A taxpayer must file a tax return if they meet certain filing requirements. These requirements may differ based on the following factors:

Before we move into the nondependent filing requirements, we need to discuss the standard deduction. Remember, the standard deduction reduces the amount of income that is subject to tax. This amount varies according to the taxpayer's filing status.

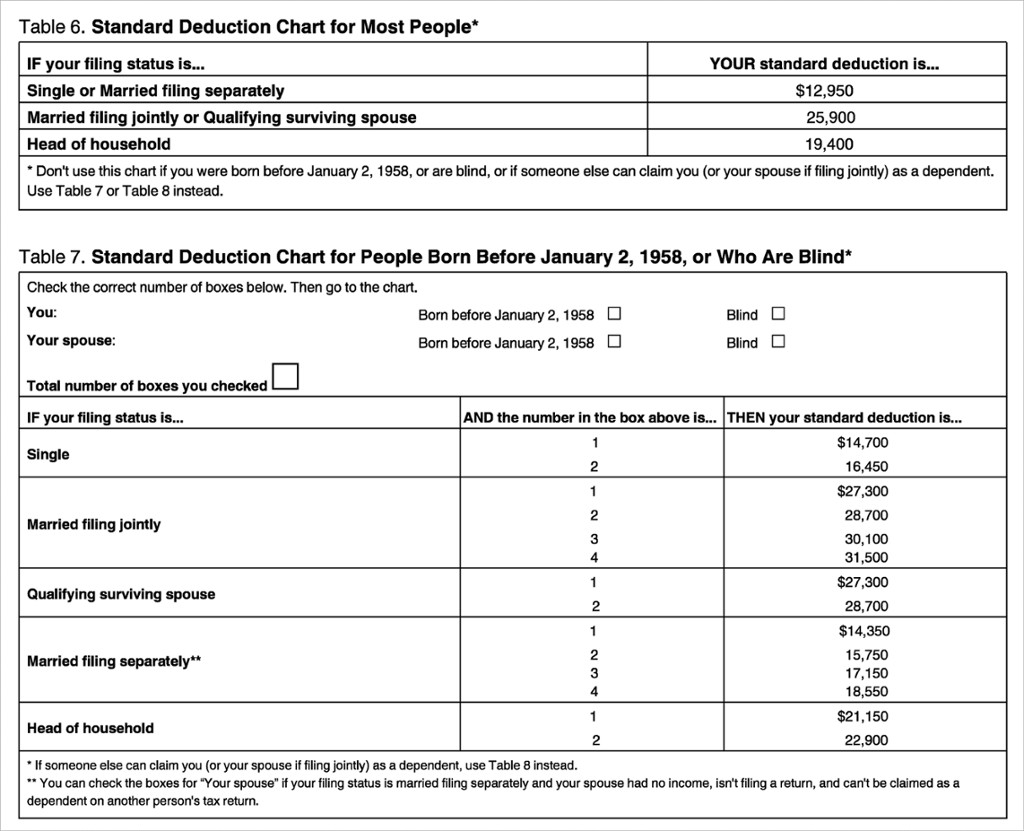

The following are the regular nondependent standard deductions for 2022:

Taxpayers age 65 or older and/or blind are entitled to increase their standard deduction by the following amounts:

EXAMPLE

Jaxon (66) and Mira (64) are filing married filing jointly. Neither is blind. Their standard deduction will be $27,300 ($25,900 standard deduction + $1,400 for Jaxon being over the age of 65).A taxpayer may claim the additional standard deduction for blindness if they are totally or partly blind at the close of the tax year. Partly blind means that the person is able to see no better than 20/200 in the better eye with corrective lenses, or the person has a field of vision not more than 20 degrees.

A taxpayer who is partly blind, and whose sight is not likely to ever improve beyond these limits, must obtain a certified statement stating this from their eye doctor (either an ophthalmologist or optometrist). The statement must be retained by the taxpayer with their records but does not need to be attached to the return or sent to the IRS.

If vision can be corrected beyond the limits by contact lenses that can only be worn briefly because of pain, infection, or ulcers, the higher standard deduction for blindness still applies.

Nondependent taxpayers are individuals who can't be claimed as dependents on another taxpayer's return. The majority of taxpayers are nondependents. The following three factors determine the filing requirement for nondependents:

For federal income tax purposes, there are five filing statuses:

The first step in identifying a taxpayer's filing status is to determine the taxpayer's marital status. Marital status (married or unmarried) is determined on the last day of the tax year. The marital status of a person who died during the year, as well as that of the surviving spouse if they do not remarry, is determined as of the date of death.

EXAMPLE

Bob and Carol were married on December 31, 2022. They are considered married for the 2022 tax year.EXAMPLE

Ted and Alice's divorce became final on December 31, 2022. They are considered unmarried for the 2022 tax year.EXAMPLE

Russell and Dawn have been married for several years. Russell died on March 27, 2022. Dawn did not remarry. Russell and Dawn are considered married for the 2022 tax year.EXAMPLE

Sally and Mary have been married for two years. Mary died on June 5, 2022. On October 15, 2022, Sally got married to Jane. Since Sally and Jane were married as of the last day of the tax year, they will file a joint return. Assuming Mary is required to file a final tax return, that return will be filed using the married filing separately filing status.If a taxpayer is unmarried on the last day of the tax year, they may be eligible to file as single, head of household, or qualifying surviving spouse. If a taxpayer is legally married on the last day of the tax year, the taxpayer may file as married filing jointly or married filing separately.

IN CONTEXT: Words Matter

There is a lot to learn when it comes to tax terminology, but getting the terms right matters. Married taxpayers only have two choices when it comes to filing status (with one exception you will learn about later)—married filing jointly or married filing separately. Often people refer to the separate status as married filing single. This is wrong and can cause confusion. Married taxpayers do not have the option to file single in any situation. Taking the time to get the terminology correct will help your understanding as well as help you serve clients more effectively.

A taxpayer is legally married if, at the end of the tax year, they are in a common-law marriage that is recognized in the state where the couple is residing, or was recognized by the state where the common-law marriage began.

While specific requirements vary by state, a common-law marriage generally must meet four legal standards:

While some states allow common-law marriages, there is no such thing as a common-law divorce. If the partners decide to go their separate ways, they must petition the state court for a decree of divorce just like any other married couple.

Following a landmark Supreme Court ruling in 2015 legalizing same-sex marriages in every state, married individuals who are members of the same sex must follow the same guidelines as other married couples.

For federal tax purposes, the term “spouse” includes an individual married to a person of the same sex if the couple is lawfully married under state (or foreign) law. However, individuals who have entered into a registered domestic partnership, civil union, or other similar relationship that is not considered a marriage under state (or foreign) law are not considered married for federal tax purposes.

Registered domestic partners are two individuals who are not married under state law. They are not recognized as married for federal tax purposes and cannot file married filing jointly, married filing separately, or as qualifying surviving spouse.

RDPs are recognized on a state-by-state basis, with some states recognizing them throughout the state, some states only recognizing them in certain counties, and other states not recognizing them at all. The State of California defines domestic partners as "two adults who have chosen to share one another’s lives in an intimate and committed relationship of mutual caring."

For general tax purposes, a person’s age is considered as of December 31st of the tax year. However, for filing requirements, a taxpayer is considered to have attained the age of 65 on the day before their 65th birthday.

EXAMPLE

Jane McGuire’s 65th birthday is January 1, 2023; for tax purposes, she is considered age 65 for the 2022 tax year.The age of a person who dies during the year is determined as of the date of death.

EXAMPLE

Shelton Burrows died on September 21, 2022, a month before his 65th birthday. He is age 64 for purposes of his 2022 tax return.As discussed in the last chapter, gross income is total worldwide income subject to tax. There are two aspects to determining gross income:

| Gross Income Filing Requirements for 2022 (Nondependents) | |

|---|---|

| Individuals Who Are: | Are Required to File If Their Gross Income Is At Least: |

| Single | |

|

$12,950 |

|

$14,700 |

| Married Filing Jointly | |

|

$25,900 |

|

$27,300 |

|

$28,700 |

| Married Filing Separately | |

|

$5 |

| Head of Household | |

|

$19,400 |

|

$21,150 |

| Qualifying Surviving Spouse | |

|

$25,900 |

|

$27,300 |

For 2022, the gross income threshold amount is the taxpayer’s standard deduction with an increase for taxpayers (and spouses if filing jointly) who are age 65 or older. This amount reduces the taxpayer’s income subject to income tax on their return. If a taxpayer has gross income less than their standard deduction, then it is generally safe to say that their gross income is reduced to zero and the taxpayer may not be required to file a tax return.

Ownership of income, in the case of a married couple, is determined by state law. The laws in most states regarding the ownership of income and property are based on British common law. These states are called separate property states. In separate property states, the income received belongs to the spouse who earned it or who owns the property that produced the income.

Nine states are community property states. See the chart below for a list of these nine community property states. With the exception of Wisconsin, the laws of community property states are based on Spanish civil law. Generally, in community property states, this community income received for services performed is considered to belong half to one spouse and half to the other spouse, regardless of which spouse earned it. The laws regarding the ownership of income from property vary among these states. Generally, ownership of income only needs to be determined if the couple files separate returns.

EXAMPLE

Community vs. Separate Property State

Community Property States:

Several states allow for domestic partnerships, or something similar, such as a Reciprocal Partnership or Civil Union. These laws generally provide registered domestic partners the same legal benefits and burdens as married couples. In community property states, registered domestic partner (RDP) status subjects the partners to community property rules. Although federal law does not treat an RDP as a married couple for tax purposes, the IRS has ruled that for tax years after 2006, community property rules should apply to RDPs, and that for years beginning after 2009, RDPs must report their income on their federal returns under these rules. An RDP must report half of all community income and all of their separate income unless certain exceptions apply.