Table of Contents |

To put it another way, think about bankruptcy as a reset button. Imagine you’re playing a video game, and you’ve made so many mistakes in one level that there’s no way to win. The obstacles keep coming, your energy is drained, and every step forward feels impossible. Hitting reset lets you start fresh, wiser from the experience, and ready to play smarter. That’s what bankruptcy can do—it clears the path so you can focus on moving forward instead of staying stuck.

The stigma around bankruptcy can make people feel like it’s a personal failure, but nothing could be further from the truth. Life happens. Maybe it was a medical emergency, a job loss, a divorce, or even a pandemic that threw everything off course. These events are often out of our control, yet the financial aftermath can be devastating. The reality is that millions of people file for bankruptcy every year—not because they’re irresponsible, but because the system is designed to give people a second chance when circumstances spiral beyond their control.

EXAMPLE

Consider Rachel, a hardworking single mom. After losing her job during a company-wide layoff, she used her credit cards to cover basic living expenses, including groceries and rent. Despite finding a new job, the debt snowballed faster than she could manage. Filing for bankruptcy gave her the chance to eliminate the credit card debt and focus on providing for her family without the constant stress of harassing phone calls from creditors.To understand how bankruptcy might fit into your financial journey, let’s break it down step by step—covering the process, the options available, and the consequences of this critical financial decision.

When you’re in financial distress, every decision feels overwhelming. The bankruptcy process may seem complicated at first glance, but understanding the steps can bring clarity. Think of it as following a recipe—there are specific steps you need to follow to reach your desired outcome.

1. Assessing Your Financial Situation

The first step in the process is to take stock of your finances. This means gathering all the details about your debts, income, assets, and expenses. It can be uncomfortable, but facing the reality of your financial situation is necessary to make informed decisions.

This step is like stepping on the scale after months of avoiding it. It’s not fun, but it’s the only way to know where you stand. You’ll need this clarity to determine if bankruptcy is the right choice or if there are alternatives to explore.

EXAMPLE

Consider Kevin, who lost his job during an economic downturn. He’s been living off credit cards for the past year, accumulating $75,000 in debt. Despite finding a new job, his income can’t keep up with the interest payments. Kevin tracks his income and expenses and realizes he has no realistic way to repay his debts. This assessment helps him decide to explore bankruptcy as an option.2. Choosing the Right Type of Bankruptcy

Not all bankruptcy types are created equal. For individuals, these are the two most common options:

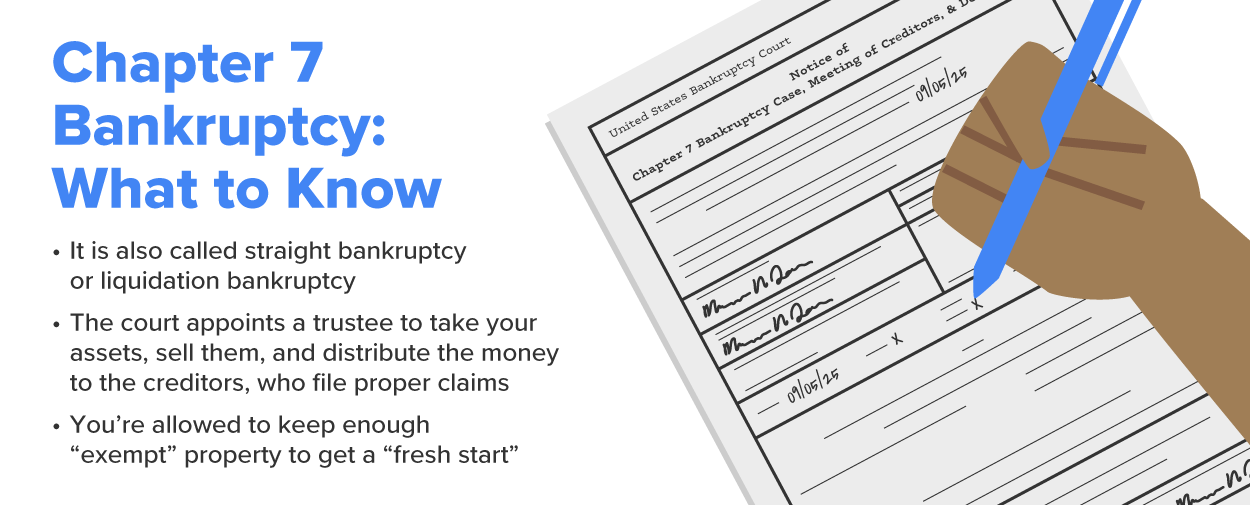

Chapter 7 Bankruptcy

Chapter 7 bankruptcy might sound intimidating at first, but let’s break it down into something easier to understand. Think of it as a financial clean slate for people who feel buried under debts they simply can’t pay back. It’s often called liquidation bankruptcy because, in some cases, you may need to sell (or liquidate) things you own that aren’t considered essential to help pay back some of your creditors. But don’t panic—this doesn’t mean you’ll lose everything!

Here’s the key: Chapter 7 is designed for people who don’t have much income or property to begin with. The law recognizes that if you’re barely scraping by, you need basic essentials to live, so it protects many of the things you own. These protected items, called exempt assets, often include things like your primary car, clothing, household goods, and sometimes even your home, depending on its value and state laws. Nonexempt assets—things like a second car, a boat, or expensive jewelry—might be sold to repay some of what you owe. However, in most Chapter 7 cases, people don’t have many nonexempt assets, so there’s often little or nothing to liquidate.

EXAMPLE

Amanda, a freelance graphic designer, has $40,000 in credit card debt but no significant assets apart from a modest car. After a means test shows that her income qualifies, she files for Chapter 7 and discharges her debts within a few months.

Here’s how Chapter 7 works:

Now, let’s take a look at Chapter 13 bankruptcy for comparison.

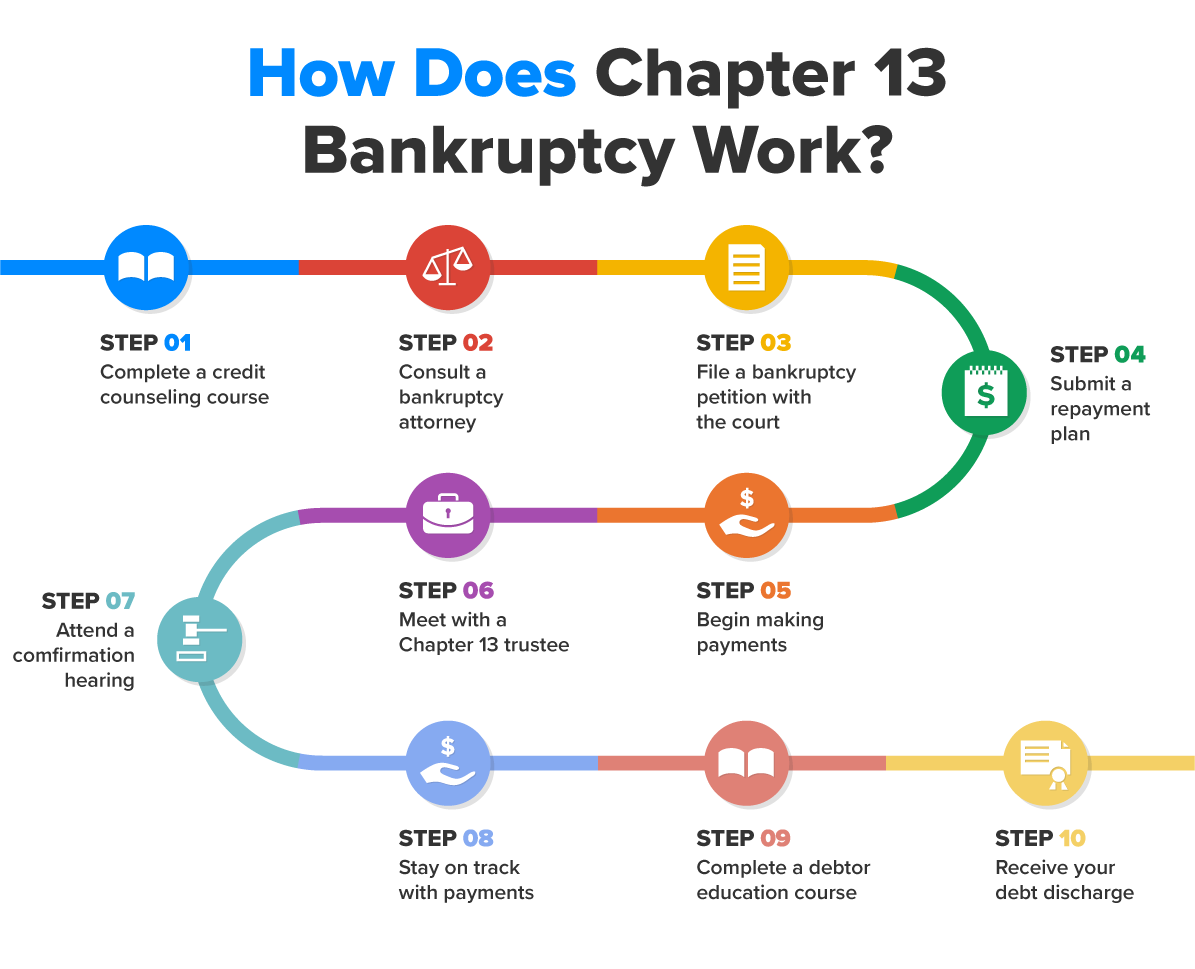

Chapter 13 Bankruptcy

Chapter 13 bankruptcy is often called reorganization bankruptcy and for good reason. Instead of wiping out all your debts right away like Chapter 7, Chapter 13 gives you the chance to reorganize your finances under the protection of the court. Think of it as hitting the pause button on the chaos of debt while you create a manageable plan to get back on track. What makes Chapter 13 unique is that you don’t have to give up your valuable assets—like your home or car. Instead, you get to keep them as long as you follow a court-approved repayment plan to pay off your debts over time.

EXAMPLE

Jarold, a nurse, fell behind on his mortgage and car payments after unexpected medical expenses. With Chapter 13, he can create a plan to repay creditors over 5 years while keeping his home and car.Here’s how Chapter 13 bankruptcy works:

Choosing the right type of bankruptcy is about finding a solution that works for your situation and helps you move forward. While it can offer much-needed relief, it’s important to know that every option comes with consequences. These effects might feel intimidating, but understanding them will help you prepare for the next steps and rebuild your financial future with confidence. Let’s dive into what to expect.

Bankruptcy can feel like a double-edged sword. On the one hand, it offers a fresh financial start by erasing or reorganizing debts that have become unmanageable. On the other hand, it’s not without its downsides. Understanding the consequences of bankruptcy can help you make an informed decision and prepare for the road ahead.

Let’s dive deeper into eight effects of bankruptcy on your financial life, your emotional well-being, and your future opportunities—and why these consequences, while real, are often less devastating than continuing to struggle with overwhelming debt.

1. Impact on Credit

The most well-known consequence of bankruptcy is its impact on your credit score. Filing for bankruptcy can drop your credit score by 100–200 points or more, depending on where you started. It also stays on your credit report for a long time:

2. Loss of Nonexempt Assets

In Chapter 7 bankruptcy, you may lose some of your property if it’s not protected under exemptions. These exemptions vary by state but often include necessities like your home (up to a certain value), your primary vehicle, clothing, and household goods. Any nonexempt assets, like a second car, a boat, or high-value jewelry, could be sold to repay your creditors.

That said, the majority of Chapter 7 cases are no-asset cases, meaning the filer doesn’t lose anything because they don’t own nonexempt property. Chapter 13 filers won’t lose any assets as long as they follow their repayment plan.

3. Bankruptcy Doesn’t Eliminate All Debts

It’s important to understand that bankruptcy doesn’t wipe out every type of debt. While it can discharge most unsecured debts like credit card balances, medical bills, and personal loans, some debts are nondischargeable, meaning you’re still responsible for paying them after bankruptcy. These are as follows:

EXAMPLE

After filing for Chapter 7, Mark’s $40,000 in credit card debt was erased, but he still had to pay back $15,000 in back taxes. Although he wasn’t completely debt-free, bankruptcy significantly reduced his financial burden and allowed him to focus on the remaining debts.4. Emotional and Social Impact

Bankruptcy isn’t just a financial process—it’s an emotional one, too. Many people feel a sense of shame or failure when they file for bankruptcy, often due to societal stigma. It can also be difficult to explain your situation to family, friends, or even potential employers who may find out about your filing.

However, it’s important to remember that bankruptcy is a tool meant to help—not punish. Financial struggles are often the result of circumstances beyond your control, like medical emergencies, job loss, or divorce. Recognizing this can help shift your mindset from guilt to empowerment.

5. Difficulty Getting Credit in the Short Term

After bankruptcy, it can be harder to qualify for loans or credit cards. Lenders may view you as a higher-risk borrower, and you may only qualify for high-interest rates or secured credit cards initially. However, rebuilding your credit after bankruptcy is possible—and many people find that creditors are willing to work with them sooner than expected.

EXAMPLE

Following his Chapter 7 filing, Richard was approved for a secured credit card with a $500 limit. By using the card responsibly and paying it off in full each month, he built a positive payment history. Within 2 years, he qualified for an unsecured credit card and started rebuilding his credit score.6. Public Record

Bankruptcy filings are part of public records, which means they can be accessed by anyone. While it’s unlikely that people will actively search for this information, it’s something to be aware of, especially if you’re applying for a job or renting a home. Some employers or landlords may ask about past bankruptcies as part of a background check.

7. Cost and Time Commitment

Bankruptcy isn’t free, and it isn’t instantaneous. Filing fees, attorney fees, and required credit counseling can add up. Chapter 7 cases are typically resolved within a few months, but Chapter 13 requires a 3–5-year repayment plan. During this time, you’ll need to stick to a strict budget to meet the terms of your plan.

8. Long-Term Benefits Outweigh Short-Term Consequences

While the consequences of bankruptcy are significant, they are often less severe than continuing to struggle with unmanageable debt. The stress of constant creditor calls, mounting interest, and sleepless nights can take a toll on your mental and physical health. Bankruptcy provides a path to relief and allows you to start rebuilding your financial future.

After filing for Chapter 7, you initially might feel regret about the impact on your credit score. But as months go by, you realize how much lighter you feel without the burden of being $100,000 in debt. The newfound financial freedom allows you to focus on improving your career and building an emergency savings fund.

Facing the consequences of bankruptcy can feel like standing at the bottom of a mountain, where you’re unsure of how to climb. It’s natural to feel overwhelmed and even a little scared. But here’s the truth: This isn’t the end of your story—it’s the start of a fresh, new chapter. Sure, there will be challenges, like rebuilding your credit, dealing with how others might perceive your decision, and making changes to how you manage money. But every small step you take will bring you closer to a brighter, more stable future. Bankruptcy isn’t a failure—it’s a chance to reset, rebuild, and reclaim control over your financial life.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.