Table of Contents |

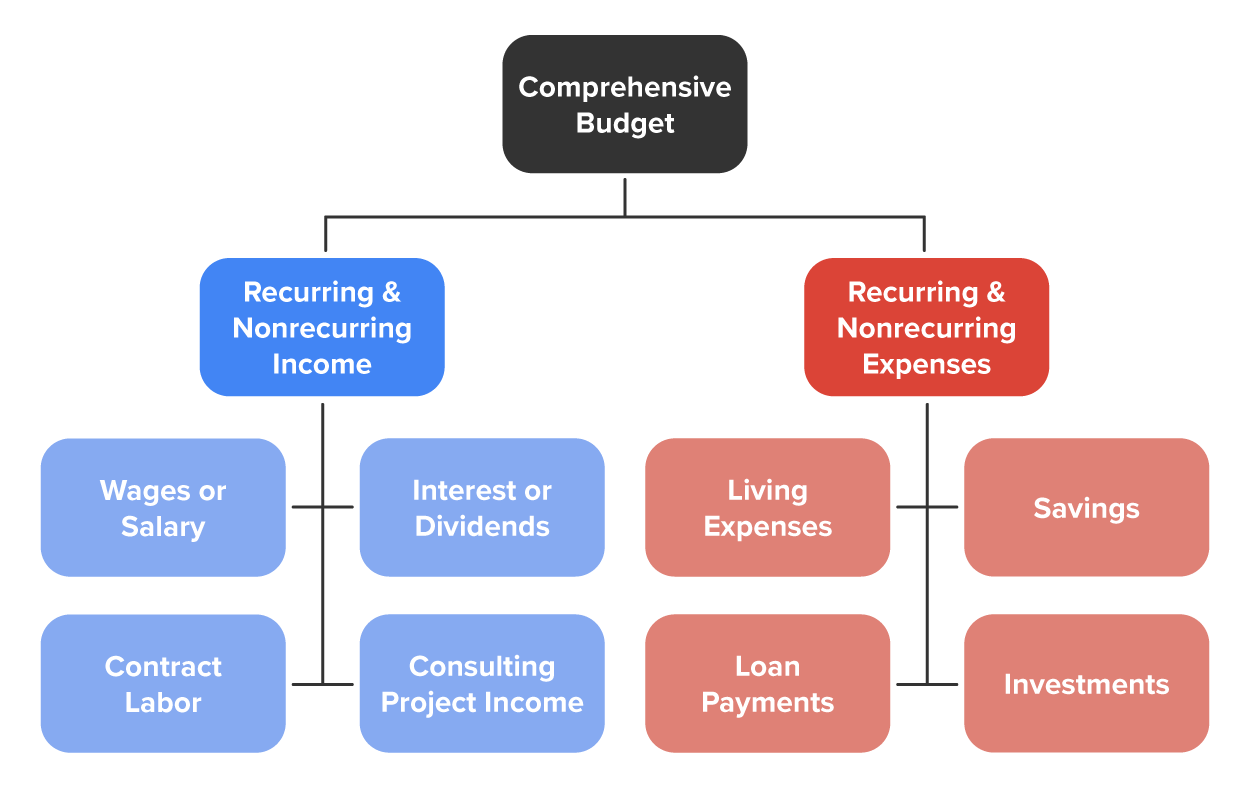

Now that you have mastered a simple monthly budget, ideally, you should create an annual budget that includes all recurring (continuing or repeating) and nonrecurring (irregular or one-time) income and expenses that are not incurred every month. Recurring income includes earnings from wages, interest, or investments, while nonrecurring income might be contract labor or consulting fees. Recurring expenses happen frequently and include rent, mortgage payments, and loan payments. Nonrecurring expenses are unexpected and include repairs to your car or house or the purchase of a replacement washer or dryer.

When you create a budget, you often forget to include nonrecurring expenses simply because you do not pay them regularly. Be careful not to overlook unusual income or expenses that happen irregularly, such as twice a year, quarterly, or only once a year. Nonrecurring expenses are often the cause of a deficit since they are not expected. These nonrecurring expenses are the reason you should create an emergency fund.

EXAMPLE

Auto insurance and real estate taxes are not paid monthly, and heating or air-conditioning expenses fluctuate every month. For this reason, personal budgets are usually estimated annually to take the timing of these factors into consideration.It is important to include these irregular items when creating an annual budget. The goal is to create an annual budget that you can then forecast into future years when planning and making financial decisions.

Now that you can create an annual budget, it is a good idea to forecast it to include more than 1 year of income and expenses. Comprehensive budgets (especially multiyear) are helpful for getting a more realistic picture of your finances. Taking the time to review your checking account or credit card statements for nonrecurring income or expenses will lessen the chance of budget errors or a surprise expense that causes stress and does not allow you to achieve your goals.

Multiyear budgets are helpful for observing trends over time and knowing whether you consistently have a budget surplus or deficit. Then, you can make adjustments as needed and plan for the future.

When forecasting estimated budgets for future years, you should include any expected future changes to your income or expenses. For example, expecting a child will increase your monthly expenses, or a promotion will raise your income. Personal situations can change, which will alter your income, expenses, choices, and progress toward goals.

Raychel

Manager at a grocery store

(Independent life stage, age 32)

Let’s revisit Raychel from the last lesson. She has converted her monthly budget to an annual one and added nonrecurring expenses and income. Raychel has also forecasted her budget over the next 2 years to create the comprehensive, multiyear budget shown below:

| 2024 | 2025 (Estimate) | 2026 (Estimate) | ||

|---|---|---|---|---|

| Gross Income | ||||

| Salary | $60,510.96 | $63,536.51 | $66,713.33 | |

| House Decorating/Painting | $4,500.00 | $6,000.00 | $8,000.00 | |

| Interest Income (From Savings Accounts) | $8.00 | $10.00 | $11.00 | |

| Total Gross Income | $65,018.96 | $69,546.51 | $74,724.33 | |

| Income Tax and Deductions (Withholdings) | ||||

| Income Tax | ||||

| Other Deductions | ||||

| Total Withholding | $10,250.04 | $10,762.54 | $11,300.67 | |

| Disposable Income | ||||

| $54,768.92 | $58,783.97 | $63,423.66 | ||

| Expenses | ||||

| Rent | $13,200.00 | $13,200.00 | $13,200.00 | |

| Food | $5,489.28 | $5,873.53 | $6,284.68 | |

| Auto Expenses | $3,879.96 | $3,879.96 | $3,879.96 | |

| Auto Insurance | $1,400.00 | $1,400.00 | $1,400.00 | |

| Electricity | $1,299.96 | $1,364.96 | $1,433.21 | |

| Phone & Internet | $1,740.00 | $1,827.00 | $1,918.35 | |

| Heating & Air Conditioning | $2,049.96 | $2,152.46 | $2,260.08 | |

| Health Care Expenses | $1,950.00 | $2,047.50 | $2,149.88 | |

| Auto Loan | $4,965.12 | $4,965.12 | $4,965.12 | |

| Student Loan | $3,000.00 | $3,000.00 | $3,000.00 | |

| Auto Repairs & Maintenance | $1,250.00 | $2,750.00 | $4,250.00 | |

| Unexpected Expenses (Buffer) | $2,500.00 | $2,500.00 | $2,500.00 | |

| Other Expenses | $8,278.80 | $8,692.74 | $9,127.38 | |

| Total Expenses | $51,003.08 | $53,563.27 | $56,368.65 | |

| Net Income (Surplus/Deficit) | $3,765.84 | $5,130.70 | $7,055.02 |

Note: For simplicity, you may have noticed that we populated the Total Withholding amount that Raychel has withheld from her Gross Income each year. We need to get the Disposable Income number to be able to finish this spreadsheet so it is automatically entered. You will learn more about taxes and deductions in a later lesson.

Note: Raychel built in $2,500 a year as “Unexpected Expenses (Buffer)” in case she has extra expenses. This gives her reassurance that her budget has some wiggle room.

As shown in the table above, Raychel modifies a few items when forecasting her budget over the next 2 years. She expects that:

As shown in her multiyear budget, Raychel’s 2024 annual disposable income, or take-home pay, is $54,768.92 after taxes and other deductions are withheld from her pay. After adding nonrecurring expenses and cushioning her expenses by $2,500 a year, her total expenses amount to $51,003.08, resulting in an annual surplus of $3,765.84.

Raychel’s forecasted budget over the next 2 years also results in annual surpluses. While her total expenses are expected to increase, so is her income.

Alternatively, the cause of a deficit may be something over which you have no control, such as job loss, accidents, or natural disasters. If the deficit is caused by rising expenses, this is the result of consuming more goods/services or an increase in the price of your purchases. A budget deficit may also be due to spending more than you can afford. The sooner you notice a budget deficit, the better. This allows you to make changes and put yourself back on track before you face financial hardship, where your credit could be damaged and borrowing for justified purchases in the future could be hindered. Finding the source of a deficit will determine the choices you have to solve the problem.

In the next lesson, you will look at what you can do to overcome a budget deficit and options for growing your wealth when you have a budget surplus.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.