Table of Contents |

Many personal financial decisions involve money received now or in the future and often a series of cash flows known as annuities, which we learned about in the prior lessons. If you were thinking that loans and investments are like annuities and involve either making or receiving payments with interest over time, you are correct! A loan involves regular payments that include an interest expense and the original loan amount, or principal.

To address some of the most common financial decisions, we need to ask a few questions to determine what we are trying to solve. If the answer is yes, then the correct formula is noted after the question:

Question 1: A single cash flow to be received or paid in the future?

Formula to use: Future value (FV)

Question 2: A single cash flow to be received or paid today?

Formula to use: Present value (PV)

Question 3: The value in the future of multiple equal cash flows received or paid at regular intervals?

Formula to use: Future value of an annuity (FVAN)

Question 4: The value today of multiple equal cash flows received or paid at regular intervals?

Formula to use: Present value of an annuity (PVAN)

Note: The PV or FV of multiple unequal cash flows received or paid at regular or irregular intervals must be calculated separately using the formulas in Questions 1 or 2 above.

If you are an adult who wishes to purchase a home, you will have questions about home loans, such as mortgages. For example, let’s say you find a home, and to make the purchase, you must take out a $150,000 mortgage, paying it back monthly. After checking mortgage interest rates online, you find the best option is a 30-year mortgage with a loan rate of 6%. You might be wondering what your monthly payment will be.

What you are solving for in this situation is the unknown monthly payment (PMT) that will be paid to the bank every month for 30 years, or 360 months (t). Since you will make regular cash flow payments on a loan of $150,000 (PV) that you receive today to purchase the home, you should use the PVAN formula.

Note: Since the payments are made monthly, the interest rate of 6% needs to be converted to monthly, and the number of periods needs to be in months when the PFIVA is calculated. Therefore, the monthly rate is 6%/12, or 1% (r), and the number of months is 12×30, or 360 months (t).

Now, we can substitute the loan amount of $150,000 as the present value of an annuity (PVAN) on the left-hand side of the equation. Also, using the PVIFA formula from the previous lesson, we calculate the interest factor to be 166.79. The formula now becomes:

$150,000 = PMT × (166.79)

To solve for the monthly PMT, we divide each side by 166.79.

That is, $899.33 = PMT, or the monthly mortgage payment on the loan. This monthly payment includes portions that go toward interest and principal repayment over time.

Now, look at the same mortgage loan with three different interest rates.

| Mortgage Amount | Interest rate (r) | Monthly Payment |

|---|---|---|

| $150,000 | 3% | $632.41 |

| $150,000 | 6% | $899.33 |

| $150,000 | 10% | $1,316.36 |

is 13.059.

is 13.059. × (

× ( )

)

For reference, the PVAN and FVAN formulas can be used to calculate:

What if you want to have $1,000,000 (the FV) in the bank when you retire? If your bank is currently paying a 3% interest rate (r) compounded annually, and you feel that you can save $10,000 per year (PMT) to put into a retirement account, what will you have in your account at age 65 if you start saving at age 25?

Use the FVAN formula to answer this question:

Using the FVIFA formula from the previous lesson, we calculate the interest factor to be 75.401. The formula now becomes:

FVAN = $10,000 × (75.401)

FVAN = $754,010

At the end of 40 years, you will have $754,010. In this case, you will fall short of your goal. However, if you can earn 5%, you can exceed your goal.

Using the FVIFA formula from the previous lesson, we find the interest factor to be 120.800. The formula now becomes:

FVAN = $10,000 × (120.800)

FVAN = $1,208,000

is 40.995.

is 40.995.

Help With the Calculations

There are many personal finance software packages and free resources on the Internet. You can find a mortgage calculator, a loan calculator, or a retirement planner to answer questions such as “How much do I have to save every year for retirement?” or “What will my monthly loan payment be?” Most importantly, be sure to use reputable sites and be careful not to give out any personal information online unless you have officially verified the source.

Adelina

A mother wanting to finish her degree

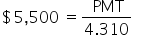

Now, let’s look at Adelina, who has saved $1,000 and wants to save more for her college tuition in the short term and the down payment on a home in the long term. If college tuition costs $130 per credit hour and Adelina needs 124 credits for her degree but has only completed 74 credits, she will need to complete 50 more credits. The estimated cost of finishing her degree is $130 × 50 credits or $6,500, minus the $1,000 she’s already saved. Since Adelina’s youngest son is only 2 years old, she plans to wait until her son is 6 before returning to college. Adelina is earning 5% on her savings account, so using our FVAN formula, we can solve for the PMT to see how much Adelina needs to save each year to achieve her goal:

Using the FVIFA formula from the previous lesson, we calculate the interest factor to be 4.310. The formula now becomes:

$5,500 = PMT × (4.310)

$1,276.10 = PMT

Thus, Adelina will need to save $1,276.10 per year to meet her goal.

is 23.657.

is 23.657.

You now see the benefit of using the PVAN and FVAN formulas to determine monthly payments for college, a mortgage, or other expenditures. However, this information is only helpful if you understand how these cash flows relate to your budget.

EXAMPLE

Suppose you calculate a monthly mortgage payment of $899.50 on a loan for $150,000, but you only have a budget surplus of $500. Using the mortgage loan payment calculated, you should go back to your budget to see if your goal is realistic. To become a homeowner, you may need to eliminate unnecessary expenses to meet the new mortgage payment.However, don’t forget that owning a home is more expensive than just the mortgage payment. Creating a projected budget based on what you would like to do, such as buying a home, and adding in the extra expenses of real estate taxes, utilities, and mortgage are extremely beneficial in seeing the full impact of home ownership on your budget. Creating a projected or estimated new budget is a smart way to see if you can truly carry the added expenses of your goal beforehand. Projected financial statements, called pro forma statements, are used in financial planning to see the expected changes in your income, expenses, or wealth depending on your potential choices. Pro forma statements allow you to get a glimpse into your projected income statement and balance sheet for any choice you consider. When making personal financial decisions, it is vital to think about their consequences on your financial statements and wealth accumulation to avoid negative consequences.

This is when financial planning becomes even more critical. As you discovered, creating a budget to see where your money goes and reviewing each expense to determine if they are necessary is the first step. Next, finding a reasonable way to begin saving is the second step toward feeling like you can make changes and progress toward financial goals.

Establishing a small and realistic short-term goal, such as setting aside $10 a week, will help you see your progress and money grow, which gives you a confidence boost. Here are a few suggestions to get started toward achieving your short-term goals that can help you move on to bigger, long-term goals later:

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.