In this lesson, you will learn how corporate governance establishes accountability and ethical conduct within organizations. You’ll explore the principles and regulations that shape how companies operate, protect stakeholders, and maintain transparency in financial management. You’ll also examine the Sarbanes-Oxley Act and other major frameworks that define modern governance standards. Specifically, this lesson will cover:

1. Defining Corporate Governance

Corporate governance refers to the framework of rules, practices, and processes by which a company is directed and controlled. It defines the relationships among a company’s management, board of directors, shareholders, and other stakeholders. Some of what corporate governance encompasses are:

- regulatory and market mechanisms that influence corporate behavior.

- roles and relationships among a company’s management, board of directors, shareholders, and other stakeholders.

- goals for which a corporation is governed: ensuring that these goals are pursued in responsible, transparent, and accountable manners.

In finance, strong corporate governance is essential for maintaining investor confidence, ensuring accountability, and promoting long-term financial health.

![The four pillars of corporate governance: accountability, transparency, responsibility, and fairness.]](https://cdn2.sophia.org/markup_pictures/40939/file/e7aa2dc1db73816d79cd4fd5134af9c4.png) alt=The four pillars of corporate governance: accountability, transparency, responsibility, and fairness.]

alt=The four pillars of corporate governance: accountability, transparency, responsibility, and fairness.]

The following principles serve as the foundations of ethical and sustainable corporate governance practices.

-

Accountability: the obligation of individuals and organizations to be answerable for their actions. Executives and board members must be accountable to shareholders and other stakeholders for the decisions they make. Financial managers are expected to ensure that company resources are used efficiently and ethically.

-

Transparency: the open and honest disclosure of relevant financial and operational information. It ensures that investors, regulators, and the public have access to accurate and timely data about a company’s performance and governance practices. In finance, transparency is critical for fair valuation, risk assessment, and informed decision making.

-

Responsibility: the ethical and legal duties that corporate leaders have toward stakeholders. This includes not only maximizing shareholder value but also considering the impact of business decisions on employees, customers, communities, and the environment. Financial managers play a key role in upholding this pillar by ensuring compliance with laws and regulations, managing financial risks, and aligning financial strategies with the company’s long-term goals.

-

Fairness: the treating of all stakeholders equitably and justly. In finance, this includes ensuring that shareholders have equal access to information. Fairness also extends to how companies interact with customers, suppliers, and employees. A fair governance structure promotes inclusivity, reduces conflicts of interest, and supports a culture of integrity. When fairness is embedded in corporate practices, it enhances stakeholder loyalty and long-term value creation.

Together, these four pillars form the foundation of sound corporate governance, which is essential for financial stability and investor trust. In financial management, they guide how capital is raised, allocated, and reported. Companies that uphold these principles are better positioned to manage risk, attract investment, and achieve sustainable success.

- Corporate Governance

- The roles of and relationships between a company’s management, board, shareholders, and other stakeholders, as well as the goals for which the corporation is governed. Much of the contemporary interest in corporate governance is concerned with the mitigation of conflicts of interest and the nature and extent of accountability of the people in the business.

- Stakeholders

- A person or organization with a legitimate interest in a given situation, action, or enterprise.

- Conflicts of Interest

- Occur when an individual or organization is involved in multiple interests, one of which could possibly corrupt the motivation for an act in the other.

2. Principles

Sound, ethical principles of corporate governance play a vital role in financial management by ensuring that companies are run in a way that is transparent and accountable to stakeholders. Over the past few decades, several major reports and regulations have shaped how companies around the world approach governance. These frameworks help protect investors, promote financial integrity, and support long-term business success.

The Cadbury Report (United Kingdom, 1992)

Published in response to a series of high-profile corporate failures in the UK, the Cadbury Report emphasized the importance of board structure, internal controls, and the separation of the roles of CEO and chairperson. It introduced the concept of “comply or explain,” encouraging companies to follow governance codes or publicly justify deviations. This report laid the foundation for many governance codes adopted across Europe and beyond.

OECD Principles of Corporate Governance (1999, revised 2004)

Issued by the Organization for Economic Co-operation and Development, these principles provide an international benchmark for policymakers, investors, and corporations. They cover key areas such as shareholder rights, equitable treatment of stakeholders, disclosure and transparency, and the responsibilities of the board. The OECD principles are widely used by both developed and emerging economies to guide corporate governance reforms.

The Sarbanes-Oxley Act (United States, 2002)

Enacted in the wake of major accounting scandals like Enron and WorldCom, the Sarbanes-Oxley Act (SOX) introduced sweeping reforms to improve corporate accountability and financial transparency. Key provisions include stricter requirements for financial reporting, internal controls, and auditor independence. More information about SOX is available in the following sections.

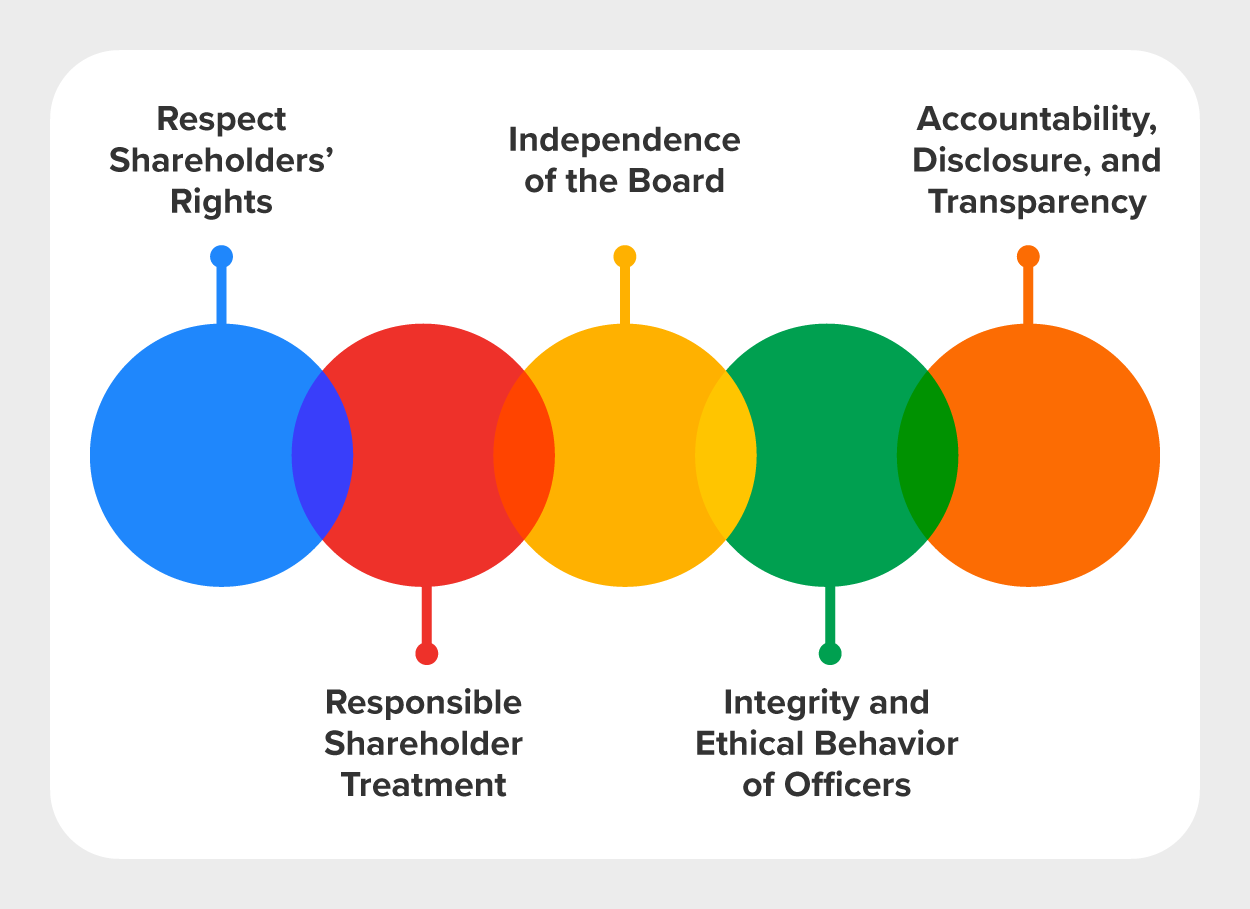

Together, these documents have shaped the global conversation around corporate governance, leading to how companies think about the following:

-

Shareholder Rights and Engagement: Companies must uphold and protect the rights of shareholders, ensuring they have the information and opportunities needed to participate meaningfully in corporate affairs. This includes clear communication, timely disclosures, and encouraging active involvement in annual general meetings and key decision-making processes.

-

Respect for Stakeholders: Beyond shareholders, companies have responsibilities to a broader group of stakeholders (employees, creditors, suppliers, and local communities). Good governance requires honoring these relationships through ethical practices, legal compliance, and socially responsible behavior that supports long-term sustainability.

-

Effective Board Oversight: A well-functioning board of directors is essential for monitoring management and guiding corporate strategy. Board members should possess relevant expertise, maintain independence, and commit sufficient time and attention to their roles.

-

Integrity and Ethical Conduct: Integrity is a cornerstone of corporate leadership. Companies should establish and enforce a code of conduct that promotes ethical behavior among executives and board members. This includes setting clear expectations for responsible decision making and fostering a culture of honesty and accountability.

-

Transparency and Disclosure: Transparency builds trust. Companies should clearly define and communicate the roles of the board and management, and ensure that financial reporting is accurate, timely, and accessible. Disclosure of material information must be balanced and fair, giving all investors equal access to facts that influence financial decisions.

<figure class="markup-center" style=""><img src="

https://cdn2.sophia.org/markup_pictures/41222/file/00d37fd8925dfe70ce40c0b935fe012f.png" title="The principles of corporate governance"></img><figcaption>The principles of corporate governance</figcaption></figure>

PepsiCo is a global leader in the food and beverage industry. It has also been noted for its excellence in corporate governance. Take a look at the PepsiCo website. Why do you think the company has won numerous awards and was featured in Fortune’s annual Blue Ribbon Companies list?

3. Sarbanes-Oxley Act of 2002

As mentioned in the previous section, the Sarbanes-Oxley Act of 2002 (SOX) is a federal law that sets standards for all domestic company boards of directors and management and accounting firms. This act is essential to study, because it fundamentally reshaped the financial landscape in the United States and set new standards for corporate accountability, transparency, and ethical financial reporting.

IN CONTEXT

The Sarbanes-Oxley Act, named after its sponsors, U.S. Senator Paul Sarbanes (D-MD) and U.S. Representative Michael G. Oxley (R-OH), was enacted to restore public trust in financial markets and to protect investors from fraudulent financial reporting by corporations. SOX was a response to a series of high-profile financial scandals that exposed significant weaknesses in corporate governance and financial reporting. The most notable of these scandals involved major corporations such as Enron, WorldCom, and Tyco, where fraudulent accounting practices led to massive financial losses for investors and employees.

Enron’s case was particularly influential in spurring the creation of SOX. The energy company used complex accounting loopholes to hide debt and inflate profits, misleading investors and analysts about its true financial health. When these deceptions came to light, Enron declared bankruptcy, devastating shareholders and employees and shaking trust in U.S. financial markets.

The changes enacted by Sarbanes-Oxley included the following:

- Establishing the Public Company Accounting Oversight Board in order to provide independent oversight of accounting firms and audits

- Establishing standards for the independence of external auditors, including new auditor approval and reporting requirements

- Mandating that senior executives take personal responsibility for the accuracy of financial reports, including the definition of the relationship between external auditors and corporate audit committees

- Setting reporting requirements for financial transactions, including off-balance-sheet transactions, pro forma figures, and stock transactions of corporate officers

- Restoring investor confidence in securities analysts by requiring disclosure of conflicts of interest

- Requiring the comptroller general and the SEC to study and report on the effects of consolidation of accounting firms and the role that credit rating agencies play in the markets

- Defining specific criminal penalties for manipulation of financial records while also providing certain protections for whistleblowers

- Setting criminal penalties associated with white-collar crimes and recommending stronger sentencing guidelines making failure to certify corporate financial reports a criminal offense

- Requiring that the chief executive officer sign the company tax return

- Audits

- The verification of the financial statements of a legal entity intended to enhance the degree of confidence of intended users in the financial statements by providing reasonable assurance that the financial statements are presented fairly.

- External Auditor

- An audit professional who performs an audit of the financial statements of a company, government entity, or other legal entity or organization in accordance with specific laws or rules and who is independent of the entity being audited.

In this lesson, you defined corporate governance, which is the system of rules and relationships that direct and control a company, ensuring accountability, transparency, and fairness among management, the board, shareholders, and stakeholders.

You also examined principles of corporate governance, including the four pillars that support ethical business conduct and investor trust: accountability, transparency, responsibility, and fairness. This section also introduced key global frameworks such as the Cadbury Report, OECD Principles, and Sarbanes-Oxley Act, which strengthen board oversight, shareholder rights, and ethical standards across organizations.

Finally, you investigated the Sarbanes-Oxley Act of 2002, a U.S. law enacted in response to corporate scandals like Enron and WorldCom, which established stricter auditing standards, executive accountability, and criminal penalties for fraud.

Together, these frameworks reinforce the importance of strong governance in maintaining ethical leadership, accurate financial reporting, and long-term investor confidence.

{kind=link}