Table of Contents |

Now that we have discussed the costs that are incurred by manufacturing companies and how to prepare their financial statements, we will learn about the functions and costs that are related to merchandising and service companies. Let’s start with the reporting income for a merchandising company.

A merchandiser is a business that sells merchandise or goods to customers, such as a bookstore or a grocery store.

Merchandisers are often identified as either wholesalers or retailers. A wholesaler is a merchandiser who buys goods from a manufacturer and then sells them to retailers.

EXAMPLE

McLane is a wholesale supply chain merchandiser. It buys food merchandise from manufacturers and distributes it to retailers, such as Walmart and 7-Eleven, which in turn sell the products to individual customers.A retailer buys merchandise either from a manufacturer or a wholesaler and then sells those goods to customers.

EXAMPLE

A retailer can be a major chain like Macy’s or Walmart, or it can be an individual shop or business. A gift shop might buy some merchandise from a wholesaler and other merchandise—perhaps more local goods—directly from the manufacturer.The operating cycle of a merchandiser begins when the company purchases inventory; they then sell the inventory to customers; and finally, they collect cash from customers.

The goods that merchandising companies sell are called the merchandise inventory and are recorded as such in the financial statements. When we report net income for a merchandising company, we record the revenue from the merchandise that was sold minus the cost of the merchandise and any other expenses that the company incurred. Net income is the remaining revenue after the company pays its expenses.

For a merchandiser, revenues are referred to as sales. The total expense of buying and preparing merchandise to be sold is referred to as the cost of goods sold (COGS; merchandising). When we dive into the financial statements later in the tutorial, we will see how COGS is incorporated into the income statement for a merchandising company.

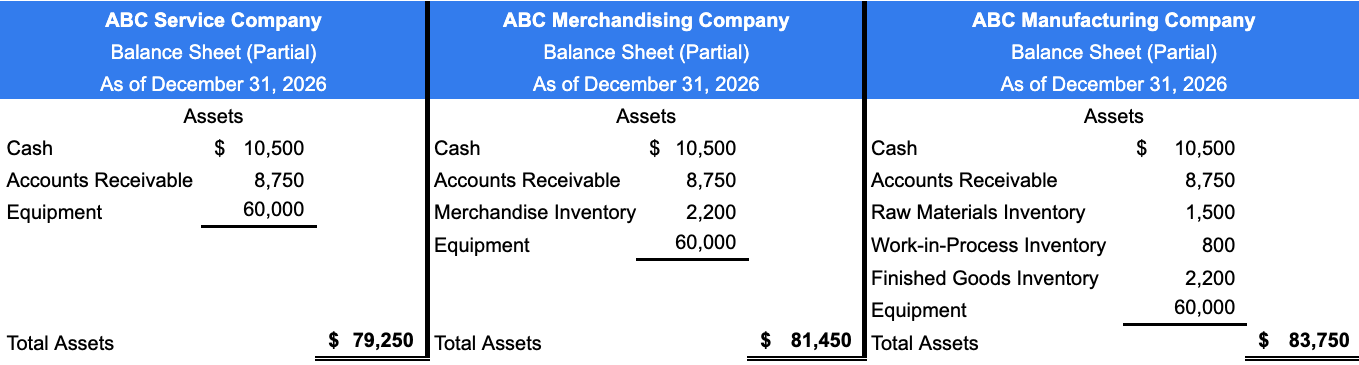

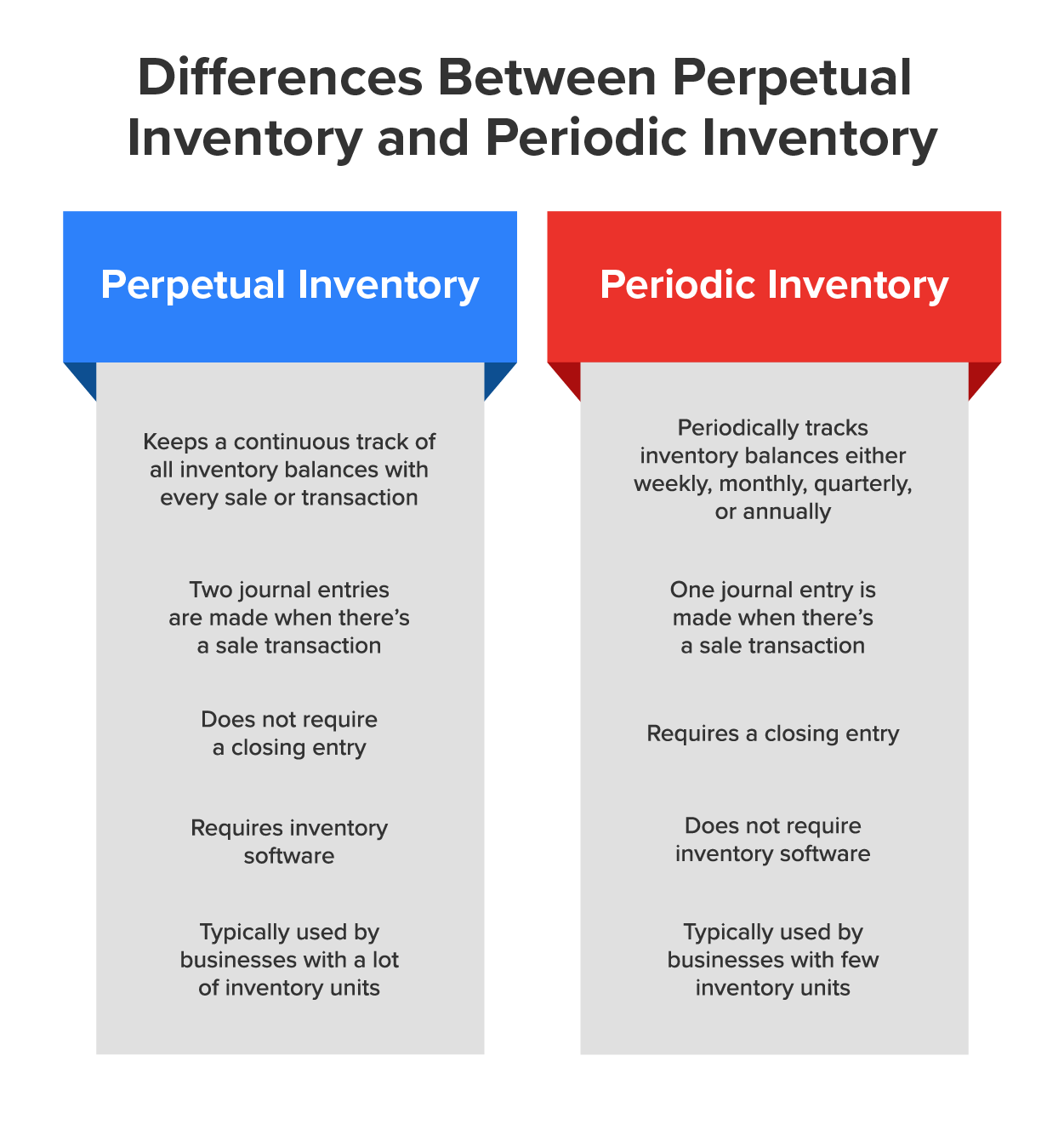

Merchandise inventory is recorded as a current asset on the balance sheet of a merchandising company. Companies need to have a method for determining the value of their merchandise inventory on hand and also the value of the merchandise inventory that they have sold. There are two main types of inventory accounting systems. The perpetual inventory system updates the accounting records for each purchase and sale of inventory and the periodic inventory system updates accounting records for purchases and sales of inventory at the end of the accounting period.

A perpetual inventory system automatically updates the inventory account every time a sale occurs. This system is often referred to as “recording as you go.” The recognition of each sale happens immediately upon the sale of the merchandise. The perpetual inventory system keeps a running computerized record of the merchandise inventory. Many retail establishments use a perpetual inventory system to keep an ongoing record of their inventory.

EXAMPLE

When a customer purchases socks at Walmart and the cashier scans the barcode, the inventory is updated immediately. The inventory might track the socks by brand, style, or both in order to be able to replenish the inventory for the socks that were sold.This system achieves good control over the inventory, given that it updates records as transactions take place. Technology has increased the use of the perpetual system because it gives managers immediate access to sales and inventory levels, giving them the ability to set goals and strategies based on these numbers.

A modern perpetual inventory system records the following:

Merchandising companies require adjusting entries for inventory, sales discounts, and sales returns and allowances for theft or deterioration of merchandise. When the perpetual inventory system is used, an adjusting entry to the merchandise inventory is created to show any loss of merchandise due to theft or deterioration. According to the revenue recognition principle, discussed in a prior lesson, sales are recorded at the amount expected to be received. Because of this, we make adjusting entries for expected sales discounts and expected returns and allowances due to product defects.

IN CONTEXT: Point-of-Sale Systems

Many retailers use point-of-sale (POS) systems to manage their inventory. These computerized systems allow merchandising companies to have a running total of their inventory on hand along with the cost of the inventory on hand. POS systems allow companies to manage their inventory by knowing what their highest-selling items are, what items need to be replenished, and what items are bringing in the most money. All of these factors will help managers to make effective decisions related to the company’s inventory.

A common POS system is Square. Square can be used by merchandising companies to update inventory and accounting records each time a sale occurs. Given that it is a cloud-based application that can be accessed from anywhere, Square has become a valuable resource for merchandising companies to record sales, accept payments, and manage inventory.

The periodic inventory system requires updating the inventory account only at the end of a period to get a physical count of the inventory and determine the quantities on hand. The periodic system might be used along with a perpetual inventory system to make sure that the physical count matches the information from the sales and purchases that are recorded as they occur. When the periodic inventory system is used alone, it is typically used for small stores that do not have a lot of inventory on hand. This method is not very widely used given that the perpetual inventory system is computerized.

When the periodic inventory system is used, the merchandise inventory balance remains the same until the company counts and verifies the inventory balance. A physical count is typically completed at the end of the year but could be completed sooner if shortages are noticed. The purchases account is updated to reflect the cost of all purchase transactions that occurred during the period. The merchandise inventory account balance is reported on the balance sheet, and the purchases account is reported on the income statement when the periodic inventory method is used.

Unlike the perpetual inventory system, the periodic inventory system requires a closing entry to update the inventory amounts to reflect the actual count that was conducted at the end of the year.

The following is a chart that shows the differences between the perpetual and periodic inventory systems that are used by merchandising companies.

A merchandising company will prepare the income statement, balance sheet, and statement of owner’s equity.

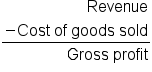

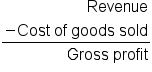

Merchandisers use the multistep income statement to show the company’s net income or loss. The multistep income statement is an income statement format that has subtotals for reporting gross profit and operating income in addition to net income or loss. Gross profit is the amount of revenue that remains after we account for the costs of the goods that were sold to create the revenue.

Gross profit and net income measure a business’s success because they tell us how much profit the company is bringing in. Having a high gross profit is important to a merchandiser because the profit allows them to continue to purchase and sell merchandise with the goal of continuous growth.

EXAMPLE

Gary’s Grocery Mart collected revenue of $10,000 in the month of January, and it cost him $3,000 to purchase the products that he sold. His gross profit for the month is $7,000. ($10,000 revenue $3,000 COGS

$3,000 COGS  $7,000 gross profit)

$7,000 gross profit)

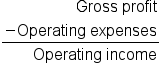

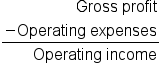

After calculating the gross profit, operating expenses are then deducted to determine the net income.

Operating expenses are expenses, other than COGS, that are incurred through the company’s daily operations. These expenses can be categorized as either selling expenses or administrative expenses.

Selling expenses are expenses that are related to marketing and selling the company’s goods and services, such as the salesperson’s commission or the vehicle that the salesperson drives.

EXAMPLE

For Gary’s Grocery Mart, selling expenses would include buying ads in the local newspaper, paying a sign maker to create signs that advertise sales to passersby, and providing salaries for cashiers and stockers.Administrative expenses are any other expenses that are not related to marketing the company’s goods and services. These expenses include office expenses, depreciation on the building and equipment, rent for the administrative office, and utilities for the administrative office. These administrative expenses are incurred behind the scenes, separate from a retail establishment. For most merchandising companies, there is a separate location that houses administrative offices including managers, accountants, and human resources personnel.

EXAMPLE

Gary’s Grocery Mart incurs administrative expenses for the rent and utilities that are associated with the administrative building that contains the offices of the company manager, the accountants, and human resources.Operating income tells us the income that is related to the company’s normal operations. It is calculated by subtracting the operating expenses from the gross profit. It is important to note the difference between operating income and net income. Operating income shows us the gross profit minus the operating expenses while net income considers both operating expenses and nonoperating expenses such as interest expenses and tax expenses.

The last section of the multistep income statement records nonoperating activities.

Nonoperating activities include other expenses, revenues, losses, and gains that are not related to the company’s operations. Other revenues and gains might include interest revenue, dividend revenue, or gains from the disposal of assets. Other expenses and losses consist of interest expenses and losses from asset disposals. If the company does not have nonoperating activities, its income from operations is only its net income.

On the balance sheet, a merchandising company includes merchandise inventory in the current assets section, representing the value of inventory that the company has on hand to sell to customers. The balance sheet will also include an asset account for estimated returns inventory. The merchandising company will also have an additional current liability account for refunds payable to show the estimated amount of refunds that are due.

The statement of owner’s equity does not have any changes from the traditional statement of owner’s equity. The statement of owner’s equity reports the owner’s contributions, owner’s draws, and dividend payouts.

A service company sells services such as time, skills, and knowledge rather than products. The service industry is an important part of the United States economy, making up a large part of the job sector and providing the population with services that are necessary within their daily lives. A service company does not have physical inventory since they are providing a service to customers rather than a product. Service companies might include accounting firms, law firms, airlines, or hospitals.

A typical operating cycle for a service company begins with having cash available, providing service to a customer, and then receiving cash from the customer for the service that was provided. The faster this cycle is completed, the more stable the company’s financial position will be. Service companies typically have simple financial transactions that involve billing customers, collecting deposits, providing the service, and collecting payment for the service that was provided. These activities will happen frequently within the accounting cycle and will be reflected in the company’s financial statements.

Financial statements for a service company are more simplified than those for a manufacturing or merchandising company. Service companies generally do not have inventory that needs to be accounted for but might have expenses for the supplies purchased and used to complete the services they provide. An exception to this might be a plumber or electrician who might keep an inventory of supplies or tools they use on a regular basis.

The income statement lists the service revenue that has been collected from the services that were provided to customers and the expenses that are related to the daily operations of the company. Some expenses that might be reported on the income statement are salary expenses, rent expenses, and/or marketing expenses. COGS is not reported because there is no physical product that is being sold. On the balance sheet, the main difference for a service company is that it does not report inventory as an asset since it does not carry inventory that will be sold to customers.

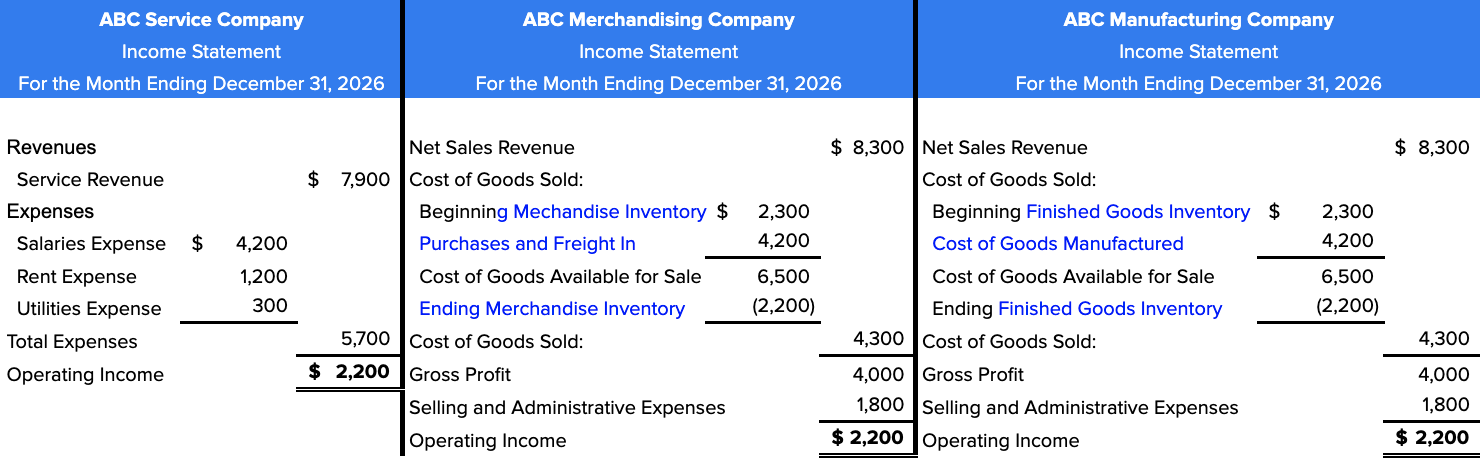

Below, we will find a comparison of the income statement and balance sheet for manufacturing, merchandising, and service companies.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.