Table of Contents |

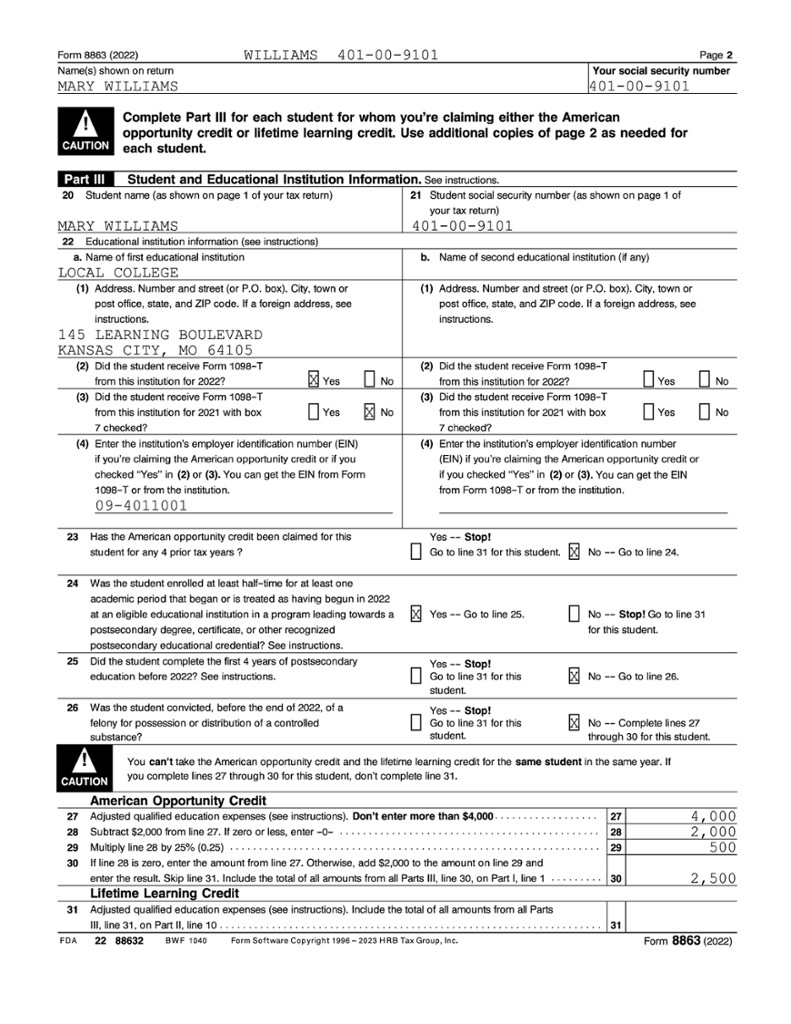

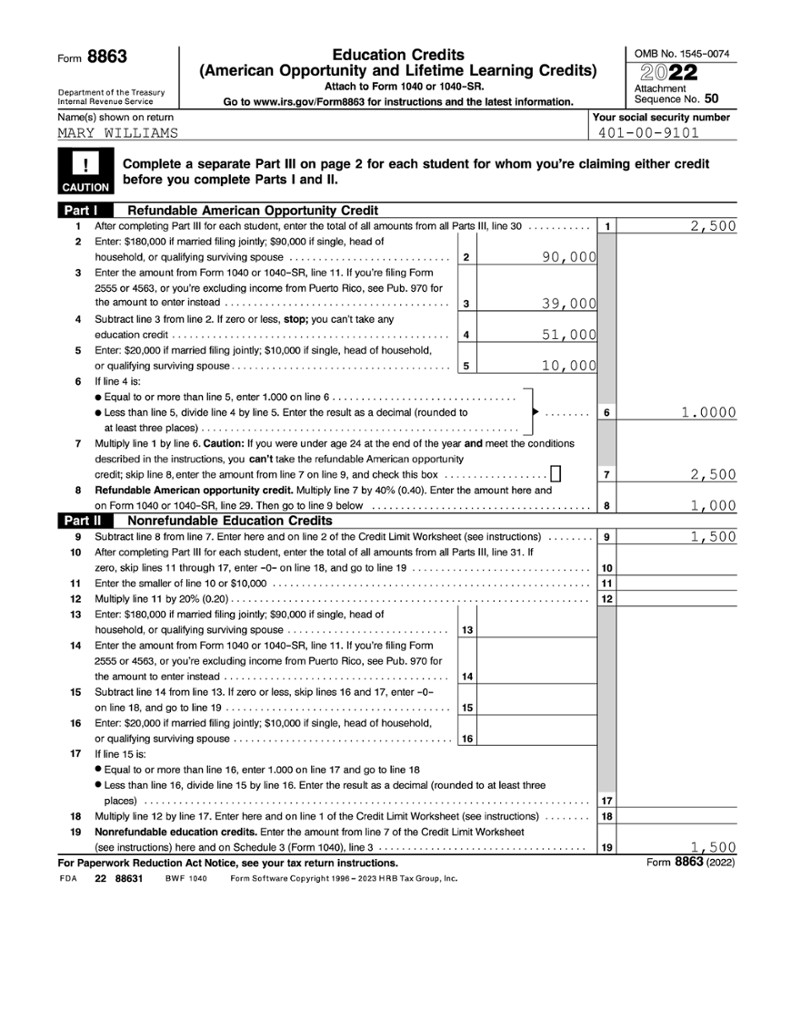

The AOTC is claimed on Form 8863, Education Credits (American Opportunity and Lifetime Learning Credits). We’re going to walk through Form 8863 using the following example.

Mary Williams, 27, is a single taxpayer and cannot be claimed as a dependent by any other taxpayer. Mary is enrolled full time at Local College (a qualifying educational institution) to earn a degree in law enforcement. The first year of Mary’s postsecondary education was 2020. Mary was not convicted of a felony for the possession or distribution of a controlled substance before the end of 2022.

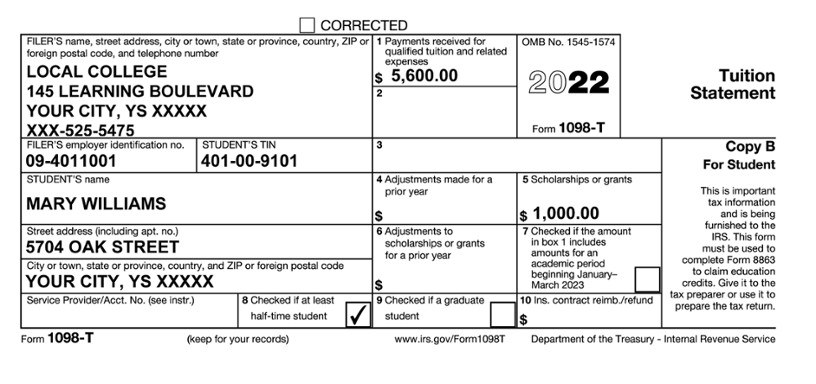

Mary received a Form 1098-T from Local College. Mary’s tuition expenses of $5,600 meet all of the qualifications for the AOTC. Mary also received a $1,000 grant. In addition to the expenses reported on Form 1098-T, Mary spent $712 on all of her textbooks, including one book ($100) required as a condition of enrollment and three other books ($612) not required as a condition of enrollment. She purchased them through an online book retailer and the school. Mary’s AGI (and MAGI) is $39,000 (all from wages). She had $3,200 federal income tax withheld. Mary’s Form 1098-T is shown below.

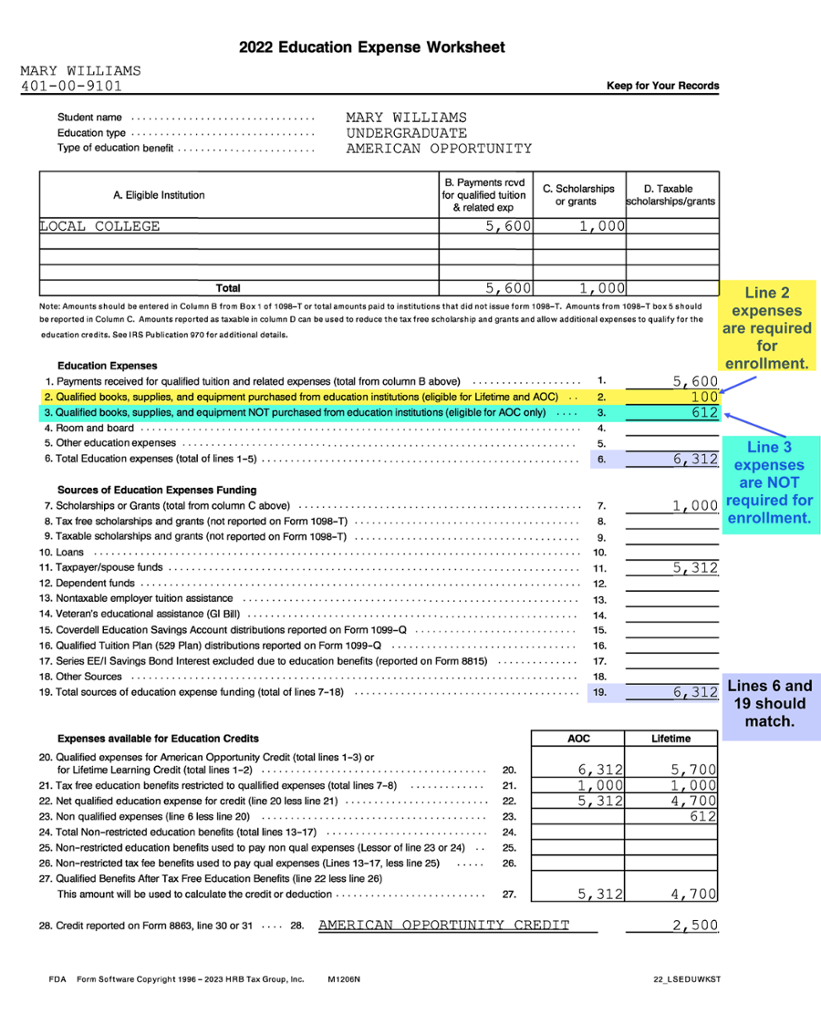

Mary’s total qualified education expenses are $6,312 ($5,600 + $712). There are $5,312 of qualified education expenses remaining after subtracting the $1,000 grant.

However, only $4,000 of qualified expenses can be used to calculate Mary’s AOTC, which is entered on Form 8863, Part III, line 27. This is because $4,000 is the maximum amount of qualified education expenses allowed when calculating the AOTC.

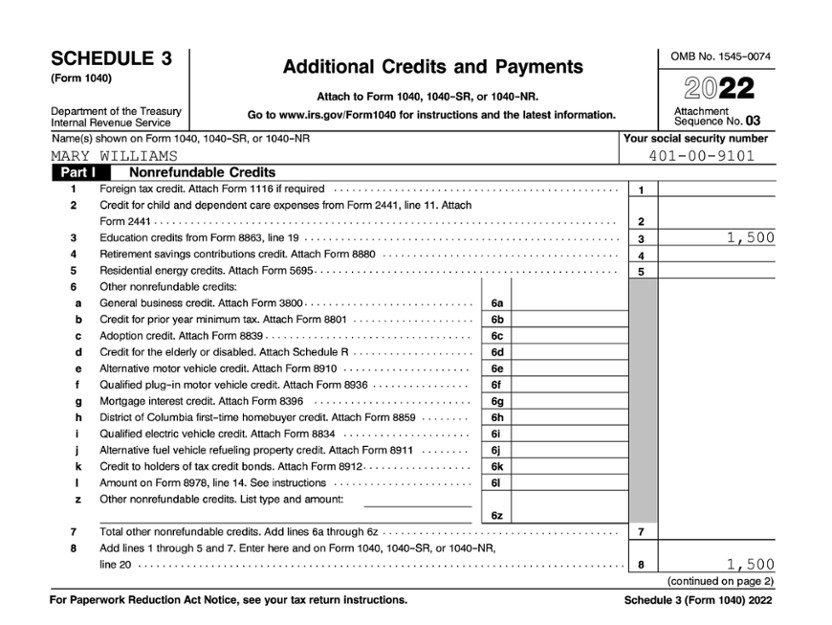

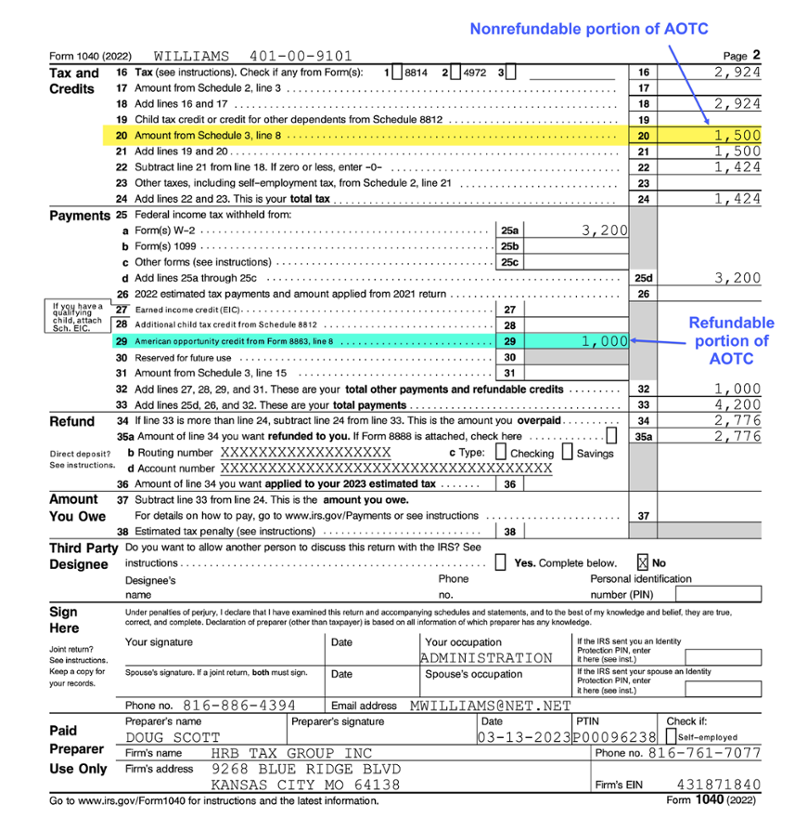

Mary qualifies for AOTC of $2,500, which is claimed on Form 8863 (shown below). Of her $2,500 AOTC, $1,500 is nonrefundable and $1,000 is refundable. Mary reports the $1,500 nonrefundable AOTC on Schedule 3, which then carries to Form 1040, line 20. She will report the $1,000 refundable AOTC on her Form 1040, line 29.

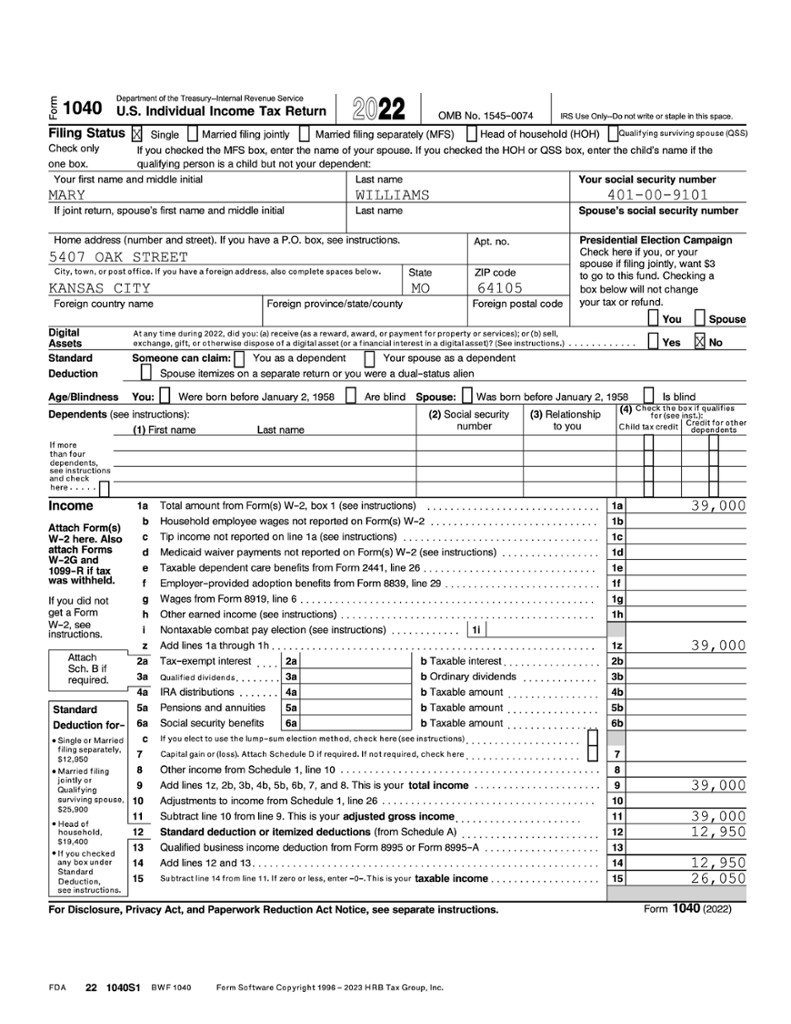

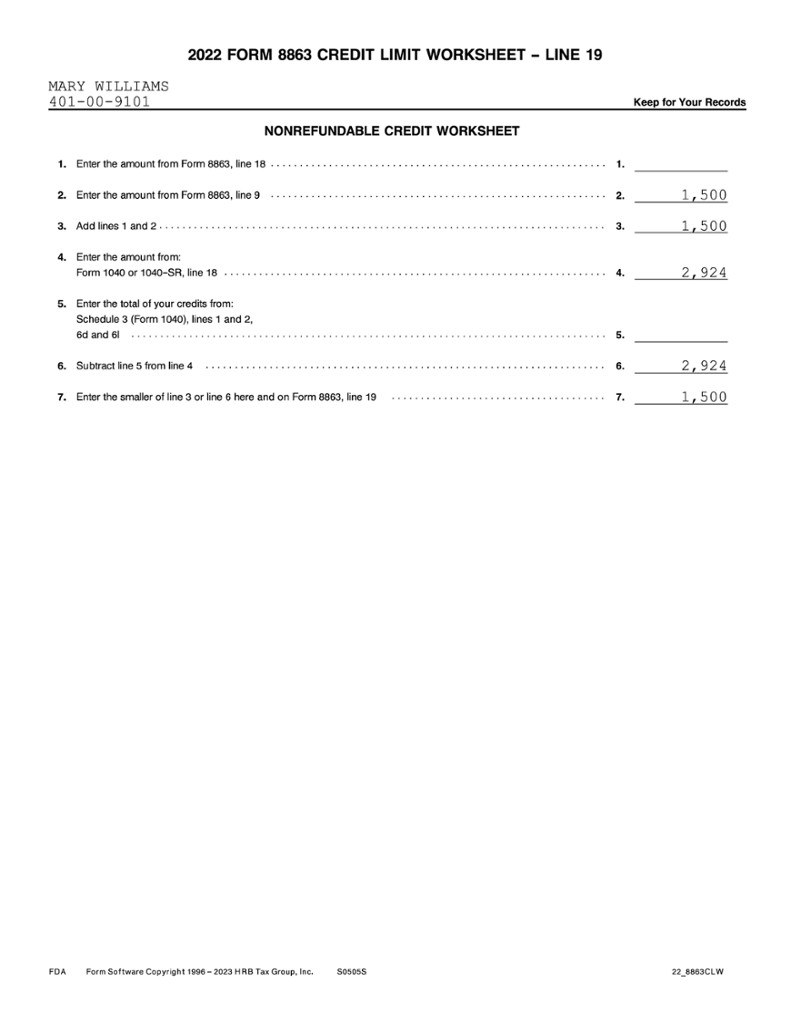

Mary’s forms are provided below in the order they would be completed when preparing the tax return, including the Form 1040, page 1; Education Expense Worksheet; Form 8863; Form 8863 Credit Limit Worksheet; Schedule 3; and Form 1040, page 2.

The Education Expense Worksheet can be used to help document the education expenses, how the expenses were paid, and a comparison of all three education benefits.

One item to note is the lines 2 and 3 amounts under “Education Expenses.” Line 2 includes qualified books, supplies, and equipment purchased as a requirement of enrollment. This makes the expenses qualified for the AOTC and the lifetime learning credit.

Line 3 includes books, supplies, and equipment NOT purchased as a requirement of enrollment. These expenses qualify only for the AOTC.

The significance between these two line numbers will become more apparent as you learn about the lifetime learning credit.

The table presented below provides an overview of the AOTC eligibility requirements for 2022.

| American Opportunity Tax Credit | |

|---|---|

| Maximum credit | $2,500 per eligible student. |

| Limited credit based on MAGI |

MAGI between $80,000 and $90,000 if single, HOH, or QSS. MAGI between $160,000 and $180,000 if MFJ. |

| Excluded from the credit based on MAGI |

MAGI $90,000 or above if single, HOH, or QSS. MAGI $180,000 or above if MFJ. |

| Refundable or nonrefundable | Up to 40% of AOTC may be refundable; the rest is nonrefundable (therefore, up to $1,000 may be refundable). |

| Number of years of postsecondary education | Available only for the first four years of postsecondary education. |

| Number of tax years credit is available | Available only for four tax years per eligible student. |

| Degree requirement | The student must be pursuing a program leading to a degree or other recognized academic credential. |

| Course load requirement | The student must be enrolled at least half-time for at least one academic period beginning during the tax year or the first three months of the following year. |

| Felony drug conviction | The student may not have any felony drug convictions as of the end of 2022. |

| Qualified expenses |

Tuition and fees required for enrollment. Course-related books, supplies, and equipment. These do not have to be purchased from the academic institution in order to qualify, nor do they have to be required as a condition of enrollment or attendance. |

| Academic periods | Payments made in 2022 for academic periods beginning in 2022 and the first three months of 2023. |