Table of Contents |

Debt financing is an arrangement in financing in which a company takes a loan and agrees to pay back the loan at a specified point in time. Now, businesses will use financial leverage to borrow funds that they need to try to increase the return on their owner’s equity in their long-term plans or goals.

This is true as far as return on that owner’s equity and as long as the businesses’ earnings are going to be greater than the interest that is charged for that particular loan. So, this is beneficial as long as the earnings are going to be solid for a company. If something unexpected happens, however, then the plan can backfire, because the business has to make up that interest payment along the way. For small businesses, long-term financing typically involves only loans.

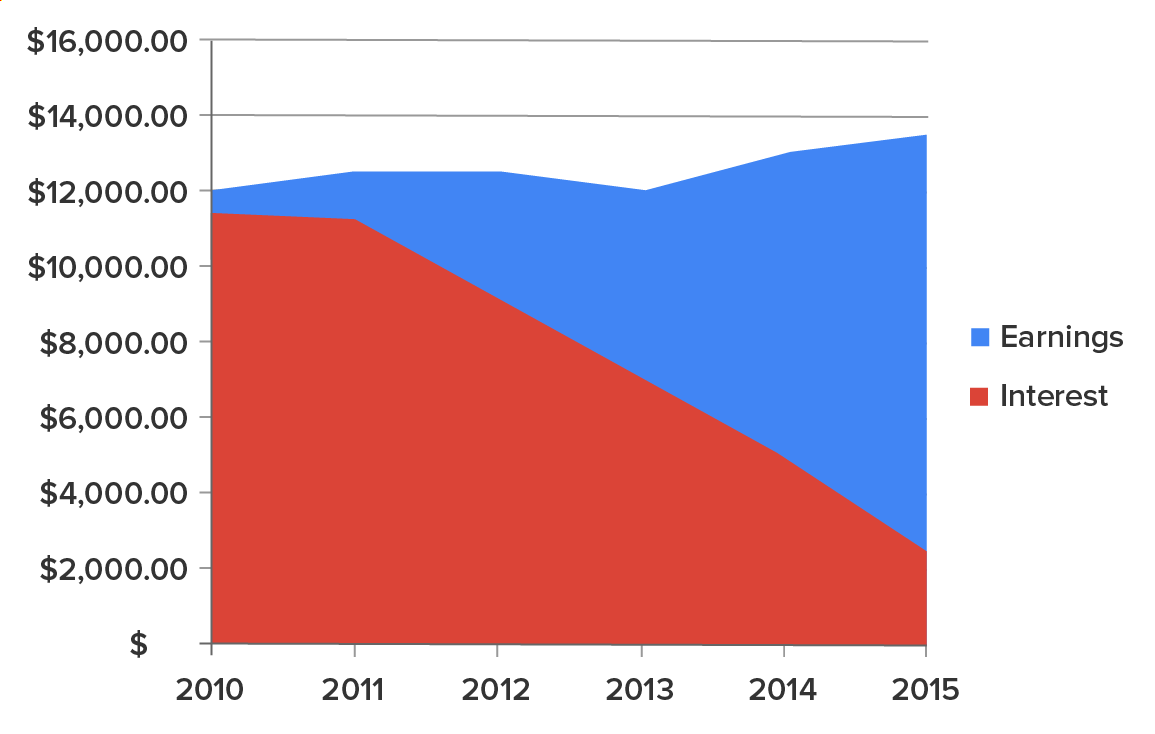

Look at the graph below. Note that the blue area represents earnings for a company and the red area is the interest that’s going to be charged for a particular type of long-term financing.

Notice that the company is making from $12,000 up to about $13,500 per year from 2010 to 2015. In this case, the interest along the way decreases along the maturity of the loan. Therefore, as long as there is that gap between earnings and interest, the situation is favorable for this particular financing. However, the company has to watch out for unexpected occurrences or outlays, especially at the beginning, that result in the company not being able to make up the difference between the earnings and the interest. In that case, it would be in trouble.

Long-term loans are typically offered by banks. Manufacturers and suppliers may also provide long-term credit, which functions as a type of long-term loan as well. When businesses get loans for more than a year, they need to have a term loan agreement, which is a promissory note that details a repayment process for that particular loan.

These are typically very long and complicated.

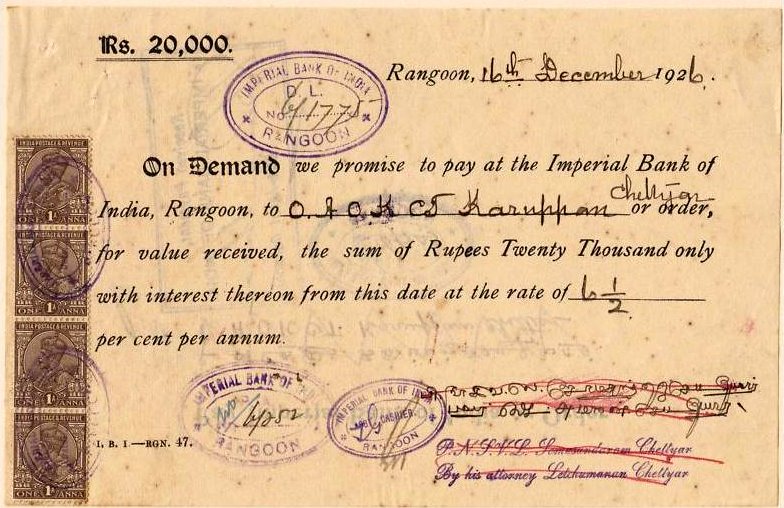

EXAMPLE

Consider this older type of promissory note to pay back a loan from the Imperial Bank of India in Rangoon.

Corporate bonds are a slightly different type of long-term financing. A bond is a financial instrument in which the organization, a company, or the government offers an IOU to the holder of the bond. The organization promises to repay the original price of the bond (called the principal) along with a set amount of interest by a specific date. The specific period when the payout is due is called the maturity date.

The maturity date is the final payment due date for a loan or other monetary instrument such as a bond. Now, with bonds, all the legal information you need to know about the bond is going to be in something called the bond indenture. Typically, a corporation appoints someone called a trustee, who is an independent person or a firm that serves as the representative for the bond owner. In most cases, this is going to be a bank—one that is independent from the bondholder or the bond issuer and will be responsible for communication between the corporation and the bond owners.

There are different types of corporate bonds. One type of corporate bond is called a debenture bond. A debenture bond is unsecured, and, typically, it’s only issued by financially strong companies because the only thing that secures it is the company’s word that it will pay this bond back. Think about it—if the company wasn’t strong and trustworthy, nobody would issue this bond because there would be no guarantee that the company would actually pay it back.

Another type of corporate bond is a mortgage bond. A mortgage bond is made up of pooled property that’s used as collateral against the face value of the bond. So, if for some reason the corporation defaults or doesn’t pay back the bond in accordance with the bond indenture, then the pooled property is sold and those funds are used to pay back the bond.

Now, let’s take a look at bonds versus loans and compare the two.

Long-Term Loans

EXAMPLE

If you issue a bond for $1,000, for example, because of the high sell and administration cost, you will only recoup about $900 or so against that $1,000 promise to pay back. As the one issuing the bond, you won’t recoup the full face value. However, if you buy this bond, you can be assured that you’ll get that full face value back—plus the 5% to 10% interest rate every year for the life of the bond.Source: adapted from sophia instructor james howard