyone can have one! Today, many brokers have low or even zero account minimums, meaning you can start investing with just a few dollars. Platforms like Robinhood and Fidelity have made it easy and affordable for everyday people to get into investing. You don’t need to be wealthy to start buying stocks, bonds, or mutual funds; you just need a broker that matches your goals and budget.

-

EXAMPLE

Let’s say you’ve decided it’s time to start investing for retirement. You talk to a full-service broker who helps you identify your investing and retirement goals. For a fee, they help you pick out a combination of stocks, bonds, and mutual funds that will give you the best chance of reaching your goal. If you’re more hands-on, you might decide on a discount broker like Robinhood or E*TRADE, where you can research and trade on your own at a lower cost.

-

If you want to learn more about brokers, here are some resources to help you compare and choose brokers:

- Investopedia’s Best Online Brokers and Trading Platforms: It offers detailed reviews and rankings of various brokers based on fees, investment options, and user experience. Investopedia

- NerdWallet’s Best Online Brokers for Stock Trading: It provides comprehensive comparisons of brokers, highlighting their strengths and weaknesses to assist in making an informed decision. NerdWallet

- U.S. News’ Best Online Brokers: It features evaluations of top brokers, focusing on factors like customer service, fees, and available investment products. Money

- StockBrokers.com’s Best Online Brokers Guide: It offers in-depth analyses and rankings of online brokers, considering aspects such as trading platforms, commissions, and overall user satisfaction. StockBrokers.com

These resources can help you assess different brokers to find the one that best fits your investment needs and preferences.

-

- Full-Service Brokers

- Financial professionals who provide personalized investment advice, research, and manage investments for clients, often at a higher cost than discount brokers.

- Discount Brokers

- Companies that let you buy and sell investments at a low cost but offer limited or no personalized advice.

3. Credit Unions

Now that you understand the roles brokers play in your finances and how they help you invest, let’s switch gears and talk about credit unions. While brokers connect you to the investment world, credit unions focus on your everyday banking needs—often with a more personal touch and some unique benefits compared to traditional banks.

-

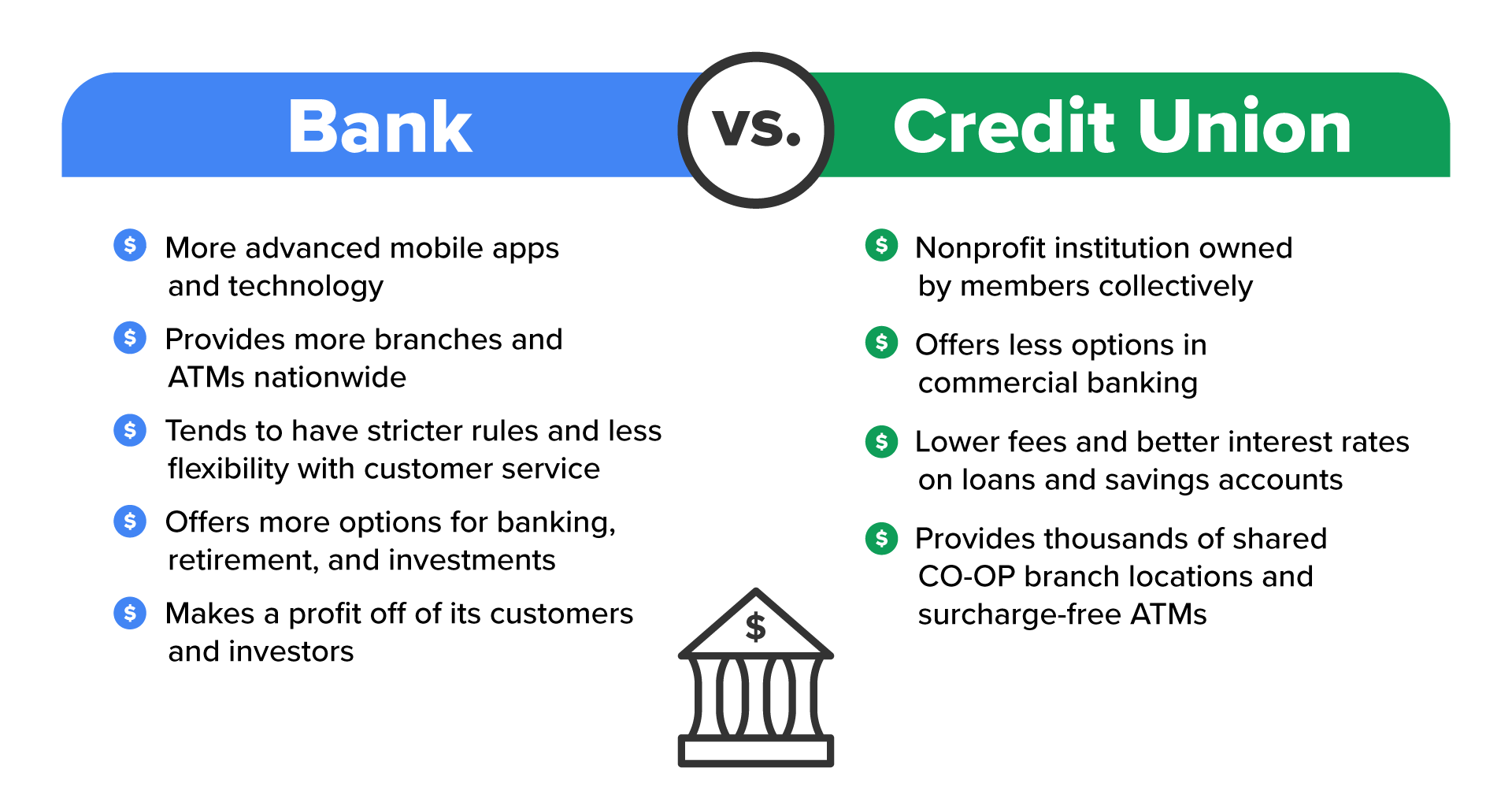

Credit unions are a lot like banks, but with a key difference—they’re not-for-profit organizations that are owned by their members. That means when you join a credit union, you’re not just a customer—you’re actually a part owner of the credit union. Credit unions usually offer lower interest rates on loans and credit cards because they’re owned by their members—you! Instead of aiming for big profits, they focus on giving back to members with better rates and fewer fees. This member-first setup helps keep costs low, so they can pass the savings directly to you.

However, credit unions aren’t open to just anyone. You must be part of a specific group, like employees of a company, members of an organization, or students or alumni of a university. If you qualify, though, joining a credit union can be a smart way to meet your money goals. They also tend to offer more financial education and support, which can be incredibly helpful if you’re trying to build good financial habits.

Here are some interesting facts about credit unions to help you understand them more and to explain why they are so special.

1. Why Can Some People Not Join a Credit Union?

Credit unions often serve specific groups of people, like employees of a particular company, members of an organization, or residents of a specific area. This is called a field of membership, and it’s why not everyone can join every credit union. However, many credit unions have expanded their membership criteria, so there’s likely one you qualify for based on where you live or work or your affiliations.

2. What Happens If a Credit Union Fails?

If a credit union fails, members’ deposits are protected by the National Credit Union Administration (NCUA), similar to how the FDIC insures deposits at banks. The NCUA insures up to $250,000 per account holder, so even if the credit union goes under, you’ll still get your money back.

3. Why Did Credit Unions Come Into Existence?

Credit unions were created as a way for people in specific communities or workplaces to pool their money to help each other out financially. They were designed to give people, especially those who might not have easy access to traditional banks, a safe place to save and borrow at fair rates. The idea behind credit unions is all about helping members rather than making a profit.

4. How Many Banks Versus Credit Unions Are There?

In the United States, there are around 4,000 commercial banks and 5,000 credit unions. Credit unions are popular with people looking for lower loan rates and higher savings rates, which is why they’re found in so many communities across the country.

5. Why Are So Many Credit Unions Called “CU”?

Many credit unions use CU in their names (like ABC CU) because it stands for “credit union.” It’s an easy way to identify them and separate them from traditional banks. The CU in the name reminds people that they’re joining a cooperative focused on serving members, not just another financial institution.

Here’s a further breakdown of a credit union versus a bank.

-

You’re ready to buy a new car, and you’re shopping around for a loan. You really aren’t sure what loan is best for you. Your traditional big bank is offering a 5% interest rate, but your local credit union—where you’re a member—is offering just 3.5%. That difference could save you hundreds or even thousands of dollars over the life of the loan. Not to mention, the credit union helps you find the right car loan to meet your budget needs, giving you truly personalized service. Based on what you’re looking for—like saving money, getting better support, or banking somewhere that cares about your community—you might decide a credit union is the best fit for your loan. For example, if you’re focused on keeping monthly payments low, credit unions often offer lower interest rates than banks, which can really help with affordability. Or, if you want a more personal touch, credit unions are known for friendly, one-on-one service that makes you feel like a valued member, not just an account number.

You might also appreciate the flexibility they offer with loan terms or access to financial advice that’s easy to understand. And if supporting local causes matters to you, many credit unions are deeply connected to their communities, so your money helps make a difference. Choosing a credit union can mean lower costs, better service, and the chance to bank somewhere that shares your values—so it’s a win-win all around.

-

- Credit Union

- A nonprofit bank owned by its members, offering services like loans and savings with low fees and good rates.

- National Credit Union Administration (NCUA)

- A U.S. government agency that regulates and insures federal credit unions.

In this lesson, you learned about the key players in the financial services industry—banks, brokers, and credit unions—and their roles in helping you manage, grow, and protect your money.