Table of Contents |

Eligible taxpayers with one or more qualifying persons must file Schedule EIC in order to claim the Earned Income Credit (EIC). Taxpayers eligible for the EIC who do not have a qualifying person do not complete this form.

Schedule EIC calls for information about the qualifying person or persons. If a taxpayer has more than three qualifying persons, they enter information about only three of them.

EXAMPLE

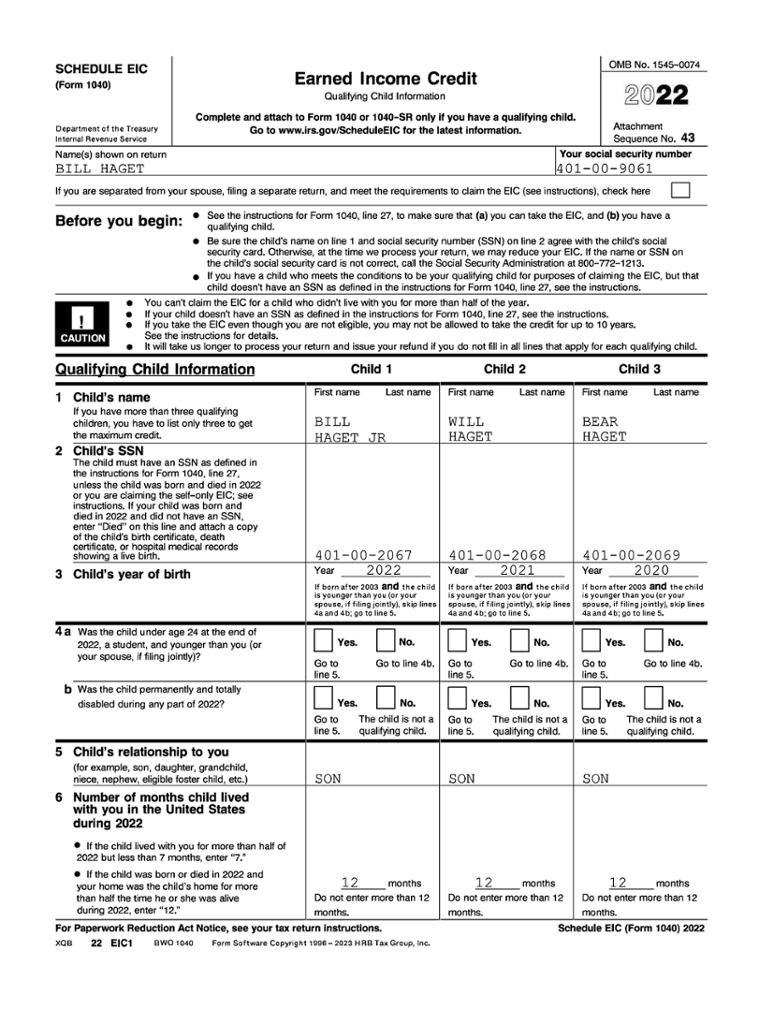

This year, Bill Haget (56), single, is filing Form 1040 claiming the head of household filing status. He has five qualifying children under age 19, all of whom are also qualifying persons for EIC. His earned income and adjusted gross income are $33,810, and his tax before credits is $1,519.

The Earned Income Credit is calculated using one of two worksheets. Before computing the amount of the credit, however, the EIC qualifications must be considered. It may be helpful to follow the six steps below to determine the amount of EIC for a taxpayer.

Determine whether the taxpayer’s investment income exceeds the maximum of $10,300. Add the amounts from Form 1040, lines:

Determine:

Determine:

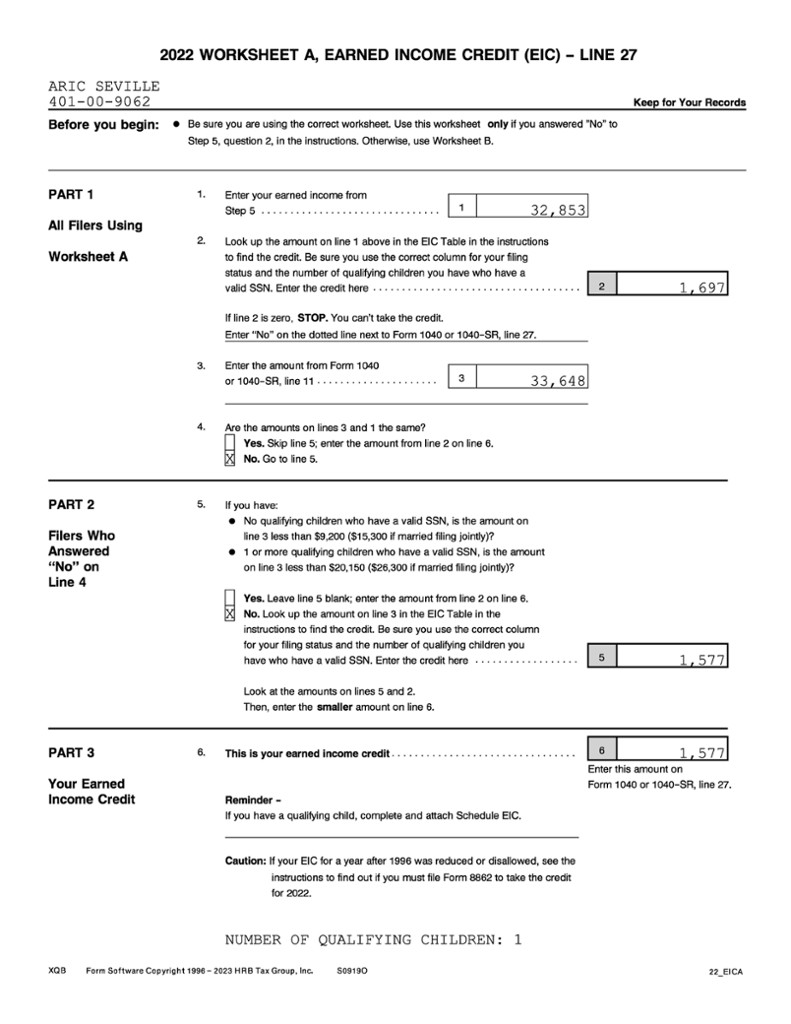

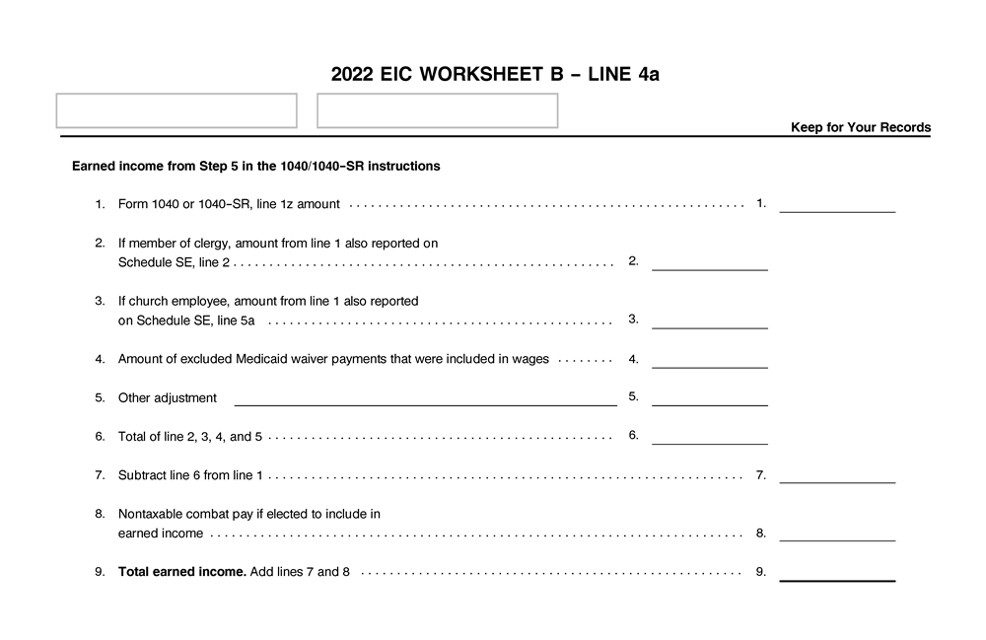

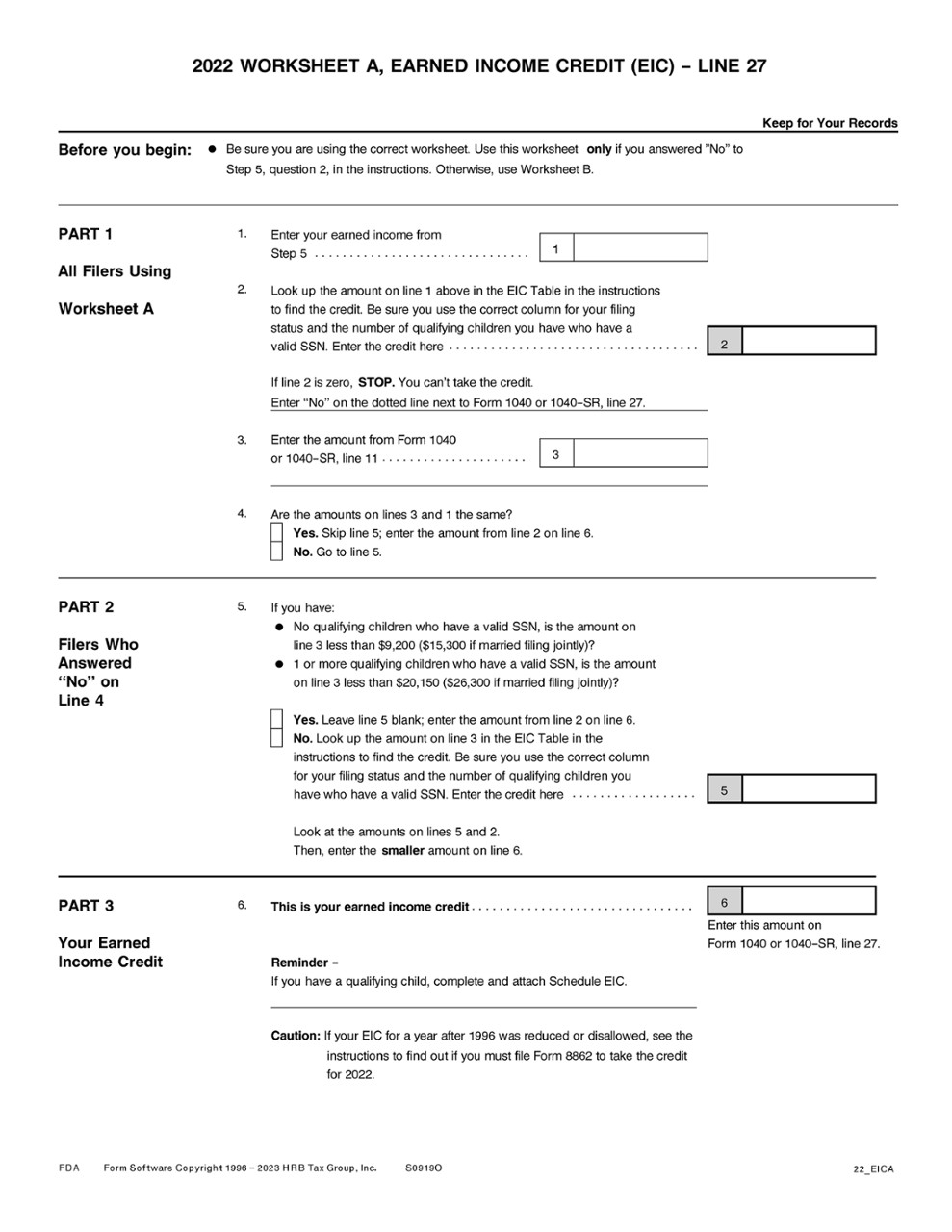

The 2022 EIC Worksheet B – Line 4a (Form 1040 Instructions, Step 5, Earned Income) and 2022 Worksheet A, Earned Income Credit (EIC) – Line 27 (shown below) are used to compute the amount of Earned Income Credit.

Enter the taxpayer’s earned income from Form 1040 on line 1. Lines 2 through 8 will not be covered in this course, so they will be left blank, zero will be entered on line 9, and the amount from line 1 will be entered on line 10. Then, any nontaxable combat pay will be entered on line 11 if the taxpayer elects to include that in their earned income, and their total earned income is entered on line 12.

In Part 1, enter the taxpayer’s earned income from Form 1040 on line 1, then look up that amount in the EIC Tables and enter it on line 2. As with the tax tables, be sure to use the correct column for the taxpayer’s filing status and number of children.

Next, the taxpayer’s adjusted gross (AGI) income is entered on line 3 and compared to their earned income on line 1. If they are the same, the amount from the EIC tables on line 2 is entered on line 6, and this is their Earned Income Credit.

If the taxpayer’s earned income and AGI are different, Part 2 is used to look up their EIC based on their AGI.

The smaller of the two potential EIC amounts is entered on line 6 of the worksheet and carried to their Form 1040.

IN CONTEXT: EIC Worksheet B

If the taxpayer is self-employed at any time in 2022, or if they are filing a Schedule SE because they are a member of the clergy or a statutory employee filing Schedule C, they will complete 2022 Worksheet B, Earned Income Credit (EIC) – Line 27a, instead of Worksheet A, Earned Income Credit (EIC) – Line 27a. This worksheet is beyond the scope of this course.

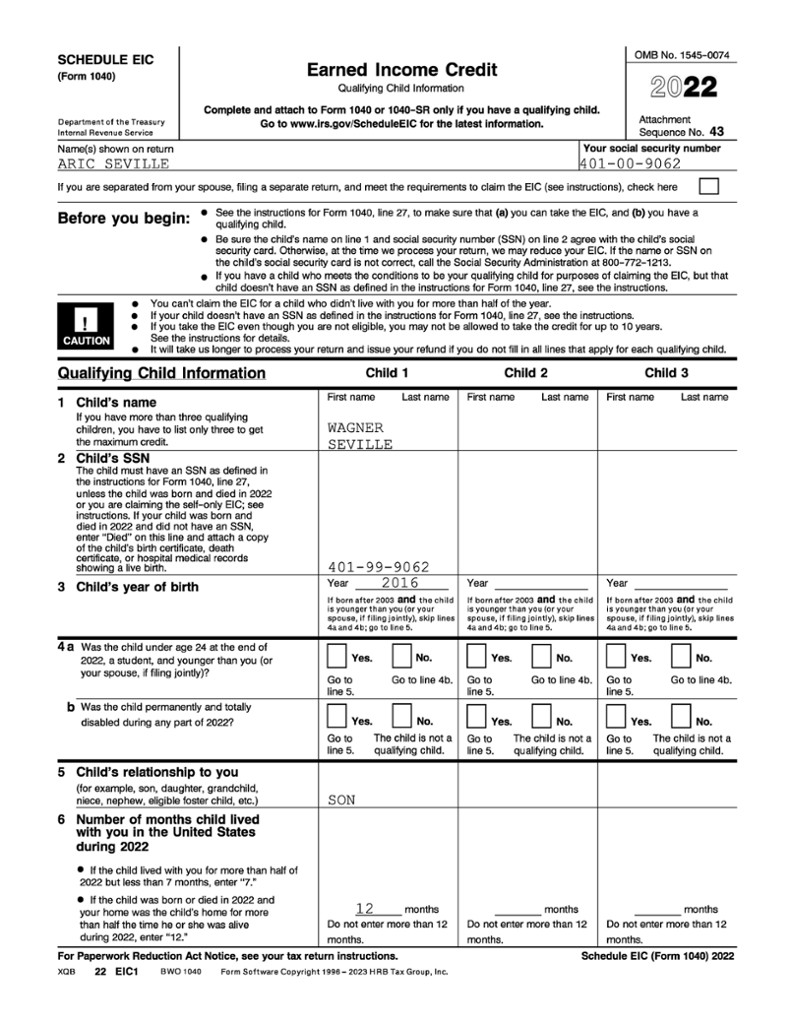

EXAMPLE

Aric Seville files as qualifying surviving spouse and qualifies for the EIC for the tax year. He has one qualifying child, his son Wagner, born in 2016. Wagner lived with Aric all year. Aric’s Schedule EIC is shown below.