Table of Contents |

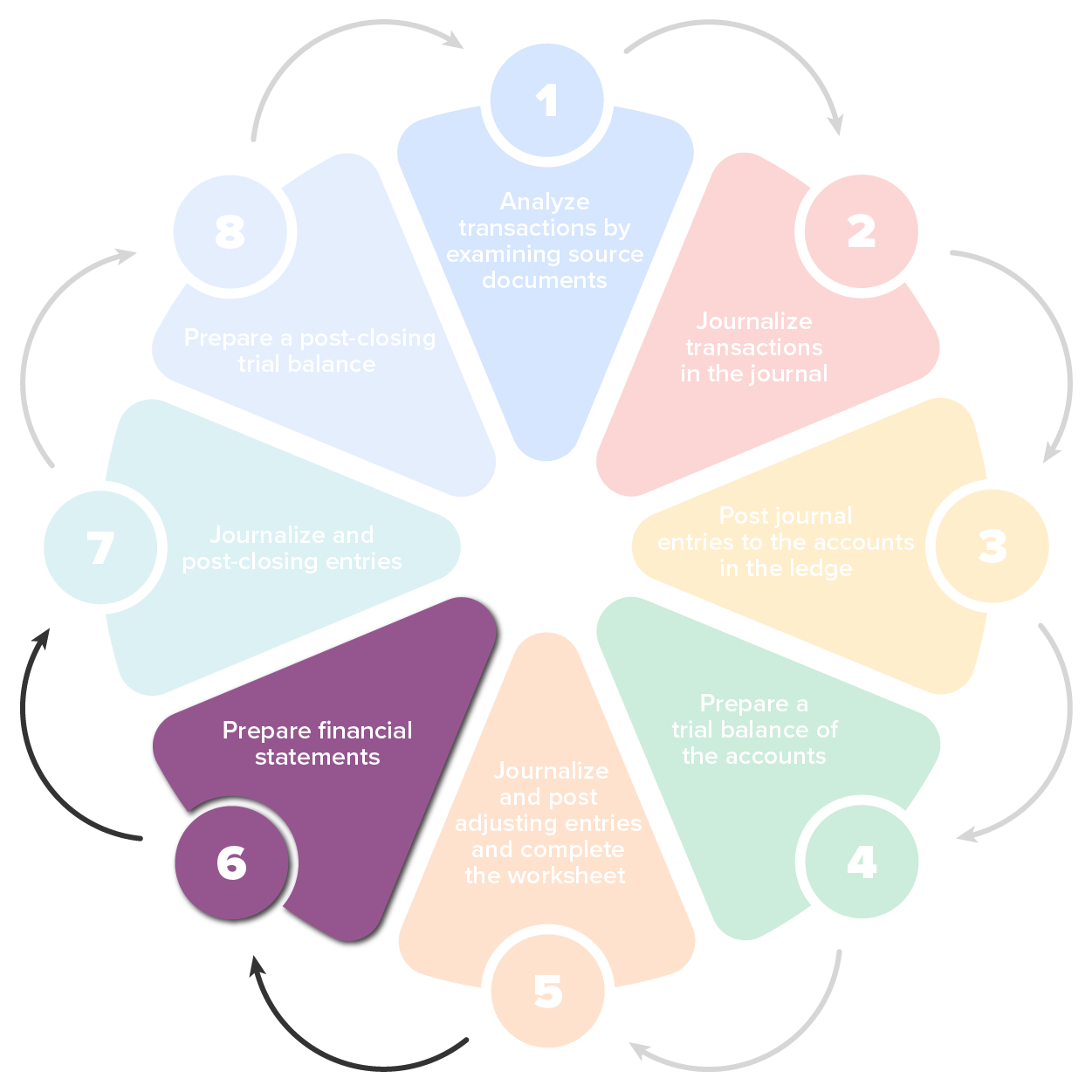

There are four basic financial statements. Together they present the profitability and strength of a company. The general purpose of the financial statements is to provide information about the results of operations, financial position, and cash flows of an organization. This information is used by the readers of financial statements to make decisions regarding the allocation of resources. At a more detailed level, there is a different purpose associated with each of the financial statements. Preparing the financial statements is step five of the accounting cycle.

IN CONTEXT

The Importance of Accurate Financial Statements

Financial statements give a glimpse into the operations of a company, and investors, lenders, owners, and others rely on the accuracy of this information when making future investing, lending, and growth decisions. When one of these statements is inaccurate, the financial implications are great.

For example, Celadon Group misreported revenues over the span of three years and elevated earnings during those years. The total overreported income was approximately $200–$250 million. This gross misreporting misled investors and led to the removal of Celadon Group from the New York Stock Exchange. Not only did this negatively impact Celadon Group’s stock price and lead to criminal investigations, but investors and lenders were left to wonder what might happen to their investments.

That is why it is so important to go through the detailed accounting process to reduce errors early on and hopefully prevent misinformation from reaching financial statements. The business must have strong internal controls and best practices to ensure the information is presented fairly.

The income statement, sometimes called a profit and loss statement, reports the profitability of a business organization for a stated period of time. In accounting, we measure profitability for a period, such as a month or year, by comparing the revenues earned with the expenses incurred to produce these revenues.

We measure revenues by the prices agreed on in the exchanges in which a business delivers goods or renders services. Expenses are measured by the assets surrendered or consumed in serving customers. If the revenues of a period exceed the expenses of the same period, net income results.

Net income is often called the earnings of the company. When expenses exceed revenues, the business has a net loss, and it has operated unprofitably.

An income statement can be used in several ways. One is to develop ratios that can pinpoint areas of improvement for a business, such as the gross margin ratio (calculated as the gross margin divided by sales) and the net profit ratio (calculated as the net profit or loss divided by sales). Another use is to track income statement line items over time, to see if there are any spikes or dips in the data that indicate the presence of problems that management should address.

EXAMPLE

One purpose of the statement of retained earnings is to connect the income statement and the balance sheet. The statement of retained earnings explains the changes in retained earnings between two balance sheet dates. These changes usually consist of the addition of net income (or deduction of net loss) and the deduction of dividends. The statement of retained earnings is useful for understanding how management utilizes the profits generated by a business.

Dividends are the means by which a corporation rewards its owners for providing it with investment funds. A dividend is a payment (usually of cash) to the owners of the business; it is a distribution of income to owners rather than an expense of doing business. Corporations are not required to pay dividends and, because dividends are not an expense, they do not appear on the income statement. The effect of a dividend is to reduce cash and retained earnings by the amount paid out. Then, the company no longer retains a portion of the income earned but passes it on to the stockholders. Receiving dividends is, of course, one of the primary reasons people invest in corporations.

EXAMPLE

The balance sheet, sometimes called the statement of financial position, lists the company’s assets, liabilities, and stockholders’ equity (including dollar amounts) at a specific moment in time. That specific moment is the close of business on the date of the balance sheet. The heading of the balance sheet differs from the headings on the income statement and statement of retained earnings. A balance sheet is like a photograph; it captures the financial position of a company at a particular point in time. The other two statements are for a period of time. As we study the assets, liabilities, and stockholders’ equity contained in a balance sheet, we will understand why this financial statement provides information about the solvency of the business. Solvency is the business’ ability to pay its long-term obligations on time.

The balance sheet is often considered to be the second most important of the financial statements (after the income statement) because it states the financial position of the business as of the balance sheet date.

When viewed in conjunction with the other financial statements, the balance sheet generates a clear picture of the financial situation of a business. In particular, the balance sheet can be used to examine a business's efficiency, leverage, and liquidity. Efficiency measures the level of performance against a standard. Leverage shows the use of debt to finance an organization’s activities and asset purchases. Finally, liquidity is a measure of the ability of a debtor to pay their debts as and when they fall due. Note, however, that when comparing these metrics to the results of other businesses for benchmarking purposes, it is important to restrict the analysis to other businesses within the same industry, since the financial structures of businesses vary across different industries.

EXAMPLE

Management is interested in the cash inflows to the company and the cash outflows from the company because these determine the company’s cash it has available to pay its bills when due. A business typically prepares a statement of cash flows for the same time period as the income statement. The statement of cash flows shows the cash inflows and cash outflows from operating, investing, and financing activities. Cash inflows show us the cash that is coming into the business and cash outflows show us the cash that is going out of the business.

The statement of cash flows is broken into three distinct sections operating, investing, and financing activities. The first section is the operating activities which generally include the cash effects of transactions and other events that enter into the determination of net income. Some examples of operating activities are cash received for product sales, commissions, and payroll. The next section of the statement of cash flows is the investing activities. Investing activities generally include business transactions involving the acquisition or disposal of long-term assets such as land, buildings, and equipment. The last section consists of the financing activities, including the cash effects of transactions and other events involving creditors and owners. These activities might consist of the sale of company shares or dividend payments.

The statement of cash flows can be used to determine trends in business performance that are not apparent in the rest of the financial statements. It is especially useful when there is a discrepancy between the amount of profits reported and the amount of net cash flow generated by operations. Many investors feel that the statement of cash flows is the most transparent of the financial statements (i.e., most difficult to fudge), and so they tend to rely upon it more than the other financial statements to discern the true performance of a business. They can use it to determine the sources and uses of cash.

There can be significant differences between the results shown in the income statement and the statement of cash flows, due to timing differences between the recording of a transaction and when the related cash is actually received. Management may be using aggressive revenue recognition to report revenue on the income statement for which cash inflows have not been received yet. Additionally, the business may have a lot of assets, and in return require large capital investments that do not appear in the income statement but are recorded on the statement of cash flows.

There are two ways to present the statement of cash flows. The direct method requires an organization to present cash flow information that is directly associated with the items triggering cash flows, such as cash collected from customers, interest and dividends received, cash paid to employees, cash paid to suppliers, interest paid, and income taxes paid.

Under the indirect method, the statement begins with the net income or loss reported on the company's income statement and then makes a series of adjustments to this figure to arrive at the amount of net cash provided by operating activities. These adjustments typically include depreciation and amortization, losses on accounts receivable, gain or loss on sale of assets, and changes in receivables, inventory, and payables.

It is important to note that the direct or indirect method only applies to the operating section of the statement of cash flows. The investing and financing sections are prepared the same way regardless of which method is used.

EXAMPLE

| Cash flows from Operating Activities | $58,000 |

| Revenues | $145,000 |

| Beginning Retained Earnings | $67,000 |

| Assets | $245,000 |

| Cash flows from Investing Activities | $42,000 |

| Common Stock | $63,000 |

| Liabilities | $80,000 |

| Cash Flows from Financing Activities | $32,000 |

| Expenses | $80,000 |

| Dividends Declared | $30,000 |

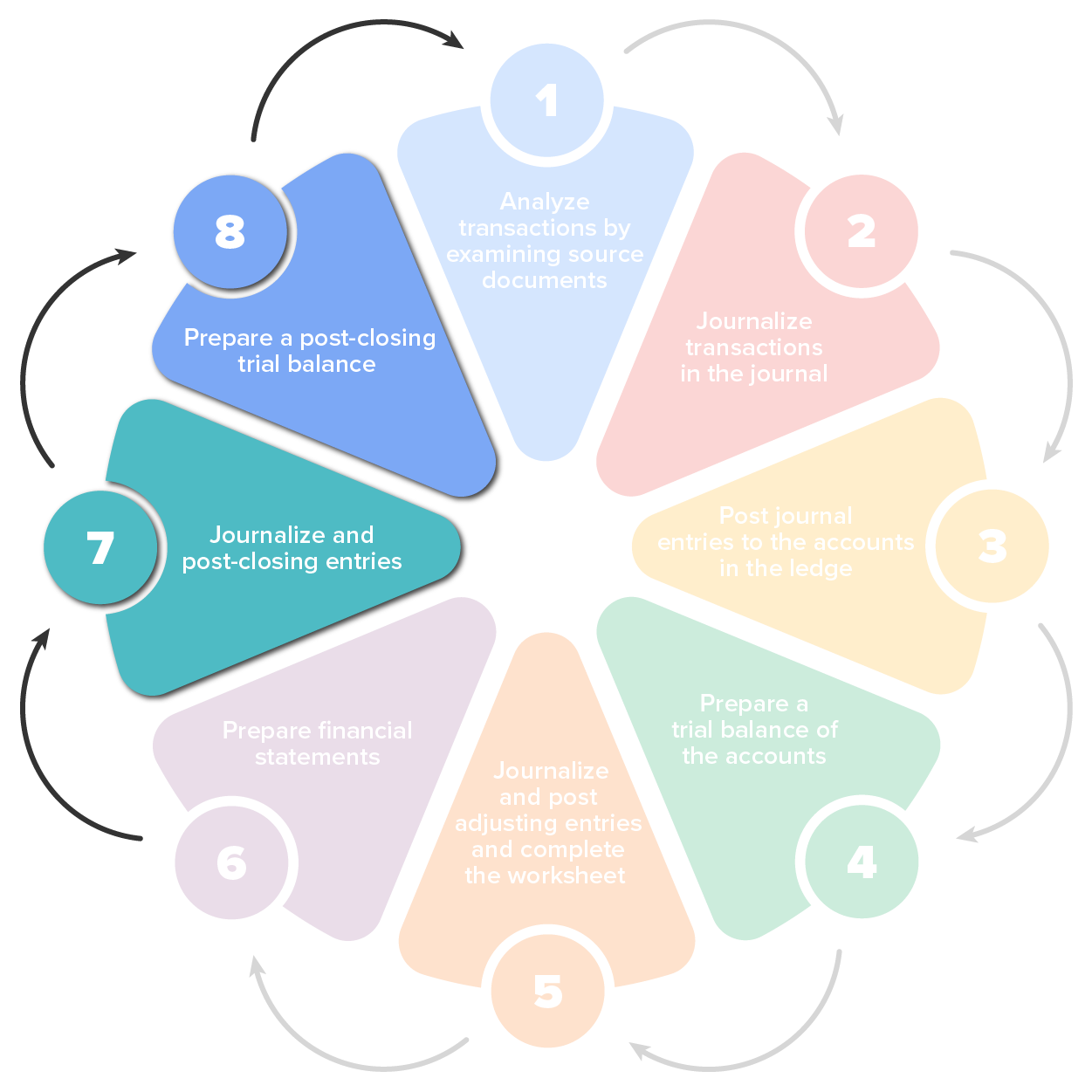

Once we complete step 5 of the accounting cycle, preparing the financial statements, we are able to close the accounting cycle by completing steps 6, 7, and 8. These last three steps of the accounting cycle consist of the following:

The next step in the accounting cycle is step 7, which is journalizing and posting closing entries. Closing entries are journal entries that are prepared to “reset” all temporary accounts to a zero balance, and which update the capital account to the current balance. Closing is intended to end or close off the revenue, expense, and withdrawal accounts at the end of the accounting period. These accounts are considered temporary accounts, because we record their activity throughout the period, and their balances do not extend to the next period. Instead, they are zeroed out. The information needed to complete closing entries is found in the income statement and balance sheet sections of the worksheet. The closing process allows us to accumulate new data about revenue, expenses, and withdrawals in the new accounting period.

The final step of the accounting cycle is to prepare the post-closing trial balance, which lists only permanent accounts in the ledger, and their balances after adjusting and closing entries have been posted. Permanent accounts are accounts whose balances are carried over to the next accounting period, such as assets, liabilities, and capital. The post-closing trial balance helps to check whether the ledger is in balance. This is important because so many new postings go to the ledger from the adjusting and closing process.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.