1. Calculating the Lifetime Learning Credit

The lifetime learning credit is available for up to $2,000 per tax return. The amount of the lifetime learning credit is the lesser of:

- 20% of the first $10,000 of qualified education expenses paid for all eligible students.

- 20% of the actual qualified education expenses paid for all eligible students if the total is under $10,000.

The lifetime learning credit is a nonrefundable credit.

-

EXAMPLE

John and Abigail Proctor have modified AGI of $75,000. Their dependent son, Joseph, is a college freshman at the beginning of the tax year. Joseph does not attend school on at least a half-time basis. The Proctors paid qualified education expenses totaling $6,000.

Their potential lifetime learning credit for 2022 is $1,200 [$6,000 × 20% = $1,200].

-

EXAMPLE

The facts are the same as in Example 1, except the qualified expenses are $12,000. In this case, the potential lifetime learning credit would be $2,000 [$10,000 × 20% = $2,000]. These are the maximum expenses for the credit ($10,000) multiplied by 20%.

Remember, the lifetime learning credit and the AOTC may not be claimed for the same student for the same year, but each credit may be claimed for different students for the same year.

-

If a student takes longer than four years to complete their undergraduate degree program, the AOTC will have been used up, but they will still qualify for the lifetime learning credit.

2. Step 1: Determine the Amount of Qualified Expenses

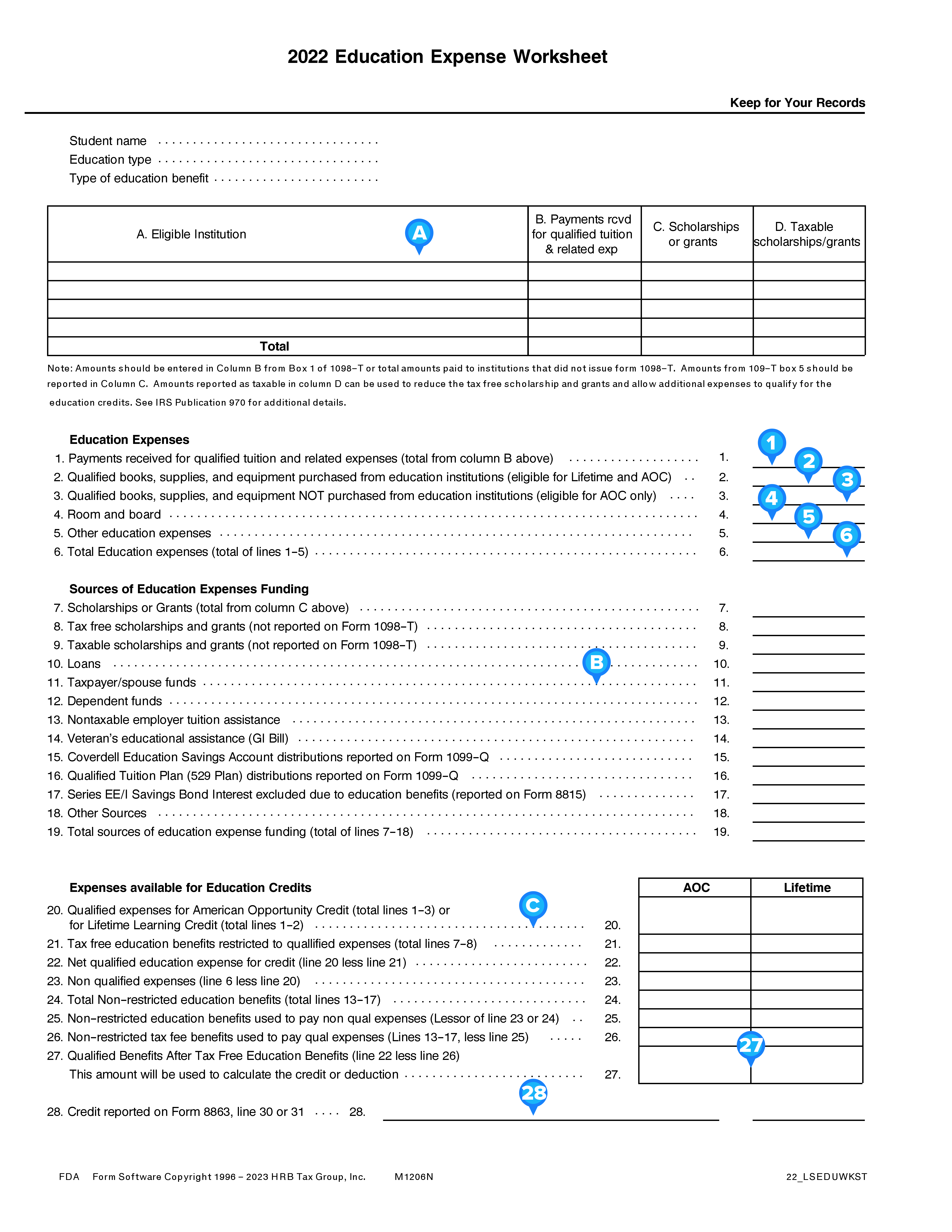

Once again, we can use the 2022 Education Expense Worksheet to help keep track of qualified and nonqualified expenses.

-

A. The top section lists the total payments received for qualified tuition and related expenses (column B), scholarships and grants (column C), and any taxable scholarships or grants (Column D).

-

Line 1. The total payments received from column B above is entered here.

-

Line 2. The cost of books, supplies, and equipment required and paid to the school for enrollment or attendance at the eligible educational institution is entered here. Do not confuse the part of the directions that say, “purchased from the education institutions.” This is referring to those items that are required as a condition of enrollment or attendance which typically are required to be paid directly to the institution. This is not referring to items purchased at the institution’s bookstore. The important distinction here is whether they were purchased as a condition of enrollment or attendance. These items are qualified expenses for both AOTC and the lifetime learning credit.

-

Line 3. The cost of books, supplies, and equipment NOT required for enrollment or attendance at the eligible educational institution is entered here. Do not confuse the part of the directions that say, “NOT purchased from education institutions.” This is not to say the books, supplies, or equipment purchased from the school bookstore are not qualified expenses. The amount entered on this line is necessary expenses that are not a condition of enrollment or attendance regardless of where they are purchased. These types of expenses are qualified expenses for the AOTC only. Expenses entered on this line are NOT eligible for the lifetime learning credit.

-

Line 4. This is the total amount paid for room and board. Room and board are not qualifying expenses for either education credit.

-

Line 5. Any education expenses that do not belong on lines 2, 3, or 4 are entered here. These are not qualified education expenses for either education credit.

-

Line 6. Total education expenses on lines 1 through 5.

-

B. This section records how all of the education expenses were paid. Lines 6 and 19 should be equal.

-

C. This section helps compare the two education credits. Each line provides instructions on what needs to be carried from prior entries on the worksheet. Line 20 specifically states to carry lines 1, 2, and 3 to the AOC column and carry lines 1 and 2 to the lifetime learning credit column.

-

Line 27. This is the total amount of qualified benefits. This amount is used to calculate the education credit on Form 8863.

-

Line 28. After comparing the two education credits, choose the most beneficial credit and enter it on the first line. The second line is the total qualified educational expenses for the lifetime learning credit, which is carried to Form 8863.

3. Step 2: Complete Form 8863, Part III

Form 8863, Part III, gathers all of the necessary information for the student and the educational institution. As you read through each of the questions, you’ll notice many of the requirements for AOTC are covered and the instructions direct where the qualified education expenses will be entered, either on line 27 for AOTC or line 31 for the lifetime learning credit.

Part III is really an aid in determining which credit the student qualifies for. If the qualifications are not met for the AOTC, the amount of lifetime learning credit qualified expenses is carried to Form 8863, line 31. This is then carried to Form 8863, Part II.

4. Step 3: Complete Form 8863, Part II, and the Credit Limit Worksheet

Part II is used to compute the amount of nonrefundable education credit(s). Form 8863, Part II, first applies the modified adjusted gross income limitation and computes the nonrefundable lifetime learning credit. The total lifetime learning credit qualified expenses (for all students) are entered on line 10. They are then limited to a total of $10,000 on line 11. This amount is multiplied by 20% for the tentative lifetime learning credit. Next, the modified adjusted gross income limitation is applied.

4a. Form 8863, Part II

4a.i. Lifetime Learning Credit MAGI

For the lifetime learning credit, the modified adjusted gross income (MAGI) equals AGI plus:

- Foreign earned income exclusion (Form 2555, Foreign Earned Income).

- Foreign housing exclusion (Form 2555).

- Foreign housing deduction (Form 2555).

- Income excluded by bona fide residents of American Samoa (Form 4563, Exclusion of Income for Bona Fide Residents of American Samoa).

- Income excluded by bona fide residents of Puerto Rico.

Note: The issues in the list above are advanced topics and are not covered in this course. If you have a taxpayer with any of these types of income, please do additional research. Information can be found in IRS Publication 970,

Tax Benefits for Education.

4a.ii. Income Limitation

Certain levels of MAGI reduce or eliminate the lifetime learning credit.

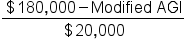

The credit is phased out for taxpayers with MAGI between $80,000 and $90,000 ($160,000 and $180,000 MFJ). The credit is not available to taxpayers with MAGI of $90,000 and above ($180,000 MFJ).

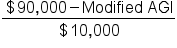

The credit for taxpayers filing a joint return is computed by multiplying the tentative credit by:

For all other filing statuses, multiply the tentative credit by:

This means there is no MAGI limitation for single, HOH, and QSS, if their MAGI is under $80,000. Their credit will be limited if their MAGI is between $80,000 and $90,000, and the credit will be unallowed if their MAGI is $90,000 or more.

For taxpayers filing MFJ, it means there is no MAGI limitation if their MAGI is under $160,000. Their credit will be limited if their MAGI is between $160,000 and $180,000, and the credit will be unallowed if their MAGI is $180,000 or more.

The MAGI limitation is computed on lines 13 through 18.

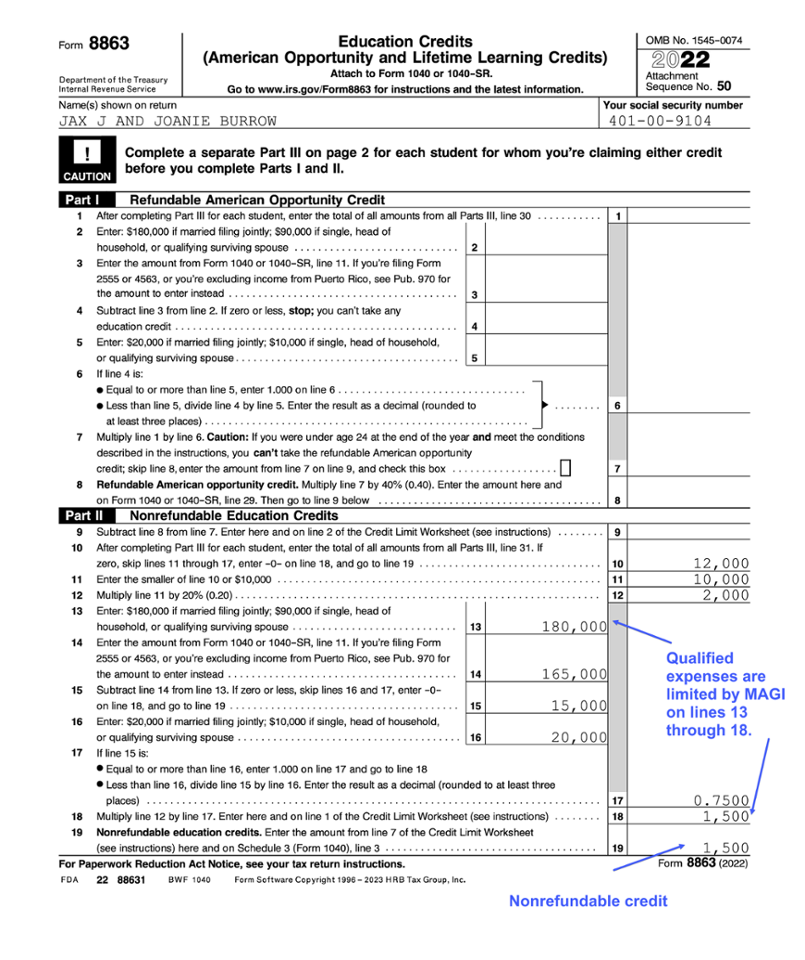

4b. Form 8863, Part II, and the Credit Limit Worksheet

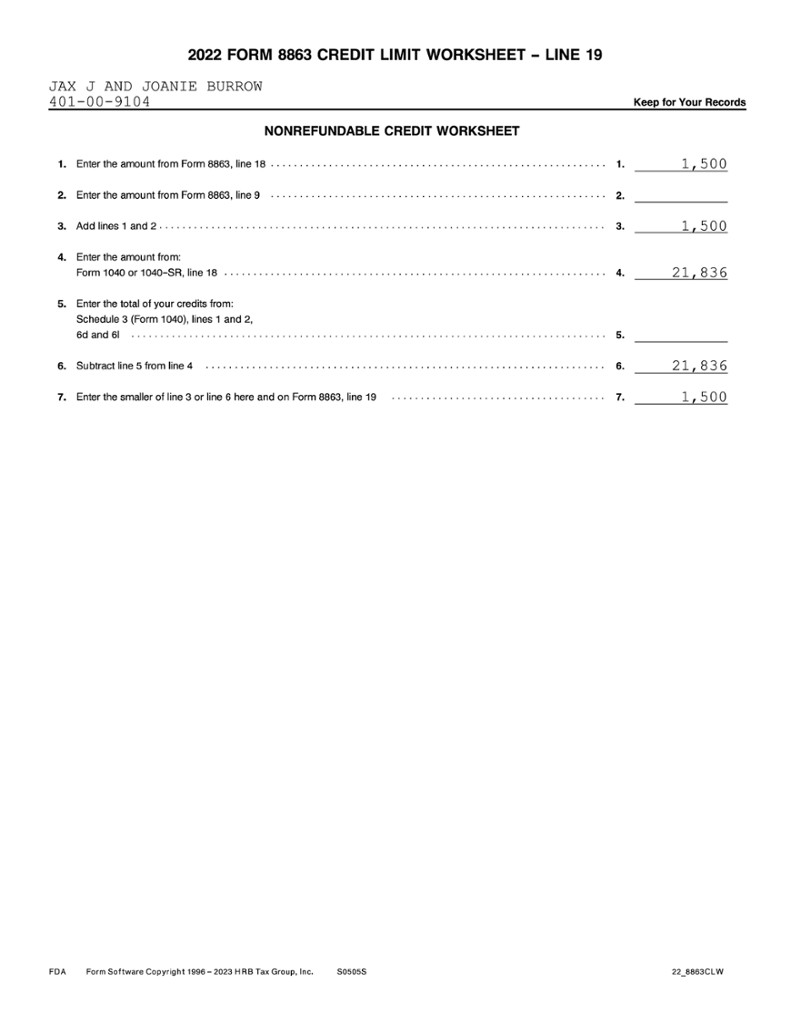

The line 18 amount of tentative lifetime learning credit is carried to the 2022 Form 8863 Credit Limit Worksheet – Line 19 next. Since the lifetime learning credit is nonrefundable, it is limited to the amount of tax on Form 1040, line 18. The worksheet adds all of the nonrefundable AOTC and lifetime learning credit amounts for the tax return on lines 1 and 2. The taxpayer’s tax from Form 1040, line 18, is entered, and then the amounts from certain other credits are subtracted first. These credits include the Foreign Tax Credit, Credit for Child and Dependent Care, and the Credit for the Elderly or the Disabled.

The nonrefundable portion of the education credits will be limited to the amount of tax remaining after the other credits are subtracted.

If there is more tax than the potential nonrefundable education credits, the entire amount is carried to Form 8863, line 19.

The amount on line 19 of Form 8863 is the total nonrefundable education credits and is carried to Schedule 3, line 3.

-

EXAMPLE

Jax and Joanie are married and will file a joint 2022 tax return. They have a tentative lifetime learning credit of $2,000 and MAGI of $165,000.

Their lifetime learning credit is reduced to $1,500 [$2,000 × ((180,000 – 165,000) ÷ 20,000) = $1,500].