In this lesson, you will learn how to create an investment portfolio. Specifically, this lesson will cover the following:

1. What Is an Investment Portfolio?

An investment portfolio is simply a collection of financial assets that you own. Think of it like a toolbox filled with different tools, each serving a specific purpose. Instead of hammers and screwdrivers, your portfolio contains investments like stocks, bonds, mutual funds, and real estate. Each one plays a role in helping you build and grow your wealth over time.

Some investments are steady and reliable, like a basic screwdriver—always useful and low risk. These might include bonds or index funds, which grow gradually and provide stability.

Other investments have more risk but offer the potential for higher rewards, like a power drill that helps you complete big projects quickly. Stocks, for example, can grow significantly over time but also experience ups and downs.

A well-balanced portfolio is like a well-stocked toolbox. It includes a mix of investments that work together to help you build wealth while managing risk.

The key is to choose the right combination of investments based on your financial goals, whether that’s saving for retirement, buying a home, or simply growing your money for the future.

Now, let’s take a closer look at the different types of investments you can include in your portfolio.

-

- Investment Portfolio

- A collection of assets—like stocks, bonds, real estate, and crypto—designed to help grow wealth over time.

1a. Investment Types

By now, you’re familiar with the different types of investments you can include in your portfolio from previous lessons. Think of this as a quick check-in to reinforce what you’ve already learned. Each investment plays a unique role in helping you build wealth, manage risk, and reach your financial goals.

- Stocks: Owning a piece of a company. Stocks can offer high growth potential, but they also come with ups and downs. Over time, they have historically provided strong returns.

- Mutual funds and ETFs: A collection of investments bundled together. These make it easier to diversify since they spread your money across multiple stocks or bonds, reducing risk.

- Bonds: Essentially, a loan you give to a company or government in exchange for interest payments. Bonds tend to be more stable and provide steady income.

- Real estate: Investing in property, whether for rental income or long-term appreciation. Real estate can provide cash flow and act as a hedge against inflation.

- Crypto: Digital assets like Bitcoin and Ethereum. Crypto is highly volatile but offers the potential for high returns and innovation in the financial world.

A well-balanced portfolio includes a mix of these investments based on your goals, risk tolerance, and time horizon.

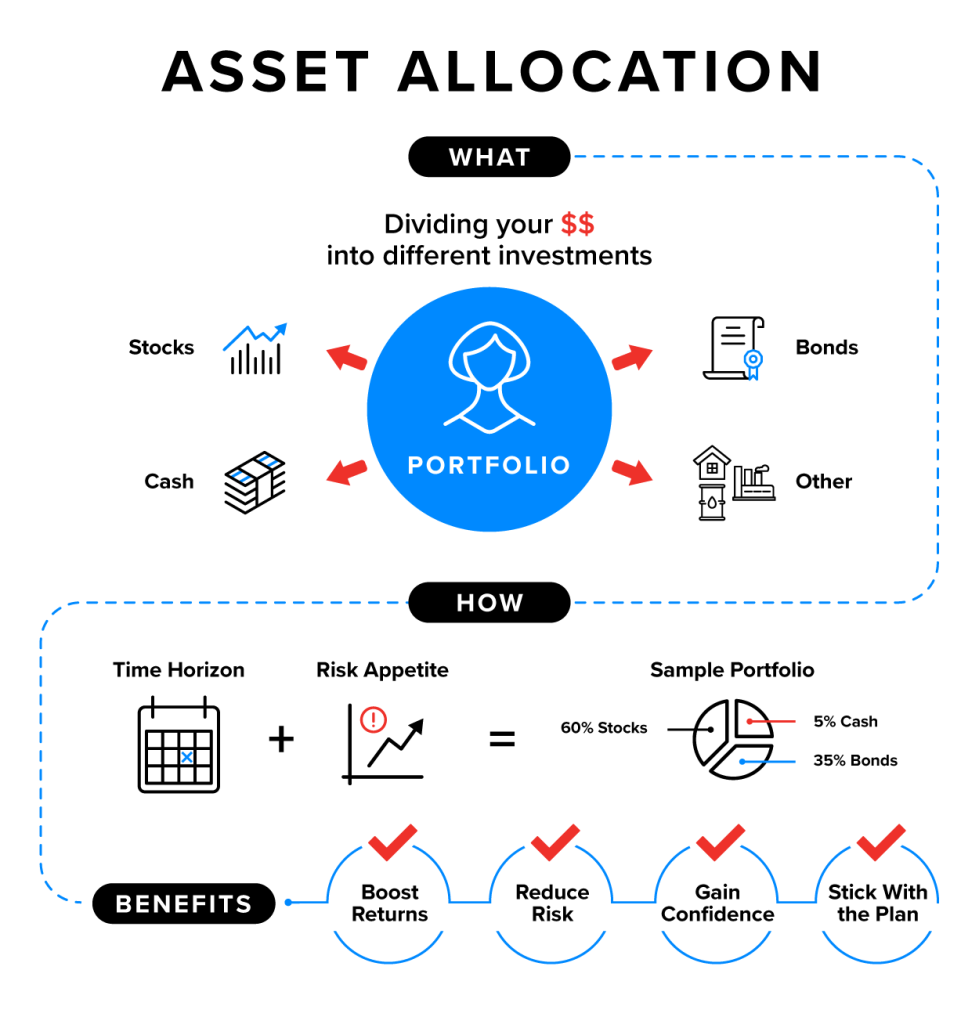

1b. Asset Allocation

Now that you know the different types of investments, the next step is asset allocation—deciding how much of your money should go into each type of investment. A well-balanced portfolio spreads risk across different assets to help you grow wealth while managing ups and downs in the market.

Asset allocation is the process of dividing your investment money among different asset categories like stocks, bonds, real estate, and crypto. The goal is to find the right mix based on the following:

- Your financial goals: Are you saving for retirement, a home, or general wealth building?

- Your risk tolerance: Can you handle market ups and downs, or do you prefer steady returns?

- Your time horizon: How long will it be until you need the money? A longer timeline allows for more risk.

These are the three main types of asset allocation strategies:

-

Conservative portfolio (low risk, steady growth)

- Best for: People close to retirement or those who want low risk

- Allocation example: 20% stocks, 60% bonds, 15% real estate, and 5% cash

- Why? Less risk, steady returns, and more stability in market downturns

-

Moderate portfolio (balanced growth and stability)

- Best for: Investors with 10+ years until retirement who want a mix of safety and growth

- Allocation example: 50% stocks, 30% bonds, 15% real estate, and 5% crypto

- Why? Balances risk and reward while keeping some protection

-

Aggressive portfolio (higher risk, high growth potential)

- Best for: Younger investors with long-time horizons who can handle market swings

- Allocation example: 80% stocks, 10% bonds, 5% real estate, and 5% crypto

- Why? Maximizes long-term returns, though with more volatility

-

When you’re younger, you have more time to recover from market dips, which means you can afford to take more risk for higher potential returns. A more aggressive portfolio—one with a higher percentage of stocks—can grow significantly over time. As you get closer to your financial goals, you can gradually shift to safer investments like bonds and real estate to protect your wealth.

Follow these steps to decide how to allocate your investments:

- Assess Your Risk Tolerance:

- Can you handle big market swings? If yes, you might lean toward more stocks.

- Prefer steady, predictable returns? Bonds and real estate may be better.

- Set Your Investment Goals:

- Short-term goals (0–5 years) → Lower risk (more bonds and cash)

- Mid-term goals (5–15 years) → Balanced approach (stocks, bonds, and real estate)

- Long-term goals (15+ years) → More aggressive (more stocks and some real estate)

- Adjust Over Time:

- Your asset allocation isn’t set in stone. As your life changes, your investments should too.

- As you get older or closer to a financial goal, you may shift toward more stable investments.

-

EXAMPLE

Meet Malik. He is 40 years old, works in tech, and wants to retire in 20 years. He’s comfortable taking some risk but doesn’t want to be too aggressive. His goal is to grow his wealth steadily while protecting himself from major market downturns.

Malik decides to divide his $20,000 investment into different assets based on his risk level:

- 60% in stocks ($12,000): He invests in an S&P 500 ETF and some individual stocks for long-term growth.

- 25% in bonds ($5,000): Bonds help stabilize his portfolio and provide steady returns.

- 10% in real estate ($2,000): He invests in a REIT to gain exposure to real estate markets.

- 5% in crypto ($1,000): He invests a small amount in Bitcoin and Ethereum for potential future growth.

By spreading his investments across different asset types, Malik is balancing growth and stability. If the stock market drops, his bonds and real estate may help cushion the loss. If the market does well, his stocks and crypto could provide strong returns.

This is how asset allocation works—it’s about creating the right balance to match your goals, risk level, and timeline.

Now that you’ve got the basics of asset allocation down, let’s bring it to life with a real example. Imagine you’re helping someone decide where to put their money to grow their wealth. In the next section, you’ll apply what you’ve learned to build an investment portfolio based on their goals, risk tolerance, and timeline. Think of it as crafting a game plan for their financial future.

-

- Asset Allocation

- A collection of assets—like stocks, bonds, real estate, and crypto—designed to help grow wealth over time.

- Conservative Portfolio

- A low-risk investment mix focused on stability, with more bonds and cash than stocks.

- Moderate (Balanced) Portfolio

- A mix of stocks and bonds that balances growth and stability for steady long-term returns.

- Aggressive Portfolio

- A high-risk, high-reward strategy with mostly stocks and little to no bonds, aiming for maximum growth.

2. Investment Portfolio Case Study

Now that you’ve learned about what’s in an investment portfolio, let’s put your skills to use for Jasmine.

Jasmine is 35 years old, a single mom, and a marketing manager, earning $85,000 per year. She has learned about different types of investments and is now ready to apply that knowledge to build her portfolio. Jasmine can invest $10,000 per year and needs a strategy that aligns with her financial goals.

Jasmine’s Goals and Risk Tolerance

- Long-term goal: Grow wealth over the next 25 years to retire comfortably and help support her son’s future.

- Risk level: Moderate—she is willing to take on some risk for growth but wants stability to protect her investments.

- Diversification strategy: This will be a mix of stocks, bonds, real estate, and crypto to balance risk and return.

Your Task: Help Jasmine Build Her Portfolio

Using what you’ve learned, decide how Jasmine should invest her $10,000 per year by selecting the right mix of assets. Consider the following:

- How much should she allocate to stocks, bonds, real estate, and crypto?

- How does each investment choice support her goal of long-term growth with moderate risk?

- What percentage of her portfolio should go toward stable versus higher-risk investments?

- Why does each choice make sense for her situation?

Portfolio Allocation Options

Jasmine has four main investment options:

- Stocks (ETFs, S&P 500, or individual stocks): Higher risk but strong long-term growth potential

- Bonds (government or corporate bonds): Lower risk, with stability and income

- Real estate (REITs) – Moderate risk and potential for growth and passive income

- Crypto (Bitcoin, Ethereum, or other coins): High risk but potential for high long-term returns

-

Activity: Design Jasmine’s Portfolio

Question 1: Select an allocation: conservative, moderate/balanced, or aggressive.

- Answer 1: Since Jasmine has a moderate risk tolerance and a long-term investment goal (25 years), a moderate/balanced portfolio is ideal.

- Recommended allocation:

- 50% stocks ($5,000): Long-term growth driver

- 30% bonds ($3,000): Stability and lower risk

- 15% real estate ($1,500): Passive income and diversification

- 5% crypto ($500): High-risk, high-reward potential

Question 2: Consider risks and adjustments—What would you change if she had a lower risk tolerance? What if she had a shorter time frame?

- Answer 2: If Jasmine had a lower risk tolerance (more cautious investor), a suggested modification could be:

- Reduce stocks to 40% and crypto to 2% (less volatility).

- Increase bonds to 40% for more stability.

- Keep real estate at 15% since it’s a moderate-risk investment.

If Jasmine had a shorter time frame (needed the money in 10 years instead of 25), a suggested modification could be:

- Reduce stocks to 40% (less time to recover from market dips).

- Increase bonds to 40% for short-term stability.

- Reduce crypto to 2% or eliminate it entirely (too volatile for a short-term goal).

- Keep real estate at 15%, as it can still provide solid returns in 10 years.

Jasmine’s 50-30-15-5 portfolio is a great fit for her moderate risk tolerance and long-term financial goal. If her situation changes, she can adjust her asset allocation to better match her risk level and timeline.

Now, it’s your turn!

Carlos is 38 years old and married with two kids, and he works as a teacher, earning $70,000 per year. He has been contributing to his workplace retirement plan but wants to take a more active role in investing to grow his wealth faster and potentially retire early.

Carlos has $6,000 per year available to invest and is willing to take on more risk for higher potential returns.

Carlos’s Goals and Risk Tolerance

- Long-term goal: Build as much wealth as possible over the next 20 years, aiming for early retirement and financial freedom.

- Risk level: High—he understands the ups and downs of the market and is comfortable taking risks for higher growth.

- Diversification strategy: This will be a portfolio heavily weighted in stocks and crypto, with a smaller percentage in real estate and bonds for some diversification.

Your Task: Help Carlos Build His Portfolio

Carlos is comfortable with high-risk, high-reward investments, so his portfolio will focus on growth over stability. Using what you’ve learned, decide how he should allocate his $6,000 per year to maximize returns.

Consider the following questions:

- How much should he allocate to stocks, bonds, real estate, and crypto?

- How does each investment choice align with an aggressive strategy?

- What percentage of his portfolio should be in high-risk versus moderate-risk investments?

- What adjustments would you make if Carlos became more risk averse later in life?

-

Activity: Design Carlos’s Portfolio

Answer the following questions, and select the “+” button to see if you are correct.

Select an allocation for Carlos.An allocation of 70% stocks, 15% crypto, 10% real estate, and 5% bonds makes sense for Carlos because he has a long investment horizon (20 years) and is comfortable taking on higher risk for greater potential returns.

- 70% stocks ($4,200 per year): The main driver of high returns

- 15% crypto ($900 per year): A high-risk, high-reward addition

- 10% real estate ($600 per year): Diversifies his investments

- 5% bonds ($300 per year): Provides a small cushion in downturns

Consider risks and adjustments—If Carlos decides he wants more stability in 10 years, how should he rebalance his portfolio?If Carlos decides he wants more stability in 10 years, he should rebalance to a more moderate allocation:

New Allocation (10 Years Later, Age 48):

- 50% stocks: Reduce exposure to minimize risk as retirement approaches.

- 25% bonds: Increase bonds for more stability and income.

- 15% real estate: Keep real estate for continued passive income.

- 5% crypto: Reduce crypto since it’s highly volatile.

- 5% cash/money market funds: Hold some cash for short-term needs.

Why This Adjustment Works:

- More bonds and cash = less volatility and a smoother transition toward retirement

- Less crypto = lower risk as he moves closer to needing his money

- Still maintains stock exposure (50%) for continued growth

By making these gradual shifts, Carlos can secure his wealth while still allowing for growth as he nears retirement.

Great job applying your knowledge to build an investment portfolio! Just like real investing, there’s no one-size-fits-all approach—what matters most is aligning investments with goals, risk tolerance, and time horizon. As you continue learning, remember that portfolios can be adjusted over time, and the key to long-term success is staying informed and making thoughtful decisions.

In this lesson, you developed an understanding of an investment portfolio, reviewed investment types, and learned about asset allocation. You rounded out the lesson with an investment portfolio case study to apply your learning.