Table of Contents |

We previously discussed the allocation of overhead in the context of job order costing and process costing. Unlike direct materials and direct labor, overhead costs are not easily traceable to products; this is addressed by using allocation rates to estimate overhead. In this lesson, we will discuss additional methods for allocating overhead that are not specific to an individual costing method.

When a company produces a few products and production is similar across product lines, managers can limit their focus to a broad function of the company, such as production. This allows managers to use a single plantwide rate to allocate manufacturing overhead costs to their inventory. This is called the plantwide overhead rate method.

The plantwide overhead rate method uses one overhead allocation rate for all of the departments within a particular manufacturing facility or plant. The term plant can be used to refer to an entire factory, hospital, or other company that has multiple departments. The overhead rate is determined by using a volume-related measure, such as direct labor or machine hours, both of which are readily available in manufacturing settings. Although this method is referred to as the plantwide allocation method, it can be used both in manufacturing companies and service companies. Merchandising companies will not use the plantwide overhead rate method since they only carry merchandise inventory, which is a finished product that doesn’t require the use of various activities.

EXAMPLE

In a hospital, overhead could be applied to different patients, treatments, or departments by using one overhead rate for the entire hospital.This method is similar to calculating overhead for a particular cost object when job order costing is used. Remember that a cost object is any product, service, department, or activity to which costs are assigned or allocated. When the plantwide overhead rate method is used, the cost object is the individual product.

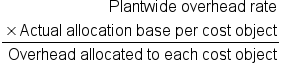

Under the plantwide overhead rate method, a single overhead rate is calculated based on the total amount of overhead costs and a chosen allocation base, such as direct labor hours or machine hours. The allocation base will depend on which process drives the costs in the overall production process. The plantwide overhead rate is calculated by dividing the total budgeted overhead costs by the total budgeted allocation base.

This rate is then applied to each cost object based on the actual usage of the allocation base by that object. We do this by multiplying the plantwide overhead rate by the actual amount of the allocation base per cost object.

When choosing an allocation base, managers need to think about which activities have an impact on the overhead. There should be a cause-and-effect relationship between the allocation base and the overhead costs.

EXAMPLE

Let’s introduce a new example company for understanding this method.

For managers, using a single plantwide rate is a fairly easy process. However, it might not always be the most accurate process for allocating overhead. For instance, if a company has two departments and they have different cost drivers, using one rate will not provide the most accurate allocation of overhead. Since the departments have different cost drivers, a more accurate approach to allocating overhead would be to use allocation rates that align with the cost driver for each department. This will be explained further as we move to the discussion of the departmental overhead rate method.

EXAMPLE

High Challenge Company has a machining department and an assembly department. The machining department uses machine hours as the cost driver, and the assembly department uses direct labor hours as the cost driver; therefore, a single plantwide rate might not be the most accurate option for the company.Companies often have several departments that produce different products using various amounts of overhead. When this happens, using a single plantwide rate can provide cost assignments that do not truly reflect the costs that are necessary to manufacture that product. When there are different departments with different cost drivers, more accurate overhead cost allocations can be determined by using multiple overhead rates to reflect each of the departments. In using the departmental overhead rate method, each department will have its own allocation rate and its own allocation base.

The departmental overhead rate method uses a four-step process for allocating overhead.

In the first step, we will assign overhead costs to each department. This is done by splitting the amount of overhead between the departments based on how much of the overhead costs are used within the department.

EXAMPLE

For High Challenge Company, there will be an allocation rate and base for the machining department and an allocation rate and base for the assembly department. High Challenge Company will assign its $2,000,000 overhead costs to its two production departments, with $1,600,000 being traceable to the machining department and $400,000 being traceable to the assembly department.In the second step, we will determine an effective allocation base for each department based on what drives costs in that department.

EXAMPLE

For the machining department at High Challenge, machine hours are used as the allocation base because machines are heavily used in the machining process, as we might expect from the name. For the assembly department, labor hours are used as the allocation base because assembling the bicycles is a more manual, labor-intensive process.Step Three consists of computing the overhead allocation rate for each department. The formula is similar to the formula for the plantwide allocation rate, except here, we use the budgeted overhead costs and budgeted allocation base only for the department at hand instead of for the entire plant.

EXAMPLE

For High Challenge Company, the machining department has a total of 10,000 machine hours, and the assembly department has a total of 10,000 direct labor hours. In this case, the departmental overhead rate is $160 ($1,600,000/10,000) per machine hour for the machining department and $40 ($400,000/10,000) per direct labor hour for the assembly department.

Once the departmental overhead rates are calculated, the final step is to assign the overhead costs to each product using departmental overhead rates.

EXAMPLE

The hybrid bicycle uses 5 machine hours per unit for the machining process and 5 direct labor hours for the assembly process. The mountain bicycle, on the other hand, uses 5 machine hours for the machining process and 10 direct labor hours for the assembly process.The overhead is calculated for each department by multiplying the departmental overhead rate by the number of hours required per unit.

EXAMPLE

For the hybrid bicycle, the overhead cost that is allocated to the machining department is $800 ($160 per machine hour x 5 machine hours), and the overhead cost that is allocated to the assembly department is $200 ($40 per direct labor hour x 5 direct labor hours), giving us a total of $1,000. The mountain bicycle has a total overhead cost of $1,200, which is made up of $800 ($160 per machine hour x 5 machine hours) from the machining department and $400 ($40 per direct labor hour x 10 direct labor hours) from the assembly department.

The amount of overhead cost can vary depending on the allocation method that is used.

EXAMPLE

If we compare the results for High Challenge Company when the plantwide rate was used versus when the departmental rate was used, it is clear that using the departmental rate is more effective in situations where there are multiple cost drivers and multiple departments. While the total budgeted overhead costs are the same under both the plantwide rate and the departmental rate methods, there are significant differences in the allocation of overhead.

In situations where there are multiple departments with different cost drivers, the departmental rate will most often provide a better allocation of overhead than the plantwide rate.

EXAMPLE

The overhead per unit for the hybrid bike is the same regardless of the overhead rate method, but the overhead per unit for the mountain bike is quite different! The departmental rate is lower than the plantwide rate because an appropriate cost driver is used for each department, rather than one cost driver for both.When choosing an overhead allocation method, it is important to select the method that will provide the most accurate allocation of overhead for each company’s specific situation.

There are some similarities between the plantwide and departmental overhead rate methods, such as the fact that they are both based on information that is available, such as direct labor or direct machine hours, and they are both easy to implement.

The single plantwide overhead rate is based on the idea that overhead costs change when the allocation base changes and that all products use overhead costs in the same proportions. If a company has multiple products that use overhead in different ways, however, the single plantwide rate may not be a reasonable option.

The use of the departmental overhead rate method assumes that different departments have different cost drivers, and those cost drivers are proportional to the allocation base. When products differ in batch size and complexity, they will typically have different amounts of overhead costs.

EXAMPLE

High Challenge Company has multiple cost drivers, so there will be different amounts of overhead costs for each department.Even though the departmental rate method will provide a more accurate allocation of overhead than the single plantwide rate, it still does not accurately assign some other indirect costs such as machine depreciation or utilities. These costs are more accurately calculated with activity-based costing, which we will discuss in the next lesson.

The decision to use the plantwide rate or departmental rates depends on the products and the process that is used in production. If a company produces similar products that use the same resources, the plantwide rate can be an efficient method to use. If multiple products use the manufacturing factory in multiple different ways, departmental rates provide a better picture of the use of manufacturing resources by the different products.

For managers to make the decision to use the plantwide rate versus departmental rates, they need to look at the costs and benefits of each system.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.