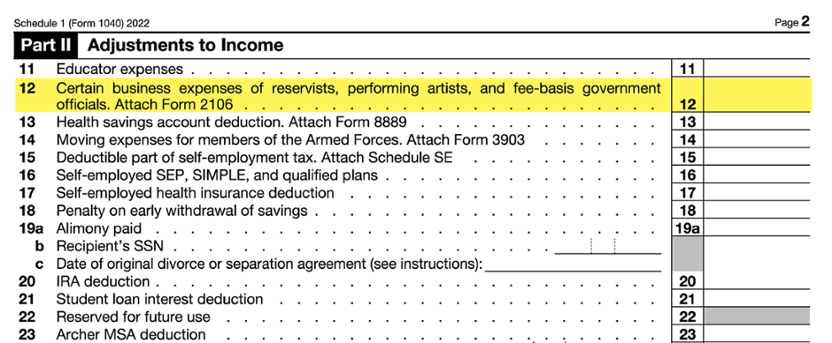

There are special rules for Armed Forces reservists, government officials who are paid on a fee basis, certain performing artists, and disabled employees with impairment-related work expenses. They will be introduced here for awareness. More information can be found in Publication 17, Your Federal Income Tax, beginning on page 99.

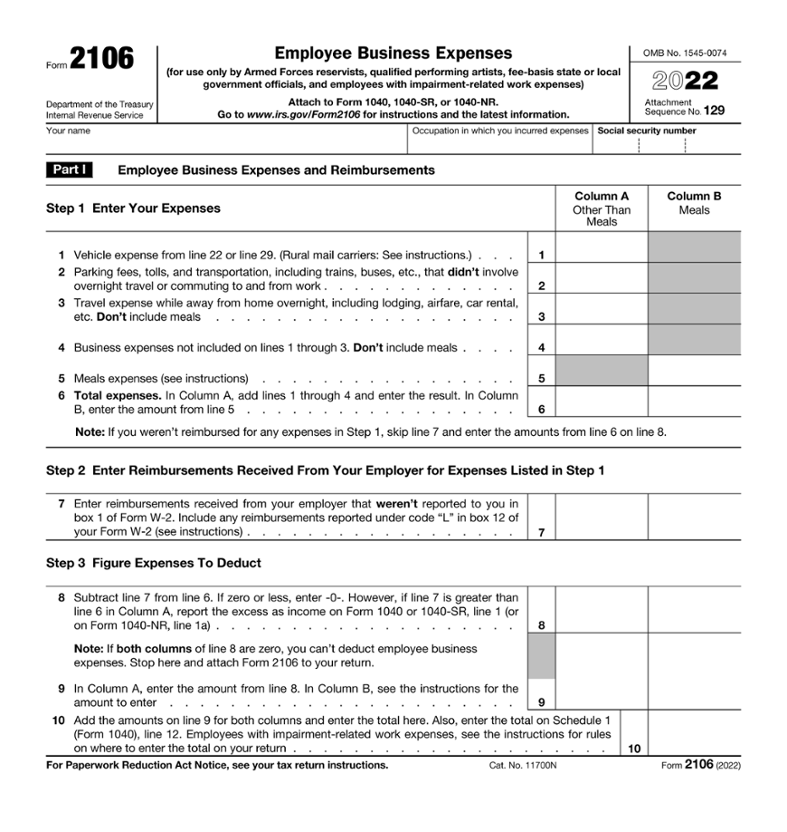

These taxpayers may be able to adjust their total income on Schedule 1 (Form 1040), line 12. If they qualify for the adjustment to income, they will first have to complete Form 2106, Employee Business Expenses.

Taxpayers who are a member of the Armed Forces, National Guard, or Reserve Corps and must travel more than 100 miles from their home for services related to the reserves may be able to deduct certain travel expenses.

Employees of state or local governments who are paid in whole or in part on a fee basis may be able to deduct their business expenses as an adjustment to income.

Certain performing artists may qualify to deduct some of their employee business expenses as an adjustment to income. There are specific requirements that must be met for the taxpayer to be able to deduct the expenses.

Such expenses would include payment related to special equipment, training, or anything else directly related to an individual’s ability to perform work with an impairment.

IN CONTEXT: Form 2106 Changes

Prior to 2018, taxpayers who had unreimbursed business expenses as an employee could potentially deduct the expenses on their income tax return as an itemized deduction. For employees, this was calculated on Form 2106.

The Tax Cuts and Jobs Act of 2017 eliminated the unreimbursed employee business expense deduction that was part of itemized deductions. Form 2106 is now only used by the four types of taxpayers mentioned above.

However, this change does not impact employer reimbursement plans. Employers can continue to use reimbursement plans to compensate employees for their expenses.

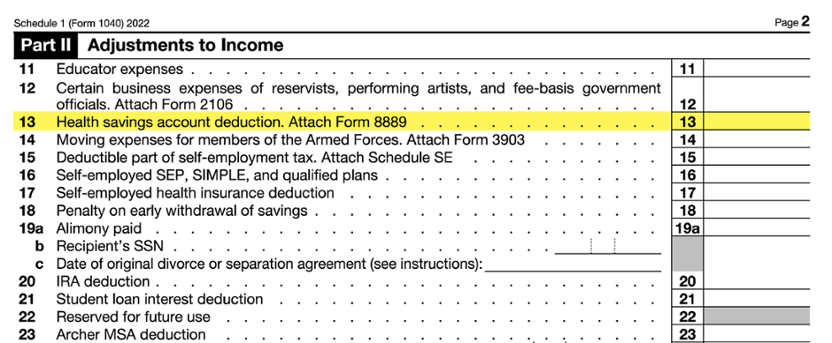

A health savings account (HSA) is a tax-advantaged medical savings account available to taxpayers who are enrolled in a high-deductible health plan (HDHP). These accounts allow taxpayers to use tax-free funds to pay for qualified medical expenses for themselves, their spouse, or dependents claimed on their return.

A taxpayer who made after-tax contributions to their HSA, not through their employer, may be entitled to deduct these contributions as an adjustment to income on Form 1040. Generally, HSA contributions made by an employer on the taxpayer’s behalf are excluded from taxable income and are not reported in box 1 of the taxpayer’s Form W-2. This amount, plus any amount contributed by the employee through their employer’s plan, is shown in box 12 with the code W.

To qualify for the HSA contribution deduction, the taxpayer must first qualify to make contributions to their HSA and not exceed their maximum annual HSA contribution limits, which are based on the HDHP the taxpayer is enrolled in, self or family. There are several other requirements that apply before the taxpayer is eligible to claim the HSA deduction on their return.

Health savings account contributions that qualify for the adjustment to income are entered on Schedule 1, line 13, and Form 8889, Health Savings Accounts (HSAs), must be attached to the return.

For more information on HSAs, see IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans.

IN CONTEXT: Flexible Spending Arrangement (FSA)

A flexible spending arrangement (FSA) is another type of medical savings account available through an employer. It is a salary reduction agreement. FSAs share many similarities to HSAs, but they are not reported on the tax return. When preparing a return for a taxpayer with a health savings account, be careful to verify that you have the right kind of account! (You can learn more about FSAs in Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans.)

The table below compares the differences between HSAs and FSAs.

HSA (Health Savings Account) FSA (Flexible Spending Arrangement) Funds belong to the taxpayer even after separation of service. Taxpayer loses the funds after separation of service. No mandatory time frame to use the funds. “Use it or lose it.” If funds are not used by the expiration date, they are lost to the employer.

IN CONTEXT: Archer MSA vs. HSA

An Archer MSA (medical savings account) is a medical savings account similar to a health savings account (HSA). Like an HSA, it is available to taxpayers enrolled in a high-deductible health plan. However, there are distinct rules governing contributions and eligibility. When distinguishing HSAs from flexible spending accounts (FSA) and Archer MSAs, if you are assisting a taxpayer who made contributions to some type of medical savings account, be sure that you understand which type of account it is so that you treat the contributions correctly on the taxpayer’s return.

A contribution to an Archer MSA is entered on Schedule 1, line 23.

Prior to 2018, taxpayers who moved within one year of starting a new job may have been eligible to deduct their moving expenses as an adjustment to income on Form 1040. The Tax Cuts and Jobs Act of 2017 (TCJA) eliminated the moving expense adjustment to income for all taxpayers, with the exception of active duty members of the Armed Forces who have a permanent change of station due to a military order.

The military taxpayer’s moving expenses are reported on Form 3903, Moving Expenses, first, and then are deducted on Schedule 1 (Form 1040), line 14.

A qualifying taxpayer is allowed to deduct reasonable moving expenses. Deductible moving expenses generally include actual costs for transportation of household goods, traveling, lodging (not meals), and temporary storage.

For more information on moving expenses, see the Instructions for Form 3903.