Estimated tax payments are the general method used to pay tax on income not subject to withholding. Estimated tax payments are used to pay both income tax and self-employment tax. In most cases, self-employment income is not subject to withholding, so estimated tax payments are required.

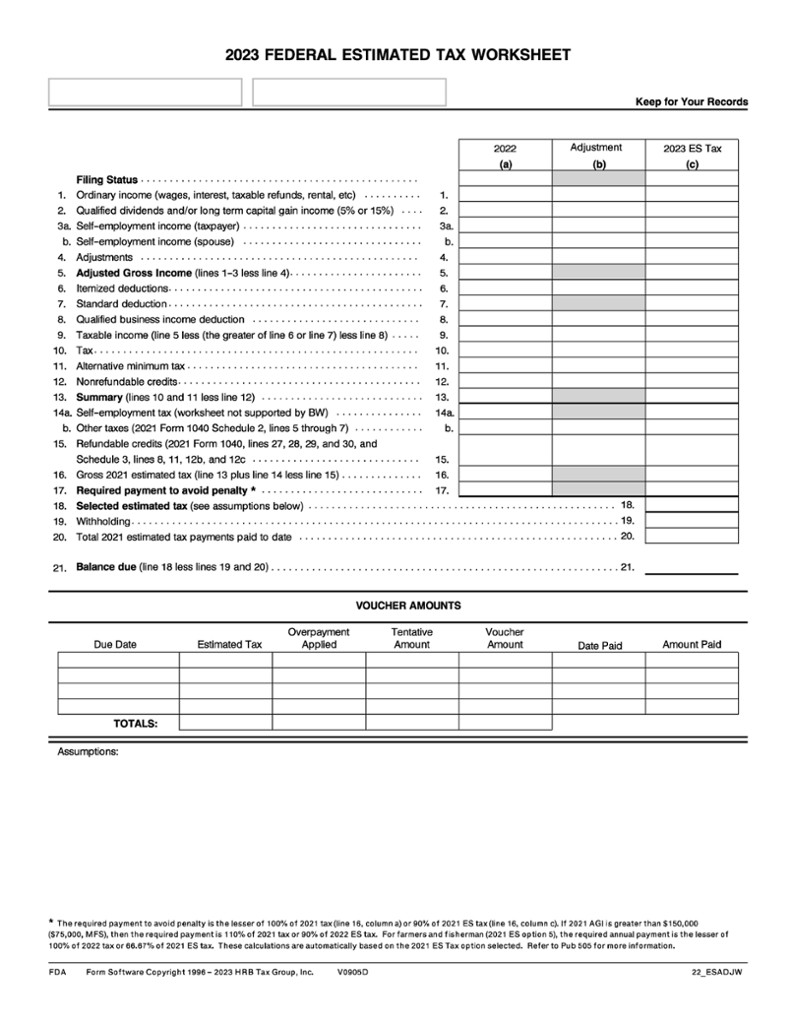

Form 1040-ES, Estimated Tax for Individuals, can be used to compute the total payments. The IRS worksheet only has one column for the 2023 estimated amounts. The 2023 Federal Estimated Tax Worksheet, shown below, can be used to determine whether a taxpayer is required to file quarterly estimated tax by comparing the 2022 actual figures with the estimated 2023 figures.

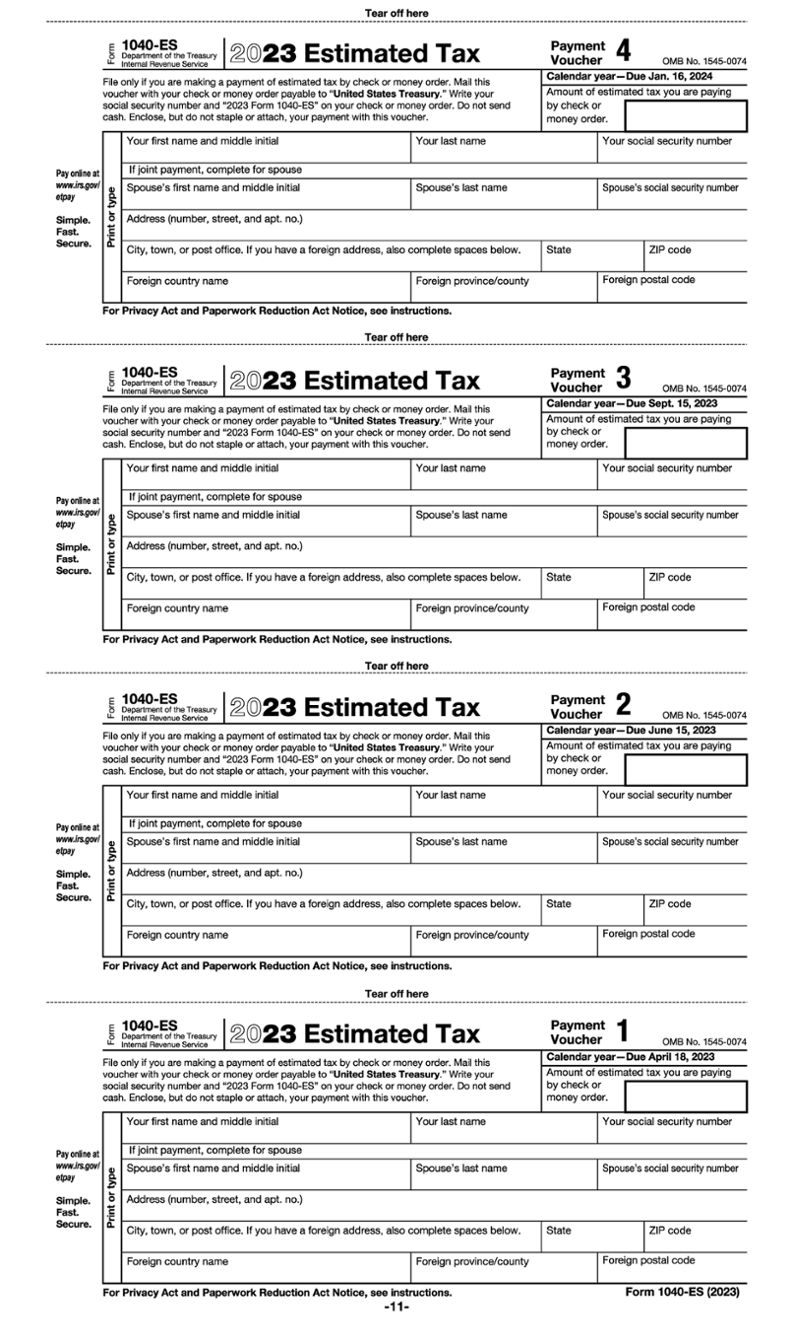

Form 1040-ES also contains blank vouchers that can be used when a taxpayer mails their estimated tax payments. Payments can also be made electronically using the Electronic Federal Tax Payment System (EFTPS).

Self-employed taxpayers will need to estimate the amount of income they will earn for the year. The United States tax system is a pay-as-you-go system, meaning tax payments must be made as income is earned. There are four estimated payment due dates:

If payments are estimated early in the tax year, they may be subject to change. If in a later quarter, the quarterly estimated earnings were too high or too low, simply complete another Form 1040-ES worksheet to recalculate the estimated tax for the next quarter.

It is important for sole proprietors to remit estimated tax payments to satisfy the income tax liability and self-employment tax requirements. Making timely estimated tax payments also helps to avoid underpayment penalties. As a tax preparer, it is your job to assist your clients in calculating their estimated tax payments.

Estimated Tax Worksheet

Estimated Tax Vouchers

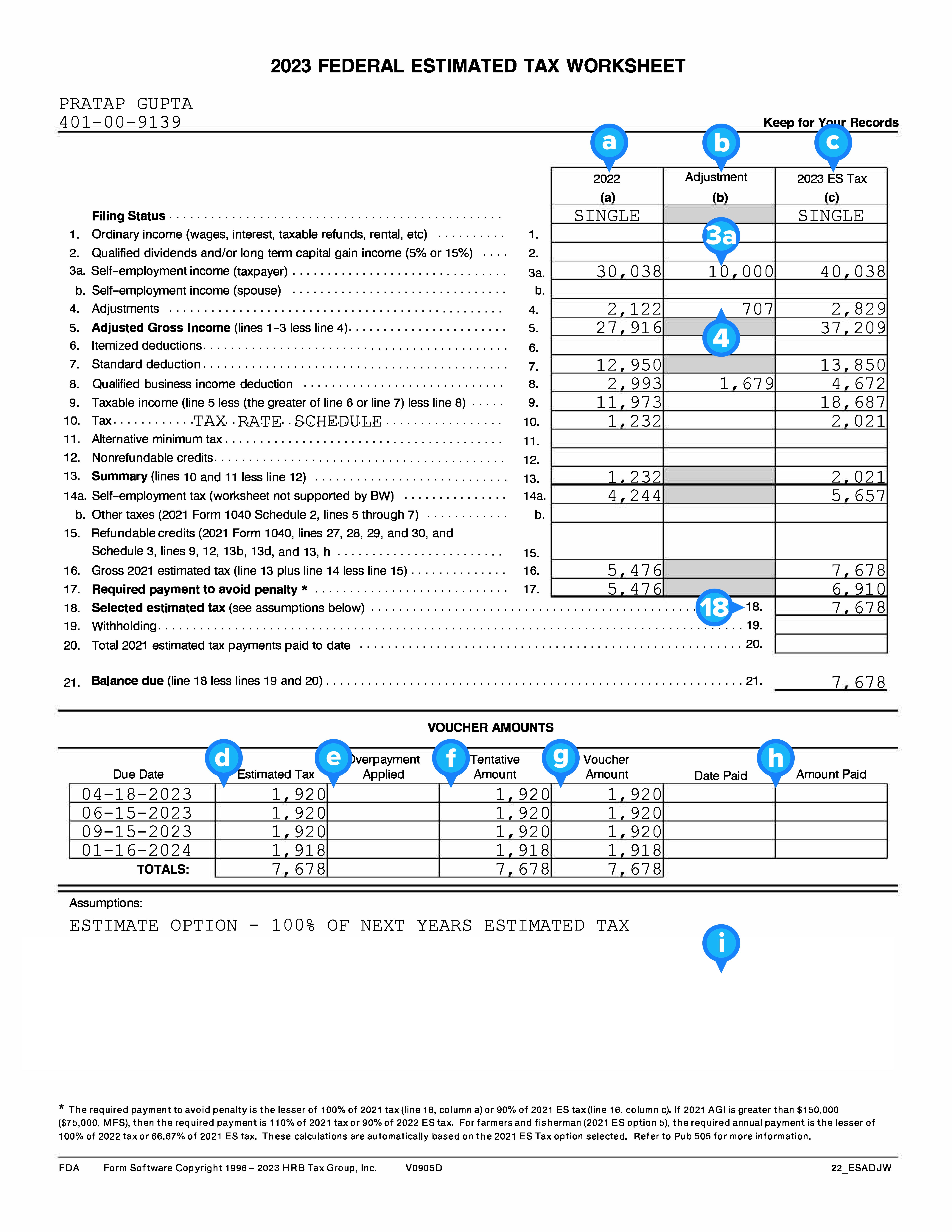

EXAMPLE

Pratap Gupta from Exercise 12.6 would like help with his 2023 estimated tax payments. He feels everything will basically be the same in 2023 as it was in 2022, other than an increase in business profits of $10,000.

Most members of the clergy are employees and should receive Forms W-2 from their religious organizations. However, churches, synagogues, mosques, or temples generally will not withhold income or payroll taxes, so the clergy members must pay self-employment tax on their compensation.

Instead of receiving Social Security and Medicare coverage through employee withholding, a clergy member pays self-employment tax on their wages, fees received, and housing allowance or the value of furnished lodging. This is true unless an election is made with the Internal Revenue Service to not be covered by such public insurance.

Members of religious orders who have taken a vow of poverty are not subject to self-employment tax if the income received for services performed as an agent of the order is turned over to the order.

The value of lodging furnished or a housing allowance, to the extent it is used to pay rent or house payments, furniture payments, utilities, and other expenses of maintaining the home, is not subject to income tax if the clergy member performs religious duties and functions. It is subject to self-employment tax, however.

EXAMPLE

Brother Bill received a housing allowance of $10,000 during the year. The $10,000 is included in his gross income for self-employment tax but excluded from income tax.If subject to Social Security coverage, clergy members enter their wages and the value of furnished lodging or housing allowance on line 2 of Schedule SE (Part I). Other religious workers subject to self-employment tax enter their wages on line 5a of Schedule SE (Part I). In both cases, taxpayers should make estimated tax payments for their expected income tax and self-employment tax liability.

A statutory employee is an employee for Social Security and Medicare tax purposes and self-employed for income tax purposes. This is the opposite of a clergy member who is a church employee but considered self-employed for purposes of Social Security and Medicare.

If an employee is a statutory employee, the small box indicating so in box 13 of their Form W-2 will be marked. Such an employee will have Social Security and Medicare taxes withheld, but there will be no federal or state tax withheld.

Typical statutory employees include:

Statutory employees should report their wages on Schedule C. A statutory employee has the advantage of using the full extent of their employee expenses on Schedule C to reduce their taxable income.

Report net profit or loss from Schedule C on Schedule 1. However, do not complete Schedule SE for any statutory employee income. Their Social Security and Medicare are already withheld from their pay.

Earned income for statutory employees for IRA and various credit purposes is the amount on Schedule C, line 1, rather than net profits.