In this lesson, you will learn how to assess your health insurance needs and compare health plan categories. Specifically, this lesson will cover the following:

1. Assessing Your Health Needs

You already know that health insurance is confusing, expensive, and—let’s be honest—something we’d all rather not think about until we have to. But here’s the deal: Choosing the wrong plan can cost you thousands, limit your access to the care you need, and leave you scrambling when a medical emergency happens. The right plan? It can protect your health, your finances, and your peace of mind.

Yet, with so many options, confusing terms, and fine print, how do you actually choose the right one? Should you go for the cheapest monthly premium? The one your employer recommends? Or the plan with the lowest deductible?

Before you even look at plans, you need to take a personal inventory. Think of it like shopping for a car—are you someone who needs an SUV for road trips or a compact car for city driving? Health insurance works the same way. What you need in a plan depends on how you use health care.

-

Ask yourself the following questions:

- How often do I go to the doctor (once a year, every few months, etc.)?

- Do I have any chronic conditions that require ongoing care or medication?

- Do I take prescription medications regularly? If so, how expensive are they without insurance?

- Do I have a preferred doctor or specialist that I want to keep seeing?

- Am I planning on having a baby or needing maternity care in the near future?

- Do I travel frequently and need coverage outside my local area?

If you’re generally healthy and only see a doctor for routine checkups, a lower-cost plan with a higher deductible might work for you. But if you have ongoing medical needs—like managing a chronic illness or requiring regular prescriptions—opting for a plan with a higher monthly premium but lower out-of-pocket costs could save you thousands over time.

Knowing your health-care habits helps you avoid overpaying for coverage you don’t need—or worse, ending up with a plan that doesn’t cover the care you do need. Now, let’s explore how to compare health insurance plan categories.

-

To see how this plays out in real life, let’s look at two people with very different health-care needs based on the health plans you learned about in the previous lesson:

Alex is 28 years old, is generally healthy, and only goes to the doctor for an annual checkup and the occasional cold. Alex doesn’t take any regular medications and rarely needs medical care. Because of this, Alex chooses a high-deductible health plan (HDHP) with a lower monthly premium but higher out-of-pocket costs. This plan saves Alex money each month, and since they don’t use health care often, they don’t mind paying a bit more if they do need care. Plus, Alex can contribute to a health savings account (HSA) for future medical expenses.

Taylor is 35 years old and has been managing asthma and migraines that require regular doctor visits and prescription medication. Taylor also sees a specialist a few times a year. Because of these ongoing health-care costs, Taylor chooses a PPO plan with a higher monthly premium but lower co-pays for doctor visits and prescriptions. Even though Taylor pays more per month, they save money in the long run because their plan covers more of their routine care.

Think about your health-care situation. Are you more like Alex, with minimal health-care needs? Or do you have ongoing medical expenses like Taylor?

- If you only go to the doctor once in a while, a lower-premium, high-deductible plan might be a smart choice.

- If you have chronic conditions, need frequent prescriptions, or want access to a broader range of doctors, a plan with a higher monthly cost but better coverage could be worth it.

By knowing your health needs, you can confidently choose a plan that fits your lifestyle and your budget—without surprises down the road.

2. Compare Plan Categories

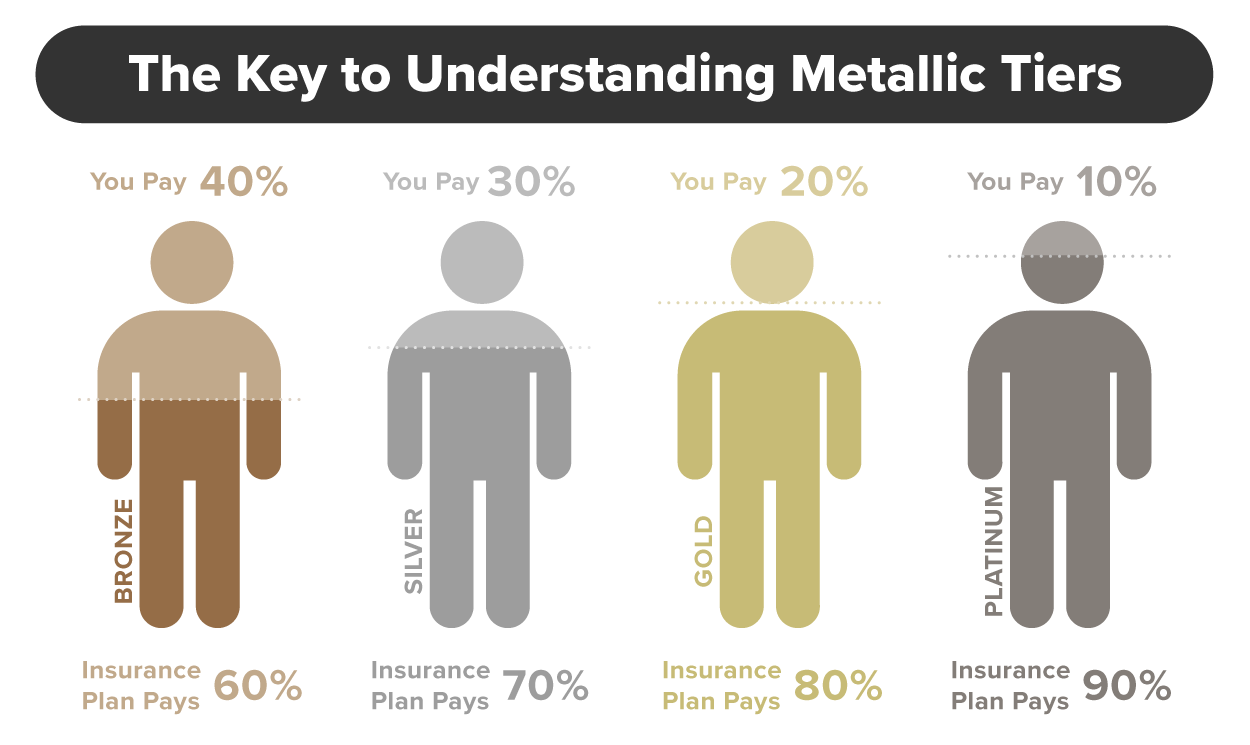

Think of health insurance like a menu—you’ve got different options, and each one balances cost and coverage in a unique way. Some plans have lower monthly costs but higher expenses when you actually use them, while others cost more up front but cover more when you need care. These categories, known as metal tiers, tell you how costs are split between you and the insurance company.

Let’s break it down with a simple analogy: ordering food at a restaurant.

-

Bronze = Fast food: Cheap up front, but if you want extras (like fries or a drink), you’ll have to pay for them. This plan has low monthly premiums but high deductibles and out-of-pocket costs when you actually use health care. It’s best for people who rarely go to the doctor and want the lowest monthly payments.

-

Silver = A casual restaurant: You pay a moderate price for a meal that includes a side so you’re not paying for every little thing separately. These plans have moderate premiums and deductibles, striking a balance between cost and coverage. If you qualify for subsidies, a Silver plan can be the best deal because it includes cost-sharing reductions, which lowers out-of-pocket costs even more.

-

Gold = A sit-down restaurant with full service: You’re paying more up front but you get quality and convenience. A Gold plan has higher monthly premiums but lower out-of-pocket costs when you get care, making it ideal for those who visit the doctor regularly or need frequent prescriptions.

-

Platinum = A fancy, all-inclusive meal: It costs the most, but everything is covered and you don’t have to worry about surprise expenses. These plans have the highest monthly premiums but the lowest deductibles and co-pays, making them the best choice for people with high medical needs or ongoing treatments.

Choosing the Right Tier for You

- If you’re young, healthy, and don’t visit the doctor often, a Bronze plan keeps your monthly costs low—just be prepared for high deductibles if you do need care.

- If you want a balance between monthly costs and coverage, Silver is often a solid middle-ground option, especially if you qualify for subsidies.

- If you have regular medical expenses and prescriptions or see specialists, Gold might save you more in the long run.

- If you have a chronic condition or anticipate major health-care needs, Platinum gives you the most coverage with the least out-of-pocket costs.

-

Health insurance can feel expensive, but if you’re buying a plan through the Health Insurance Marketplace (Healthcare.gov or your state’s exchange), you might qualify for financial help that lowers your costs. There are two main types of assistance:

1. Help Paying Your Monthly Premium

If your income falls within a certain range, you may qualify for a discount on your monthly payment called a

premium tax credit. This means that the government helps cover part of your health insurance bill, so you pay less each month.

- The less you make, the bigger the discount.

- You can apply the discount up front to lower your monthly payment, or you can choose to pay full price and get the savings as a refund when you file your taxes.

-

EXAMPLE

Without help, a Silver plan might cost $500 per month.

With a tax credit, your cost could drop to $100 per month.

- 2. Help Lowering Your Out-of-Pocket Costs

- If you qualify, you can also get extra savings that lower what you pay when you go to the doctor, pick up prescriptions, or need medical care. These savings are called cost-sharing reductions and are only available with Silver plans.

-

- They lower your deductible, which is the amount you have to pay before insurance starts covering your care.

- They also reduce your co-pays (the fee you pay for doctor visits) and your overall out-of-pocket costs.

-

EXAMPLE

Without extra savings, you might have a $3,500 deductible.

With cost-sharing reductions, your deductible could be as low as $500 or even $0.

- How to Find Out if You Qualify

- Go to HealthCare.gov or your state’s health insurance website. Enter your income, and it will tell you how much help you can get.

- Even if you think health insurance is too expensive, check to see if you qualify for financial assistance. Many people pay much less than they expect, but you won’t know unless you look.

How Metal Tiers Relate to Workplace Health Insurance

These metal tier categories primarily apply to individual health plans purchased through the Health Insurance Marketplace (ACA/Obamacare), but the same cost versus coverage trade-offs also exist in workplace health insurance plans.

-

ACA stands for the Affordable Care Act, informally known as Obamacare, which is a law established by the U.S. government in 2010 to expand access to health insurance and reduce the costs of coverage.

Most employer-sponsored health insurance doesn’t explicitly use Bronze, Silver, Gold, and Platinum labels, but you’ll still encounter different plan options with varying premiums, deductibles, and out-of-pocket costs. Here’s how they typically compare to workplace plans:

- Bronze (Similar to HDHPs)

- Lower monthly premiums

- High deductibles and out-of-pocket costs

- Often comes with an HSA

- Best for employees who are young, healthy, and rarely use health care

- Silver (Standard PPOs and HMOs)

- Moderate premiums and deductibles

- A balance of coverage and out-of-pocket costs

- Ideal for employees who use medical services occasionally

- Often the middle-tier option if your employer offers multiple plan levels

- Gold (Lower-Deductible PPOs and HMOs)

- Higher monthly premiums but lower out-of-pocket costs

- Covers more services before hitting the deductible

- Best for employees with chronic conditions, frequent doctor visits, or regular prescriptions

- Platinum (Premium PPOs and HMOs)

- The highest monthly premium

- Lowest deductible and out-of-pocket costs

- Best for employees with major medical needs, ongoing treatments, or expensive prescriptions

Even though workplace health insurance doesn’t always use metal-tier labels, the same cost-versus-coverage principles apply. If you’re choosing between multiple employer-sponsored plans, think about how often you use health care, your prescriptions, and your budget to find the best fit—just like you would in the Marketplace.

Once you’ve compared your health insurance plan categories, it’s time to compare the costs of your health plan options to figure out which one is best for you.

-

- Bronze Plan

- Lowest monthly costs but highest out-of-pocket expenses. Best for healthy individuals who rarely need care.

- Silver Plan

- Moderate monthly costs and balanced coverage. Best for those who qualify for financial help as it can lower overall costs.

- Gold Plan

- Higher monthly costs but lower out-of-pocket expenses. Best for people who need frequent medical care.

- Platinum Plan

- Highest monthly costs but the lowest out-of-pocket expenses. Best for those with high medical needs.

- Premium Tax Credit

- A discount that lowers your monthly health insurance payment if you qualify based on income.

- Individual Health Plans

- Health insurance policies purchased by individuals (rather than provided by employers) to cover medical expenses like doctor visits, hospital stays, and prescriptions.

- Health Insurance Marketplace (ACA/Obamacare)

- A government-run website where you can shop for and buy health insurance plans, often with financial assistance.

- Workplace Health Insurance

- A health plan offered by your employer, often with lower costs because your employer pays part of the premium.

2a.Compare Costs

Let’s be real: The premium—the amount you pay each month—is the first number everyone looks at when picking a health plan. But that number alone doesn’t tell you the full story. The real question is how much will this plan actually cost you over the course of a year?

To figure that out, you need to look beyond the premium and compare the four key costs that you’ve learned about already. Let’s review them again to help you choose the right health insurance plan:

1. Premium: Your Monthly Bill

This is the amount you pay every month to have health insurance, regardless of whether you use it. A low premium might seem like a great deal, but it often comes with higher costs when you need care.

2. Deductible: What You Pay Before Insurance Helps

The deductible is the amount you have to pay out of pocket before your insurance starts covering a portion of your medical expenses. A low-premium plan usually comes with a high deductible, meaning if you get sick or need care, you’ll have to cover more costs yourself before insurance kicks in.

3. Co-payments and Coinsurance: Your Share of Medical Costs

Once you’ve met your deductible, you still pay a portion of your medical bills. This comes in two forms:

- Co-payments (co-pays): A fixed amount for each doctor visit, prescription, or service (e.g., $30 for a doctor visit).

- Coinsurance: A percentage of the bill you pay (e.g., 20% of a hospital visit, while insurance covers 80%).

4. Out-of-Pocket Maximum: The Safety Net

This is the most you’ll have to pay for covered medical services in a year. Once you reach this limit, insurance will cover 100% of your costs for the rest of the year. If you have frequent medical needs, a plan with a lower out-of-pocket maximum can prevent you from spending thousands on medical bills.

-

EXAMPLE

Let’s say you have two health plan options:

|

Plan

|

Monthly Premium

|

Deductible

|

Co-pay for Doctor Visit

|

Out-of-Pocket Maximum

|

|

Plan A

|

$150

|

$5,000

|

$40

|

$7,500

|

|

Plan B

|

$350

|

$1,000

|

$25

|

$4,500

|

At first glance, Plan A seems cheaper because the monthly premium is lower. But let’s say you break your arm and need a hospital visit. Here’s what could happen:

- With Plan A, you must pay $5,000 out-of-pocket before your insurance starts covering costs. Plus, each doctor visit is $40. If the total amount you pay in medical expenses for the year, apart from your monthly premiums, reaches $7,500, you’re paying all of that yourself before insurance fully kicks in.

- With Plan B, you only need to pay $1,000 before insurance starts covering a portion of your bills. Your co-pays are lower, and you’ll never pay more than a total of $4,500 for the year.

If you rarely go to the doctor, Plan A might save you money. But if you have an unexpected illness, injury, or ongoing medical needs, Plan B could save you thousands even though the monthly cost is higher.

Before you pick a plan, think about how often you go to the doctor, whether you take medications, and if you can afford a high deductible in an emergency. A lower premium might look good up front, but if you end up paying thousands in out-of-pocket costs, it might not be the best choice in the long run.

In this lesson, you discovered how to assess your health insurance needs to choose a plan that suits you. You also got a crash course on how to compare health insurance categories and compare costs to select a plan.