In this lesson, you will learn about the importance of naming beneficiaries and asset titling. Specifically, this lesson will cover the following:

1. Understanding Beneficiaries

-

When we think about managing money, we often focus on what we need during our lifetime—saving, investing, budgeting, and paying off debt. But an important part of financial planning is considering what happens to our money and assets after we’re gone. Beneficiaries are the people or entities who receive assets upon our passing. By clearly naming beneficiaries, we ensure that our loved ones receive the money and property we want them to have without unnecessary legal complications or financial stress.

Why Are Beneficiaries Important?

Imagine you’ve worked hard for decades, saved diligently, and built a solid financial foundation. Now imagine all that effort getting tangled up in legal red tape, taxes, or even going to the wrong person simply because you didn’t take a few minutes to name a beneficiary. That’s the reality for many people who overlook this crucial step.

Types of Beneficiaries

-

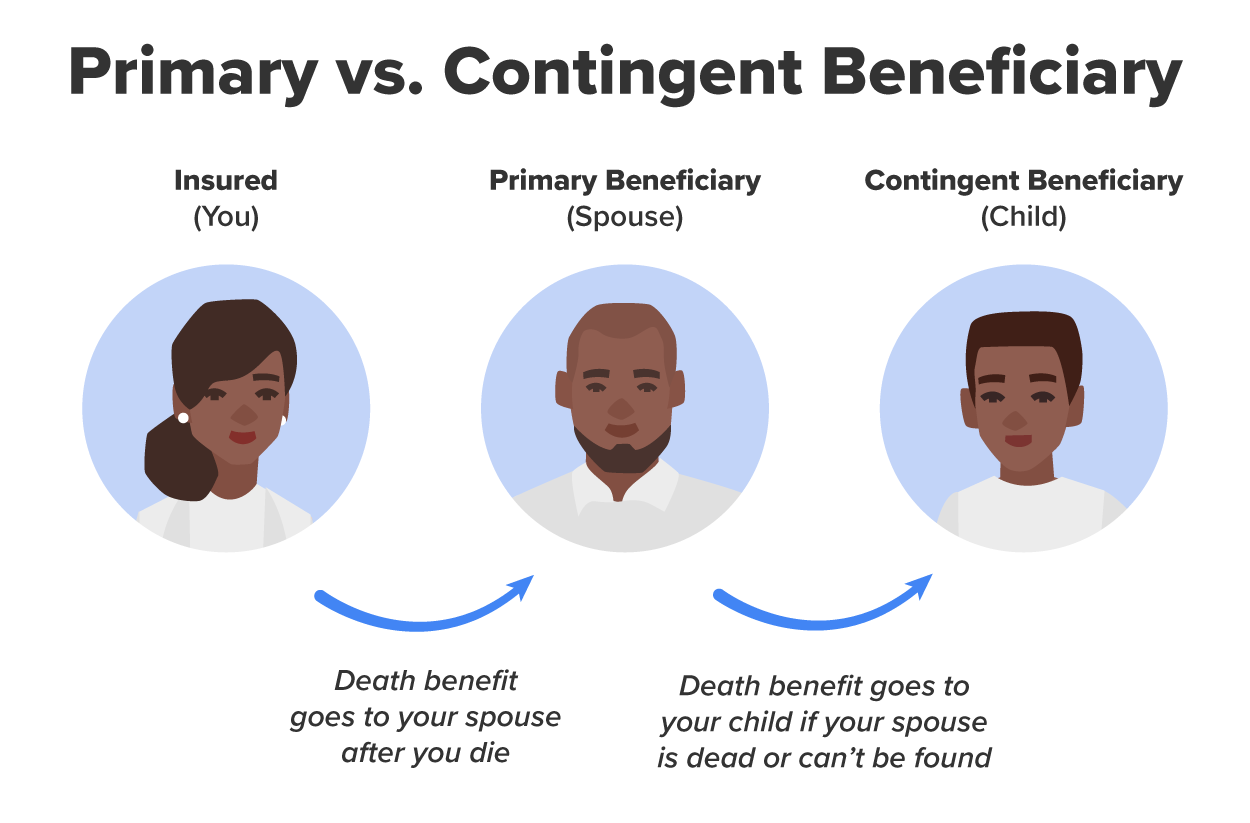

Primary Beneficiary: This is the first person (or entity) in line to receive the asset.

-

Contingent Beneficiary: This is the backup, the person who receives the asset if the primary beneficiary is no longer alive.

-

Revocable Beneficiary: This beneficiary can be changed at any time by the owner.

-

Irrevocable Beneficiary: This beneficiary cannot be removed without their consent once they are named.

-

EXAMPLE

Tiana is 35 years old, a single mom to her 7-year-old son, Malik. She has a solid career, a 401(k), a life insurance policy, and a growing savings account. She wants to make sure that if anything happens to her, Malik is financially secure and protected.

How Tiana Sets Up Her Beneficiaries

- Life Insurance Policy

- Primary Beneficiary: Since Malik is a minor, Tiana does NOT name him directly. Instead, she sets up a trust and names the trust as the beneficiary. The trust will hold the life insurance payout and distribute funds according to the instructions she sets (e.g., covering Malik’s education, housing, and other expenses).

- Contingent Beneficiary: Tiana names her younger sister, Jade, as the contingent beneficiary in case the trust cannot accept the funds for any reason.

- 401(k) Retirement Account

- Primary Beneficiary: Tiana again names the trust as the primary beneficiary to ensure the money is managed correctly for Malik’s future.

- Contingent Beneficiary: She names her sister Jade, knowing she would use the money responsibly for Malik if needed.

- Savings Account (Payable on Death, POD Designation)

- Primary Beneficiary: The trust is listed to prevent Malik from receiving a lump sum while underage.

- Backup Plan: If the trust is not in place at the time of her passing, the funds go to Jade to manage for Malik.

- What Tiana Avoids

- Naming Malik directly as a beneficiary—since he’s under 18, the court would appoint a guardian to manage the money, creating delays and legal fees.

- Forgetting to update her beneficiaries—she makes a note to review them every few years, especially if her family structure changes.

Why This Works for Tiana

- Malik’s financial future is secure and protected in a structured way.

- A trusted family member (Jade) is in place as a backup.

- She avoids legal headaches and probate delays by setting up a trust.

By planning ahead, Tiana ensures that her son is taken care of no matter what happens.

Beneficiaries aren’t just for life insurance. Many types of financial accounts allow (or require) you to name beneficiaries:

- Retirement accounts (401(k), IRA, and pensions)

- Life insurance policies

- Bank accounts with “Payable on Death” (POD) designations

- Investment accounts with “Transfer on Death” (TOD) designations

Not naming a beneficiary can cause assets to go through probate—a legal process that can be expensive and time consuming. If you want to protect your loved ones, naming a beneficiary is one of the easiest and most effective steps you can take.

-

When naming beneficiaries, be as clear as possible. Use full legal names and avoid vague terms like “my children” if you have stepchildren or specific distribution plans. Also, avoid naming minor children directly—consider a trust or guardian to manage funds until they are of legal age.

While naming beneficiaries is a key step in ensuring that your assets pass seamlessly to the right people, it is only part of the equation. How your assets are titled also plays a crucial role in what happens to them after you’re gone. Even if you name a beneficiary on a retirement account or life insurance policy, other assets—such as real estate, bank accounts, and investment accounts—may still have to go through probate depending on how they are owned.

In the next section, we’ll explore asset titling, how different ownership structures impact inheritance, and strategies to make sure your wealth transitions smoothly to your loved ones.

-

- Primary Beneficiary

- The first person or entity to receive an asset upon the owner’s death.

- Contingent Beneficiary

- The backup beneficiary who receives the asset if the primary beneficiary is unavailable.

- Revocable Beneficiary

- A beneficiary that can be changed by the owner at any time.

- Irrevocable Beneficiary

- A beneficiary that cannot be changed without their consent.

2. Asset Titling

Asset titling refers to the way an asset is legally owned and how that ownership determines what happens to it after the owner passes away. Even if you have a will, the way your assets are titled can override your instructions and directly impact whether your loved ones receive what you intended.

-

EXAMPLE

If you own a house jointly with your spouse, they may inherit it automatically without the need for probate. However, if you own the same property as a sole owner, it may need to go through the legal system before your heirs can claim it. Understanding the different ways assets can be titled will help you plan for a smooth and efficient transfer of wealth.

Common Types of Asset Titling

1. Sole Ownership

- a. One person owns the asset entirely.

- b. Upon death, the asset must go through probate unless a beneficiary is named.

2.

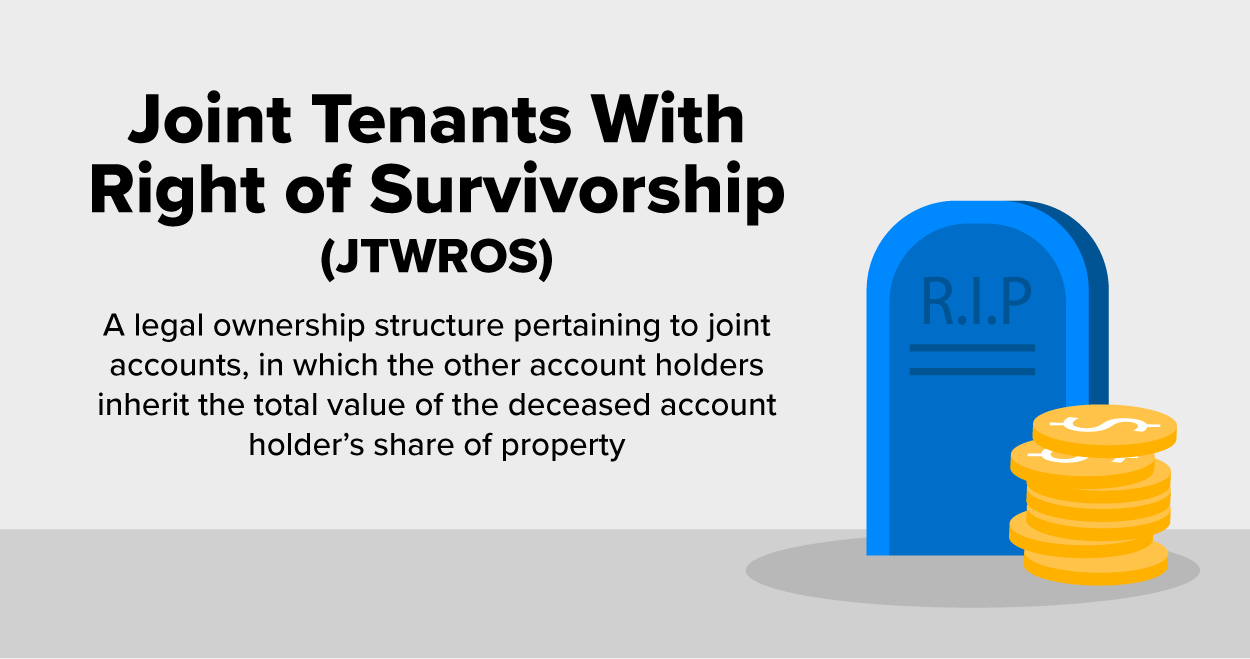

Joint Tenancy With Right of Survivorship (JTWROS)

- a. Two or more people own the asset together.

- b. When one owner dies, their share automatically passes to the surviving owner(s) without probate.

3. Tenancy in Common

- a. Two or more people own a share of the asset.

- b. Each owner’s share is passed down according to their will, rather than automatically going to the co-owner(s).

4. Transfer on Death (TOD) or Payable on Death (POD)

- a. These designations allow the asset to transfer directly to a named beneficiary upon the owner’s death.

- b. They bypass probate and ensure a smooth transition.

5. Trust Ownership

- a. Assets are legally held in a trust, which is managed by a trustee.

- b. The trustee distributes assets to beneficiaries based on instructions set in the trust, avoiding probate and providing additional legal protections.

IN CONTEXT

DeAndre (38) and Maya (36) are an engaged couple living in Atlanta. They have a 4-year-old daughter, Amara, and own a home, a joint checking account, and individual retirement accounts. DeAndre also has a life insurance policy through his job.

One night, while watching a financial advice video on YouTube, they hear about asset titling and how it affects who gets what when someone passes away. They realize they’ve never really thought about it.

The Problem: How Their Assets Are Titled Could Cause Issues

1. Their Home: Titled as “Tenants in Common” Instead of “Joint Tenants With Rights of Survivorship”

- When they bought their house, the default titling on their deed was “Tenants in Common” (TIC) instead of “Joint Tenants With Rights of Survivorship” (JTWROS).

- This means if something happens to DeAndre, his half of the house won’t automatically go to Maya—instead, it will pass according to his will or state laws.

- If DeAndre doesn’t have a will, the court will decide, potentially splitting ownership between Maya and their daughter Amara, which can complicate things.

Fix: They update their home’s deed to JTWROS, so if one of them passes, the other automatically will get full ownership without court involvement.

2. DeAndre’s Life Insurance: No Updated Beneficiary

- Years ago, DeAndre listed his mom as his life insurance beneficiary before he and Maya got serious.

- If he passes away, his mom—not Maya—will get the money, even though DeAndre now wants it to support Maya and Amara.

Fix: He updates his beneficiary to Maya (or a trust for Amara) to reflect his current wishes.

3. Maya’s Retirement Account: No Contingent Beneficiary

- Maya named DeAndre as her primary beneficiary on her 401(k) but never added a contingent beneficiary (backup).

- If something happens to both of them, the account will have to go through probate court, delaying access to funds for Amara.

Fix: She adds a trust or a guardian-managed account for Amara as a contingent beneficiary, so the money goes directly to her without legal hassles.

4. Their Joint Bank Account: Lacks POD Designation

- Their checking and savings accounts are joint, meaning if one dies, the other will still have access.

- But if they both pass in an accident, their daughter Amara won’t automatically get the money—it will go to probate court.

Fix: They add a POD designation to a trust for Amara, so the bank releases the money directly if something happens.

The Lesson Here: Title Your Assets Correctly!

DeAndre and Maya realized that asset titling isn’t just paperwork—it’s a critical step in protecting their family’s financial future. By making a few simple changes, they:

- Prevented court delays and legal fees

- Ensured their home, money, and insurance benefits went where they intended

- Made things easier for their daughter if the unexpected happens

If assets are not titled correctly, even a well-written will might not be enough to avoid legal challenges. Here’s why asset titling is crucial:

- Ensures a smooth transfer of assets to loved ones

- Avoids the probate process, which can be expensive and time consuming

- Reduces family disputes and confusion over who inherits what

Four Common Asset Titling Mistakes to Avoid

- Not Updating Titles After Major Life Events

- If you get married, divorced, or remarried, failing to update your asset titles could mean your ex-spouse inherits your home or financial accounts.

- Owning Property as Tenants in Common Without a Clear Plan

- If you own a home with a business partner or relative as tenants in common, your share might go to an unintended heir instead of your preferred beneficiary.

- Leaving Real Estate in Sole Ownership Without a Plan

- If you’re the sole owner of a home, your heirs may face probate delays and expenses. A simple solution could be adding a TOD deed.

- Not Using a Trust When Needed

- If you have minor children or want to control how and when beneficiaries receive assets, a trust can provide clear guidelines and protections.

By taking the time to title your assets correctly, you provide your loved ones with a clear path forward, reducing stress and ensuring they receive their inheritance as intended.

-

- Asset Titling

- The way ownership of an asset is legally recorded.

- Sole Ownership

- One person owns the asset entirely.

- Joint Tenancy With Right of Survivorship (JTWROS)

- Two or more owners; the asset automatically transfers to the surviving owner(s) when one dies.

- Tenancy in Common

- Two or more owners; each owner’s share passes to their heirs, not the co-owner(s).

- Transfer on Death (TOD)

- A designation allowing an asset to pass directly to a named beneficiary upon the owner’s death.

- Payable on Death (POD)

- A designation allowing a bank account to transfer directly to a named beneficiary upon the owner’s death.

In this lesson, you discovered the importance of beneficiaries and the different ways to title assets for proper distribution upon death.