Let's begin with a quick review of the laws of supply and demand:

In this tutorial, we will be discussing exactly how much more or less, and if it is the same for every good.

Elasticity is the measurement of the change in quantity demanded or supplied which indicates the sensitivity of one variable to characteristics of another variable or income.

In this tutorial, it is easier to discuss this concept with quantity demanded.

In today's lesson, though, we are focused on elasticity in the context of quantity demanded.

In other words, how much do people respond--by buying more or less--when something else changes, like price or income?

The answer is that it really depends on the good or service:

Now, elasticity is a proportion. The equation for elasticity is the percentage change in quantity-- how much people respond--divided by the percentage change in price.

Notice that for demand, elasticity will always be negative because the relationship between quantity and price is negative, as they move in opposite directions. If the price goes up, then people buy less.

For supply, it will always be positive because quantity and price move in the same direction. As prices go up, producers want to supply a greater quantity, and vice versa.

| Elasticity Equation | |

|---|---|

| For Demand | For Supply |

| NEGATIVE, since Q & P move in opposite directions | POSITIVE, since Q & P move in the same direction |

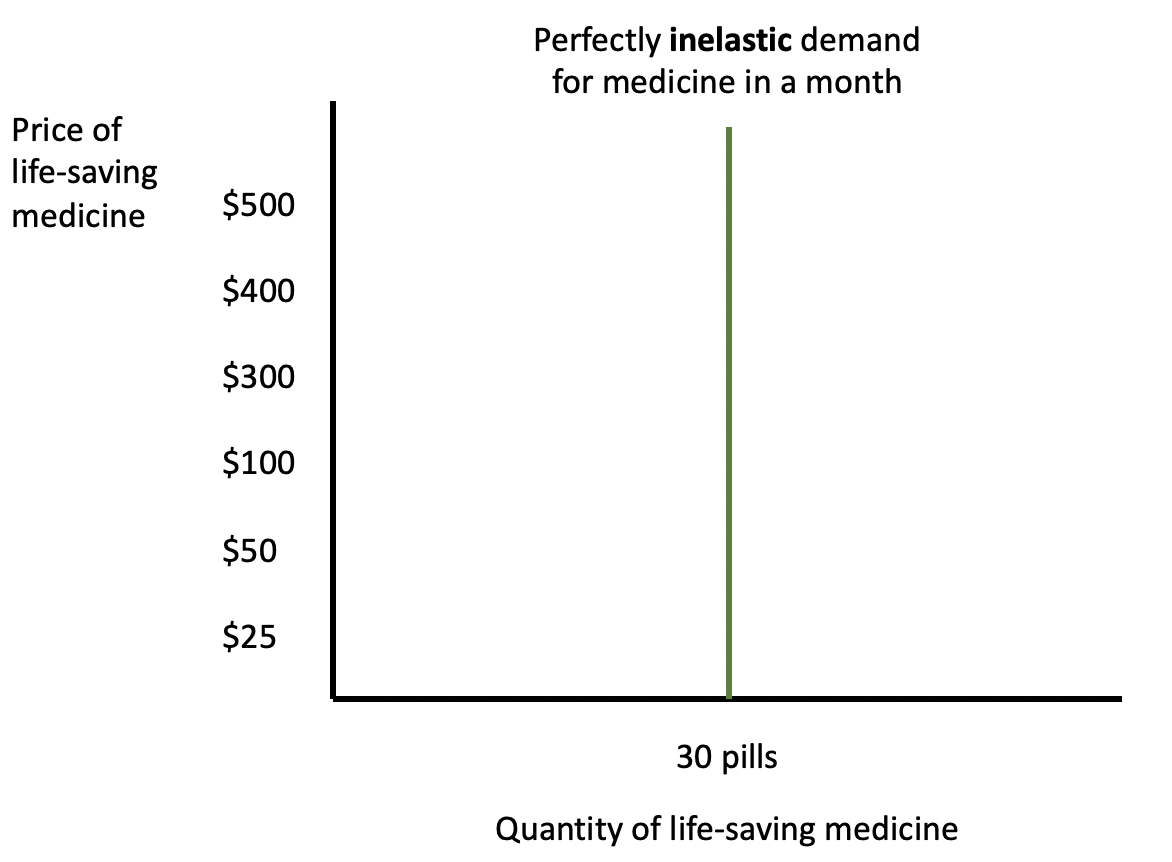

Let's look at an extreme example of monthly demand for life-saving medicine.

Notice we have the price of this life-saving medicine on the y-axis and the quantity that people are purchasing on the x-axis.

Now, no matter how expensive this medication gets, people are purchasing the exact same quantity--30 pills per month. Therefore, they are not responsive at all to a price change because a life-saving medicine is a necessity, and there are no substitutes.

Perfectly inelastic demand, then, is defined as demand for goods and services that remains the same regardless of a change in price, resulting in a vertical line on the demand curve.

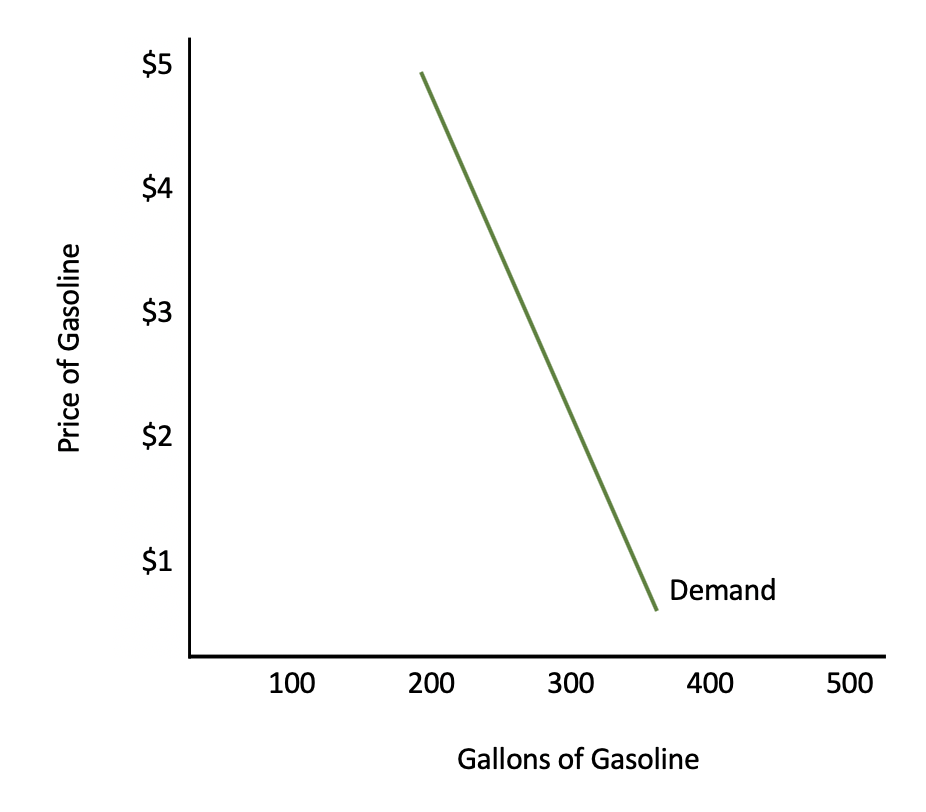

Now, most things in the world are not perfectly inelastic, but there are items like gasoline that are relatively inelastic.

This is not straight up and down, or completely vertical, because people do change their behavior somewhat as the price of gasoline goes up.

However, notice how the price can change significantly, yet consumers do not change their purchasing habits very much. This is because most people view gasoline--at least in the short term--as a necessity and without a substitute.

Now, as prices goes up significantly, people do tend to stop going on long trips or they carpool, so there are things that can be done, but it is still relatively inelastic.

Inelastic demand is demand that does not respond easily to the changes of other economic variables.

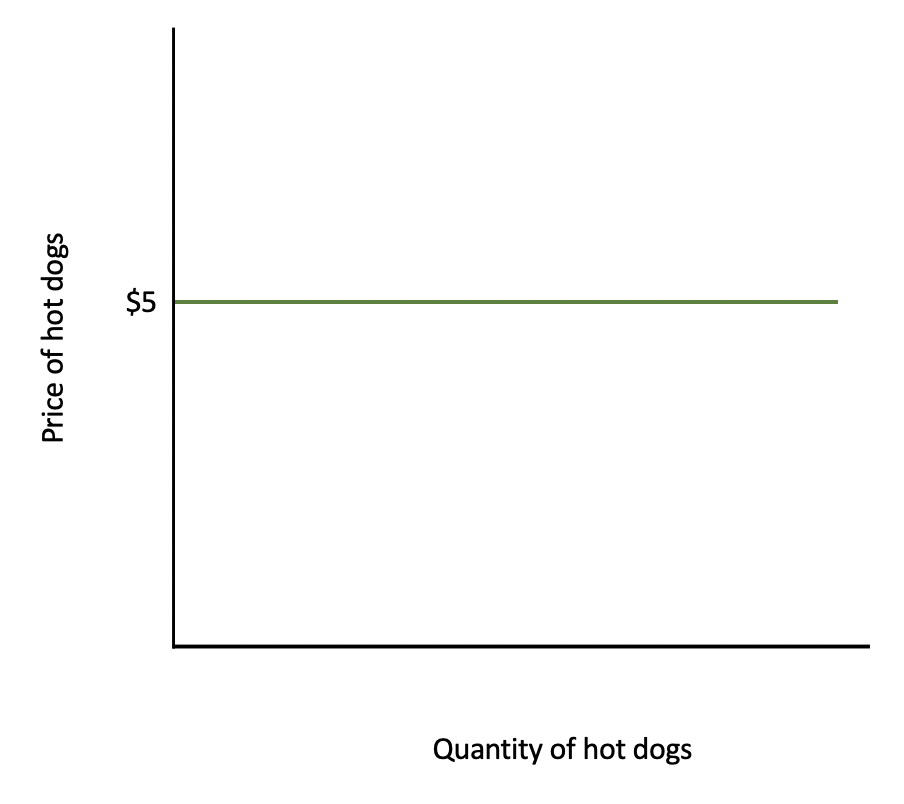

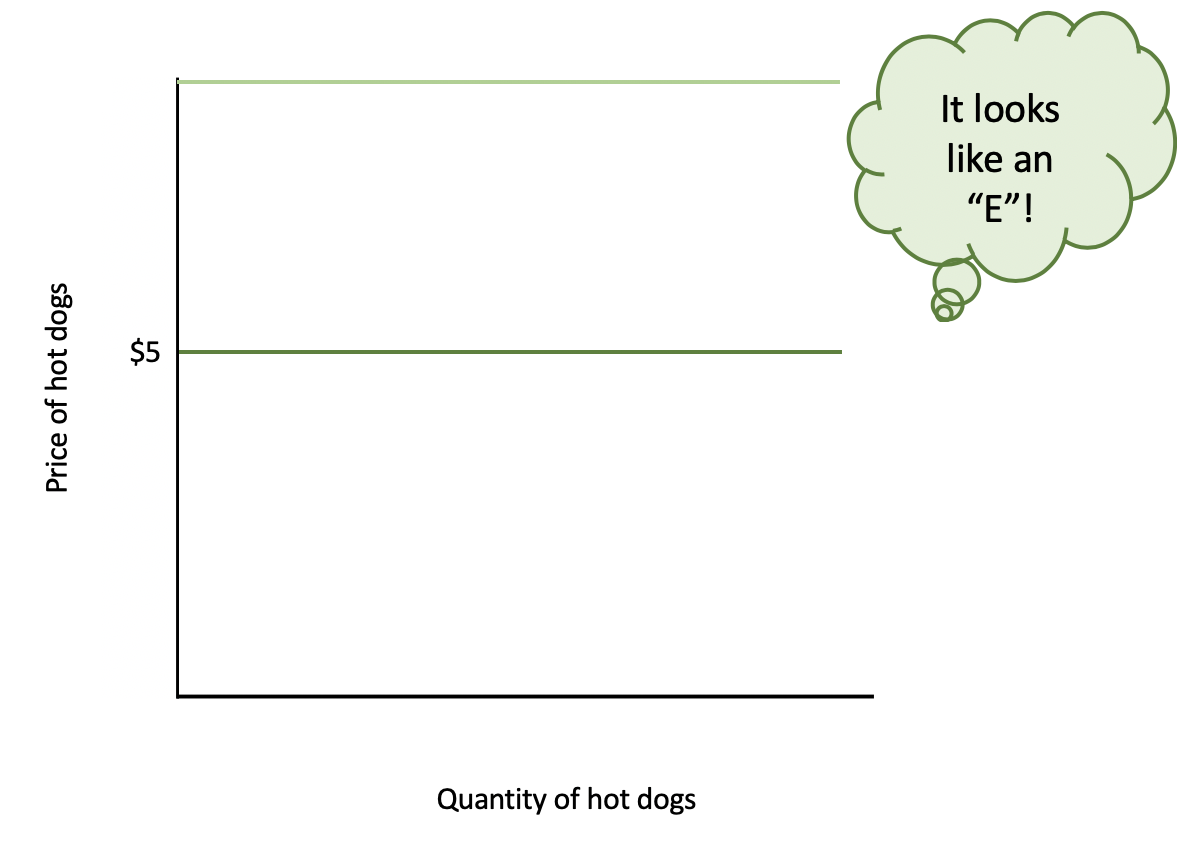

Let's look at the opposite extreme, which is perfectly elastic demand.

Again, this is difficult to find in the real world, but we will use the hypothetical example of a hot dog stand that is one of 200 stands in a baseball stadium. They are all selling an identical product and are all charging $5 for that identical hot dog.

If one hot dog stand out of 200 decided to raise price, even marginally, no one would purchase a hot dog there. The quantity demanded, in theory, according to this curve, would drop to zero.

There is no ability to change price here; there is only one price they can charge. They can sell all that they want at this price, so there is no incentive to drop the price. Conversely, if they raise the price at all, nobody would purchase from them.

Perfectly elastic demand refers to demand for goods and services that changes significantly due to change in price, resulting in a horizontal line on the demand curve.

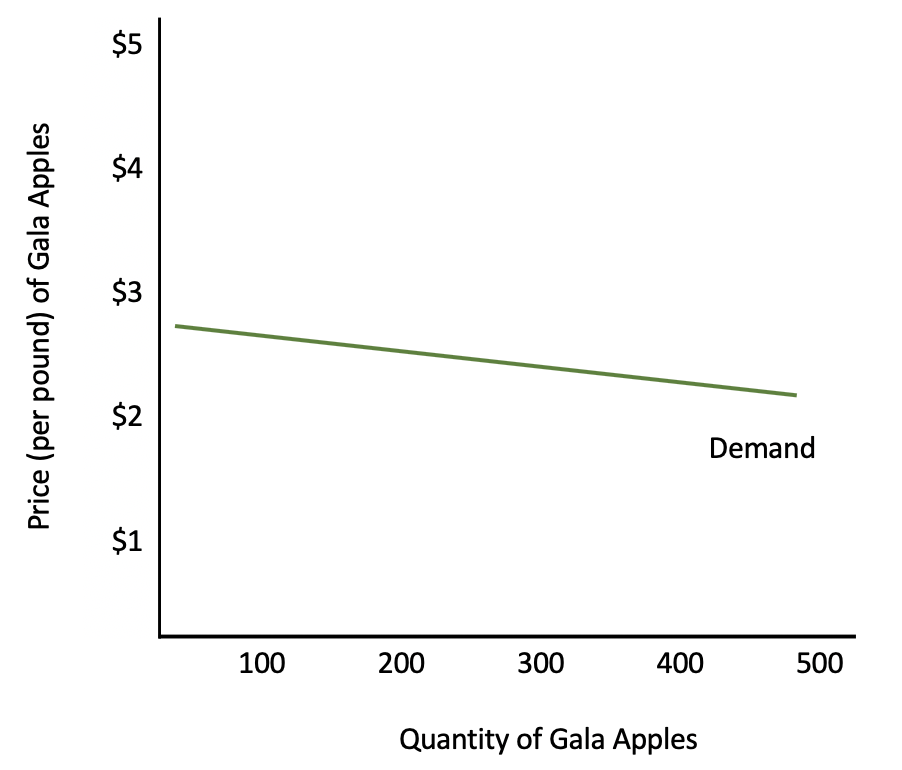

However, not many things are perfectly elastic in the world, so here is an example of something that is simply elastic, which would be the demand for a specific brand of something.

Demand for a specific type of apples, like Gala apples, would be somewhat elastic, because there are many substitutes for a single brand of apples.

If Gala apples are the only ones changing in price, notice how even a small change in the y-axis, in price, results in a large change in quantity being purchased of Gala apples.

It is not completely horizontal, because prices could increase a bit and you would still see purchases of Gala apples by people who simply prefer them.

Elastic demand is defined as demand that responds easily to the changes of other economic variables.

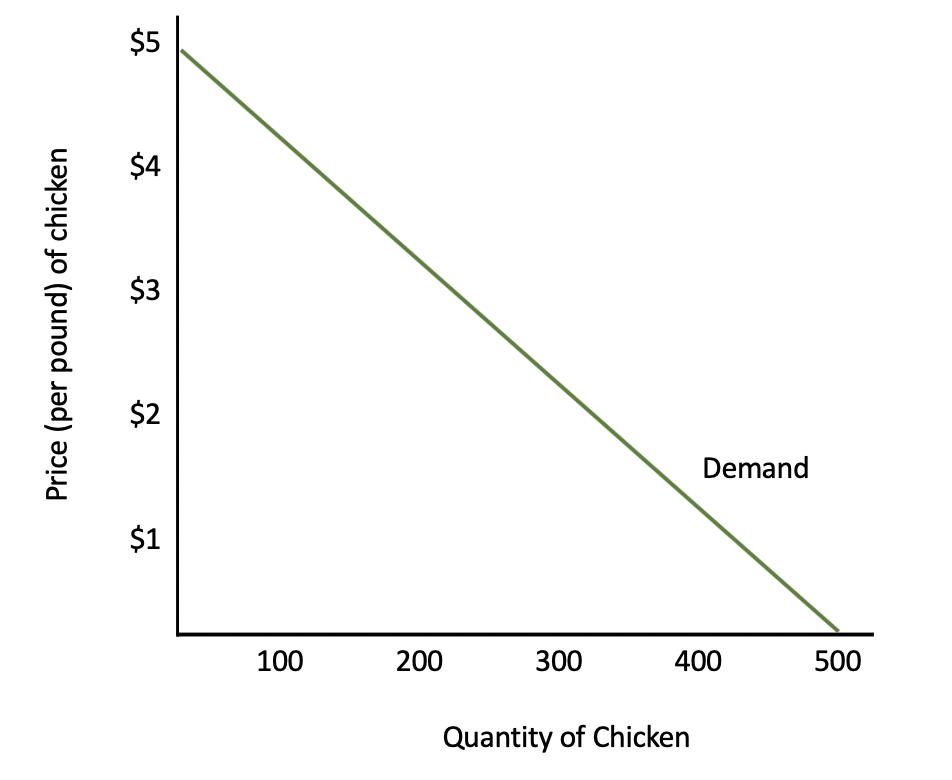

Finally, we have unit elastic demand, illustrated by this example using demand for chicken.

Along this curve, let's assume that the price of chicken rises by 10%, and as a result, consumers buy exactly 10% less chicken. Perhaps they buy beef instead of chicken that week.

Unit elastic means that the change in price proportionately changes the level of demand.

Source: This work is adapted from Sophia author Kate Eskra.