In this lesson, you will learn what a FICO score is, why it matters, and how it is calculated. You’ll also learn how to establish credit and monitor your credit report, including how to spot cases of identity theft. Specifically, this lesson will cover the following:

1. What a FICO Score Is

-

What is a FICO score?

Think of your

FICO score, also known as your credit score, as your financial report card—but instead of grading your math skills, it grades your monetary skills!

As you previously learned your credit score ranges from 300 to 850 and it tells lenders how likely you are to pay them back. Think of it like a backstage pass to the world of loans and credit: The higher your score, the more VIP treatment you get, like lower interest rates and faster approvals. Your FICO score is based on things like how often you pay your bills on time, how much you owe, and the kinds of credit you’re juggling. So, if you want the red carpet rolled out for your financial dreams, boosting that score is key.

Whether you’re financing a car, getting a mortgage, or applying for a credit card, lenders look at your FICO score to decide if you’re a risky borrower and, subsequently, what interest rate to charge. Understanding how FICO scores are calculated and how they influence borrowing costs can help you make informed financial decisions.

-

FICO stands for Fair Isaac Corporation—the company that created the FICO score way back in 1956.

You might wonder, “If I don’t have any credit cards, do I actually have a FICO score?” This is an excellent question! The answer is maybe. Let’s dig deeper.

You can still have a FICO score even if you don’t have any credit cards! FICO scores are based on different types of credit, not just credit cards. Other accounts, like car loans, student loans, mortgages, or even certain types of bills (like a credit-builder loan), can help you build a credit history. We’ll talk about all of these in more depth later on.

If you have at least one credit account that’s been open and active for at least six months and has been reported to the credit bureaus, you can generate a FICO score. It might take a little longer to build a score without a credit card, but other types of credit accounts work, too.

Next, we will break down the building blocks of your FICO score, starting with where the information comes from and how it’s collected.

-

- FICO Score

- A three-digit number (300–850) that shows how likely you are to repay debt. Also known as a credit score.

1a. Credit Bureau Reports

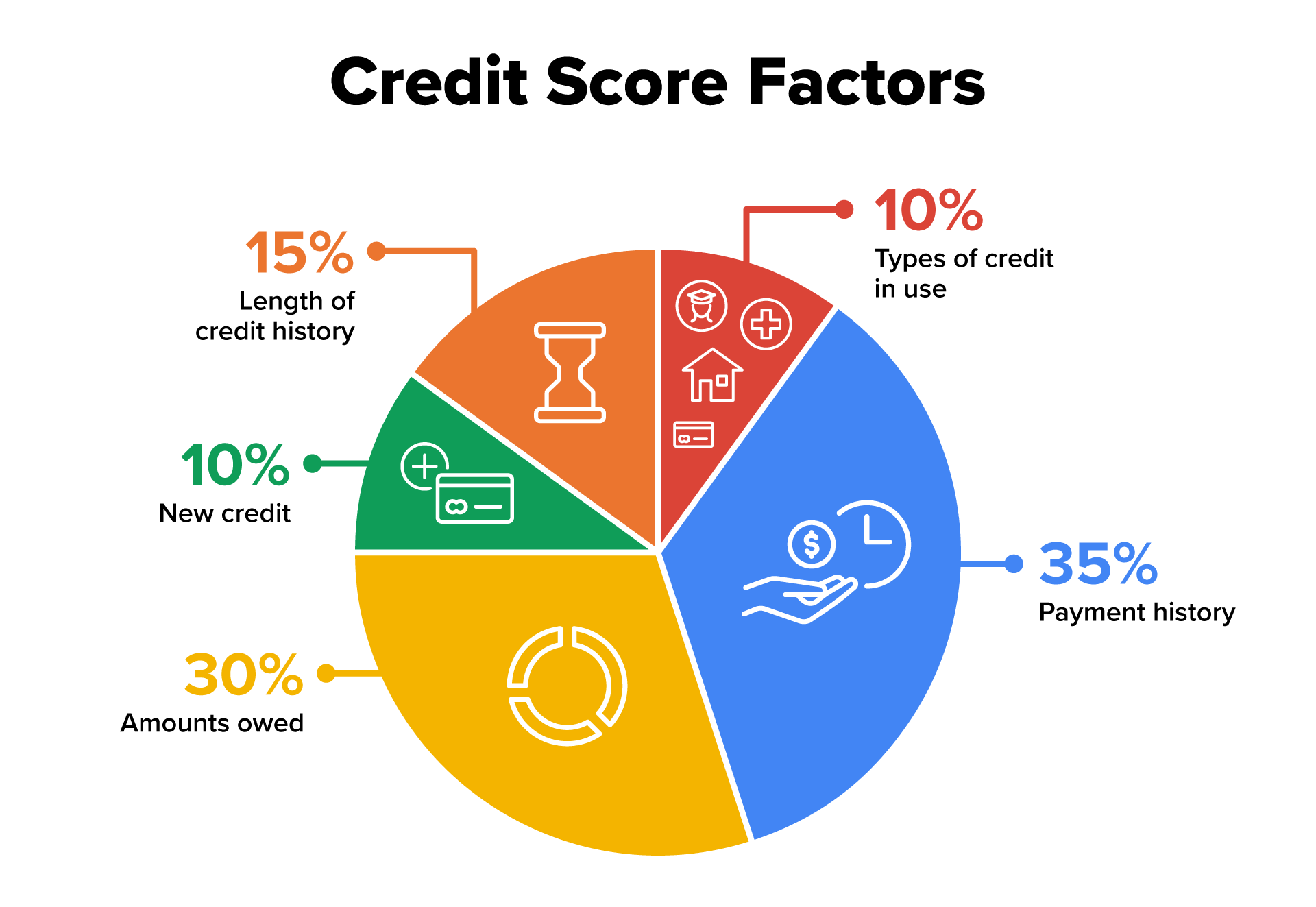

Your FICO score is based on information collected by credit bureaus—agencies that gather and manage credit information. The three major credit bureaus in the United States are Experian, Equifax, and TransUnion. These agencies compile credit reports. A credit report is a detailed record of your credit history. It shows lenders and other entities how you manage credit. Here are the components of your FICO score:

- Payment history

- Amounts owed

- Length of credit history

- Types of credit in use

- New credit inquiries

Each factor influences your FICO score, which ranges from 300 (poor) to 850 (excellent). For example, missed payments or a high balance on a credit card can lower your FICO score, while timely payments and a mix of credit types can improve it. Since each bureau may have slightly different information, your score can vary among them. This is very common, so don’t be alarmed if this happens to you.

Lenders use credit reports to determine how reliable you are when it comes to repaying loans. Knowing how each item on your credit report affects your score can empower you to make choices that positively impact your borrowing options.

-

Do you know your FICO score? Now is a great time to figure out your FICO score, and this couldn’t be easier.

You can get a free credit report from each of the three major credit bureaus—Experian, Equifax, and TransUnion—once a year by visiting

AnnualCreditReport.com. This is the only official site authorized by federal law to provide free credit reports.

Here’s how it works:

- Go to www.annualcreditreport.com and follow the instructions to request your reports.

- You’ll need to enter some personal information (like your Social Security number) to verify your identity.

- Choose whether you want to view your reports from one, two, or all three bureaus.

You can check all three reports at once, or you might choose to space them throughout the year to monitor your credit more frequently.

You can also find out your credit score by looking at your most recent credit card statement. Most credit card companies now display a credit score right on your statement. If you don’t have a credit card, you can use a free mobile app like

Credit Karma or

Credit Sesame to see your most recent FICO score.

Now that you have an understanding of credit bureau reports, next we will dive into what the FICO score itself represents and how it’s calculated.

-

- Credit Bureaus

- Companies that collect and store credit information, like payment history, to help lenders make decisions regarding loan approvals. The major U.S. credit bureaus are Experian, Equifax, and TransUnion.

- Credit Report

- A detailed record of your credit history, including your loans, credit card accounts, payment history, and any outstanding debts, that lenders use to assess your creditworthiness.

2. How Your Fico Score Is Calculated

Your FICO score is calculated based on the information in your credit report. The score itself is calculated based on five items:

1. Payment history (35%): Have you paid past credit accounts on time? The best way to make sure you are paying your bills on time is to set up automatic payments. However, you need to make sure that you have enough money in your bank account to pay your bills.

2. Amounts owed (30%): How much debt do you currently owe? This is also known as your credit utilization number.

-

EXAMPLE

Imagine you have a credit card with a $1,000 limit, and you’ve charged $300 to it. This means you’re using 30% of your available credit. Keeping this usage below 30% is generally recommended to maintain a good credit score. So, if you stay under $300 on that $1,000 limit, you’re in the ideal range for healthy credit utilization!

3. Length of credit history (15%): How long have your accounts been open? This time clock starts with the very first piece of credit that you open. Lenders see a longer history as a sign that you have more experience managing credit responsibly. This history includes how old your first account is, how new your most recent account is, and the average age of all your accounts.

-

If you have an old credit card, keep it open even if you’re not using it much. Closing it can make your credit history look shorter, which might lower your credit score. The longer your history, the better it can be for your score! If you’re worried that keeping your credit card will entice you to overspend, you can tuck it away outside your wallet or cut it up. If you need to use it again, simply pull it back out or contact the credit card company and ask for another card to be sent to you.

4. Credit mix (10%): What types of credit accounts do you have (e.g., credit cards or loans)? Credit bureaus like to see a good mix of credit, such as a car loan, a student loan, a credit card, and a mortgage.

5. New credit (10%): Have you recently applied for any new credit?

-

Here are some tips for managing new credit to keep your score healthy:

- Apply Only When Necessary: Each time you apply for credit, it triggers a hard inquiry into your credit report, which can temporarily lower your score. Avoid applying for multiple accounts at once as this can signal to lenders that you might be taking on too much credit too quickly.

- Space Out Applications: If you do need new credit, try to space out applications over a few months. This gives your score time to recover between inquiries and look more stable to lenders.

- Avoid Opening Too Many Accounts at Once: Opening several new accounts in a short time can make you look risky to lenders. This is especially important if you’re new to credit—gradually building credit with just one or two accounts can strengthen your score over time. Try not to open more than three new lines of credit in a 90-day period.

- Look for Preapprovals: Preapprovals or soft inquiries don’t impact your score (e.g., using a mobile app like Credit Karma or Credit Sesame to check your credit score). Many credit card companies offer preapprovals that allow you to see if you’re likely to qualify without affecting your score.

2a. Why Your FICO Score Matters

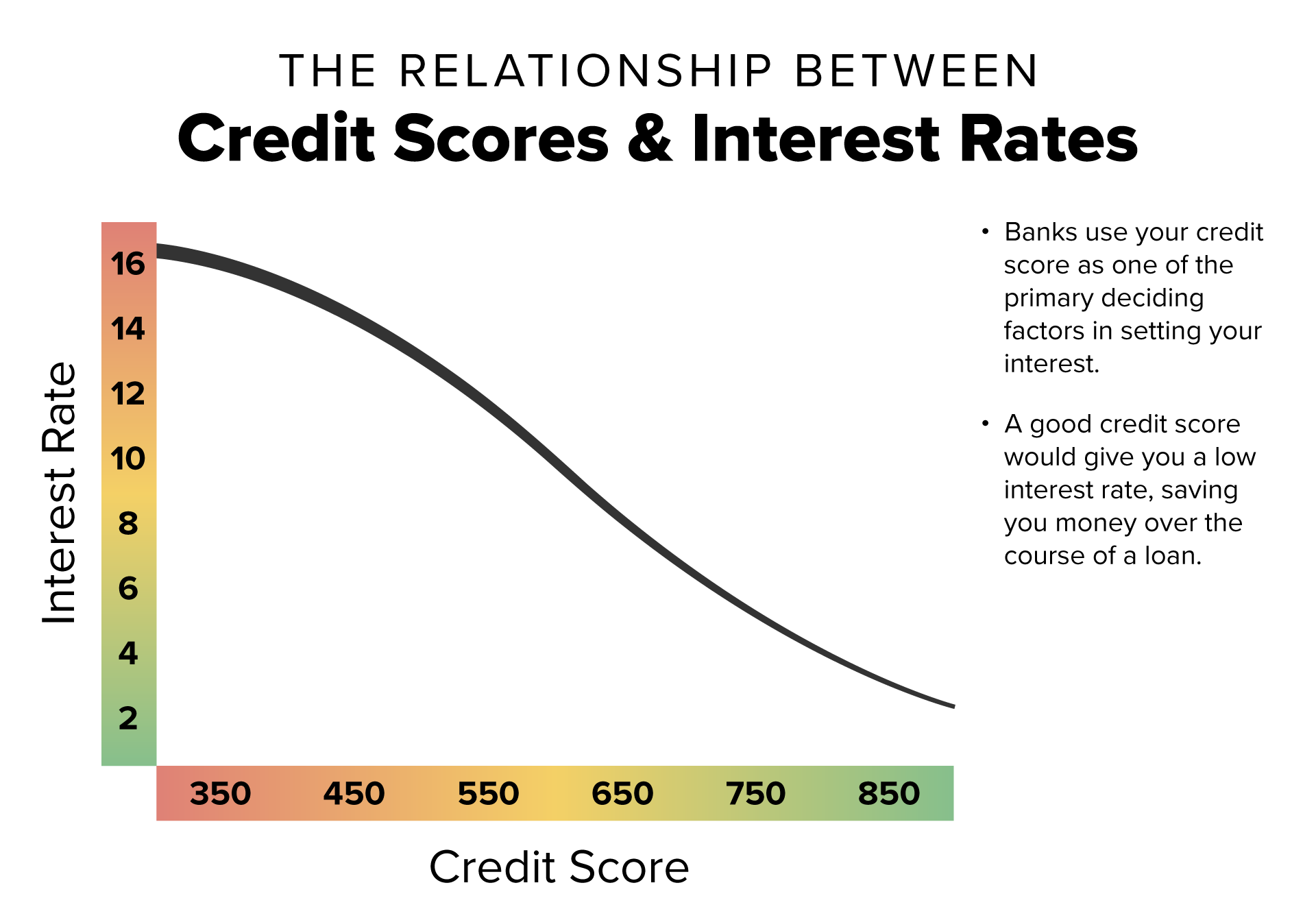

Your FICO score affects not only whether you’ll get approved for loans but also the terms of those loans. Borrowers with high scores often receive lower interest rates, saving thousands of dollars over the life of a loan. Those with lower scores may be subject to higher rates or even face denial on a credit application.

-

EXAMPLE

Imagine two friends, Alex and Jamie, both applying for a $20,000 car loan. Alex has a FICO score of 780, which is considered excellent, while Jamie’s score is 620, which falls into the fair range.

Because Alex has a high score, the lender sees them as low risk and offers a low interest rate of 3%. This means Alex will pay much less interest over the loan’s term. For Alex, the monthly payment on a 5-year loan would be about $360, and they would pay roughly $1,800 in interest by the end of the loan.

Jamie, with a lower score, is seen as a higher risk by the lender. As a result, the lender offers an interest rate of 10%. With this higher rate, Jamie’s monthly payment on the same 5-year loan would be around $425. Over those 5 years, Jamie would pay about $5,500 in interest—more than triple of what Alex would pay!

Big takeaway: Even though they’re both borrowing the same amount for the same car, Jamie will pay significantly more overall because of the higher interest rate. A higher FICO score means lower interest rates, which saves you a lot of money over time.

Here’s how your FICO score translates to borrowing costs and, ultimately, your interest rates.

- Excellent (720–850): You’ll generally receive the lowest rates, saving thousands over the life of a loan.

- Good (680–719): You’ll get favorable terms, though not as low as the top tier.

- Fair (620–679): You’ll likely receive higher interest rates, making loans more expensive.

- Poor (below 620): You may struggle to find lenders willing to work with you or face very high rates if approved.

With an understanding of what goes into your FICO score and why it is important, let’s discuss how you can establish credit if you’re starting from scratch.

3. How to Establish Credit

If you’re new to credit, establishing it might feel daunting, but don’t worry, you’ve got this. Here are three ways you can kick-start your credit-building journey:

- Try a Secured Credit Card: Think of this as a credit card with training wheels! A secured credit card is a type of credit card that requires a cash deposit up front as collateral. This deposit reduces the risk for the credit card issuer, making it easier to get approved, especially for people with limited or poor credit history. The deposit usually becomes your credit limit, so if you deposit $500, you can typically charge up to $500 on the card. Using a secured credit card responsibly (by making payments on time) can help you build or improve your credit score. Use it for small purchases—maybe your favorite coffee or gas—and then pay it off each month. It’s an easy way to show you’re responsible with credit, and you get bonus points for paying on time! Once you’ve used a secured credit card for 6 months to a year responsibly, you can typically upgrade to a traditional credit card.

- Hop on as an Authorized User: An authorized user is someone who has permission to use someone else’s credit card account, but they’re not responsible for paying the bill. The primary account holder adds the authorized user to their account, and the authorized user gets their own card to make purchases. Food for thought: Being an authorized user can help you build or improve your credit score if the account is in good standing since the account’s positive payment history can appear on your credit report. Ask a family member or friend with great credit to add you as an authorized user on their card. This way, you get the benefit of their good payment history without actually being responsible for the bill!

- Get a Credit-Builder Loan: Think of a credit-builder loan as a practice loan. Instead of getting money up front, you make small monthly payments that go into a savings account. Once you’re done paying it off, you get the money—and you’ve built credit along the way!

These options are like setting up stepping stones for your credit journey. They are low risk, are easy to manage, and help you build credit without diving into debt!

Once you’ve built your FICO score, it’s time to stay informed about what’s on your credit report. Let’s look at why monitoring is an important part of your financial plan.

-

- Secured Credit Card

- A card that requires a cash deposit as collateral, which usually sets your credit limit. It’s used to help build or rebuild credit.

- Authorized User

- Someone added to another person’s credit card account, allowing them to use the card but not be responsible for payments.

- Credit-Builder Loan

- A small loan designed to help people build or improve credit; the borrowed amount is held in a bank account and released only after full repayment.

4. Monitoring Your Credit Report

Regularly checking your credit report is essential for maintaining a healthy credit score. By using a free service like Credit Karma or Credit Sesame, you have the ability to monitor your credit score and report at the tip of your fingers. Looking at your own credit report will not lower your credit score. Remember, this is called a soft pull. However, when you apply for a new piece of credit or a loan and the lender does a hard pull of your credit report, this impacts your credit score. The hard pull will impact the new credit piece of your FICO score.

Reviewing your report can help you identify the following:

- Mistakes: Sometimes, credit bureaus make mistakes, which could unfairly lower your FICO score. See below to learn about some common mistakes that could be made.

- Signs of fraud or identity theft: Strange accounts or loans you didn’t authorize could indicate identity theft. We've already talked about identity theft, but we will include more information in this lesson.

- Areas for improvement: A credit report can show where you might need to improve, like paying off high balances or making timely payments.

-

Credit bureaus can sometimes make mistakes on your credit report that could impact your credit score. Here are some common errors to watch out for:

- Incorrect Personal Information: Sometimes, credit reports have wrong names, addresses, or Social Security numbers due to data entry errors or similar names. This can lead to mix-ups in your credit history.

- Duplicate Accounts: A single loan or credit card may appear more than once on your report, which can make it look like you have more debt than you do.

- Outdated Information: Old or closed accounts can sometimes still show up as open or active. Additionally, paid-off debts may still appear outstanding if not updated.

- Incorrect Account Status: An account marked as delinquent or in collections when it’s actually current can hurt your score unnecessarily. This can happen because of reporting errors from creditors.

- Accounts That Aren’t Yours: Occasionally, accounts belonging to someone else can appear on your report, especially if you have a similar name or Social Security number. This can happen because of clerical errors or even identity theft.

- Wrong Payment History: Late payments can mistakenly appear even if you paid on time, negatively impacting your score.

- Inaccurate Public Records: Bankruptcies, tax liens, or foreclosures may be incorrectly reported or show up even if they’ve been resolved or dismissed.

As you’ve already learned, the law allows you to get one free credit report each year from each of the three major credit bureaus through AnnualCreditReport.com. Reviewing these reports regularly can help you stay aware of any changes and address potential issues quickly.

-

EXAMPLE

Let’s say you check your report and notice a credit card that you never opened. This could be a case of identity theft, where someone has used your information to obtain credit fraudulently. Catching this early allows you to dispute the charge and protect your FICO score.

In addition to monitoring, it’s also vital to take steps to protect yourself against identity theft. Let’s explore how.

4a. Identity Theft Safeguards

As we’ve established, identity theft and fraud can damage your credit score and take years to resolve. The time for credit recovery after identity theft varies:

- Quick Disputes (1–3 Months): Minor fraudulent charges often recover quickly after a dispute.

- Late Payments (6 Months–2 Years): Missed payments can take longer but lessen over time.

- High Balances/New Accounts (6 Months–1 Year): Once fraudulent balances are cleared, recovery can happen in about a year.

- Collections (1–2 Years): Collections due to fraud take longer to resolve but usually improve within 2 years.

- Severe Fraud (3–5 Years): Cases involving false bankruptcies or numerous accounts may take years to fully recover.

Now, let’s look at several strategies to help you avoid being a victim of identity theft.

- Use strong passwords: Avoid using easy-to-guess passwords (like 1, 2, 3), and update your passwords regularly.

- Beware of phishing scams: Don’t click on suspicious links in emails or messages claiming to be from your bank.

- Shred important documents: Dispose of financial statements or personal information securely.

- Consider a credit freeze: This restricts access to your credit report, making it harder for identity thieves to open new accounts in your name. This is a free option every credit card and bureau offers simply by calling and asking for it.

Identity theft can lead to fraudulent accounts, unpaid debt in your name, and a lower credit score. By protecting yourself, you also safeguard your FICO score from sudden drops due to unauthorized accounts or missed payments.

In this lesson, you learned what a FICO score is and how it is reported on a credit bureau report. You learned how your FICO score is calculated and why your FICO score matters. You also explored ways to establish credit. Finally, you discovered the importance of monitoring your credit report and learned about some identity theft safeguards.